WEEK ENDING 2/2/2024

- Fed takes March easing off the table, and the market buries it.

- Friday’s jobs report does not reflect a slowing economy.

- Republicans and their pundits could be picking on the wrong pop star.

A CITY DIFFERENT TAKE

This has been an interesting week.

On January 30, the Jolts survey showed more than 9 million job openings, beating expectations of 8.75 million. The 10-year Treasury bond finished the day at 4.033%.

On January 31, the Fed held interest rates steady and assigned a low probability of a March rate cut. The market-assigned probability of a March rate cut was 42% on January 30 and dropped to 35% at the close of business on January 31.

On February 1, other economic numbers came out which showed a mixed economic picture. The 10-year Treasury bond finished the day at 3.881%.

The big surprise came on Friday with the monthly jobs report. Nonfarm payroll beat expectations by a mile (+353,000 compared to +185,000), and revisions were significantly positive, with two-month payroll net revisions of +126,000.

That was not the only surprise; average hourly earnings M/M beat expectations (0.6% vs. 0.3%), and Y/Y's 4.5% rise exceeded the expected 4.1% increase. The unemployment rate held steady at 3.7%. The only worrisome number was average weekly hours, which was down versus expectations (34.1 versus 34.3, a 0.6% decrease). Measured against the M/M change in average hourly earnings, it means workers worked less but were paid the same. And measured against the Y/Y change in average hourly earnings, it indicates workers are better off. Consumers have the same or more cash in their pockets.

All in all, this is not a jobs report of a slowing economy. To go back to March’s rate cut, as of this writing, the market's implied probability is now down to 24%.

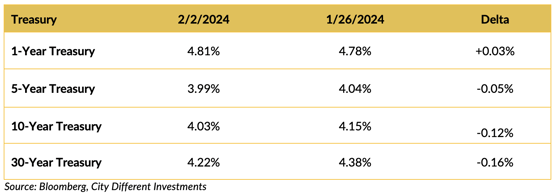

CHANGES IN RATES

Friday’s employment report brought the Treasury rally to an abrupt end. Although Treasury rates were lower on the week.

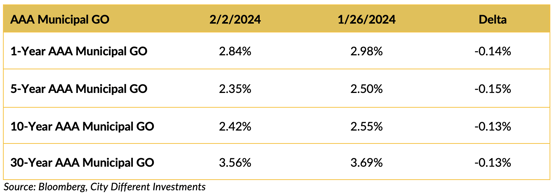

The municipal market’s yield moved lower on the week.

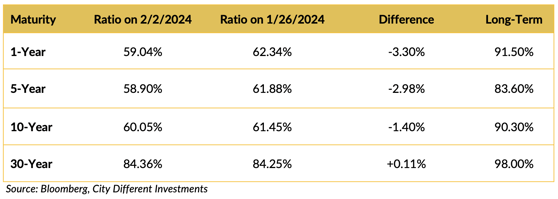

The municipal/Treasury ratios decreased (municipal bonds became more expensive) during the week. They are past breakeven rates versus their Treasury equivalents.

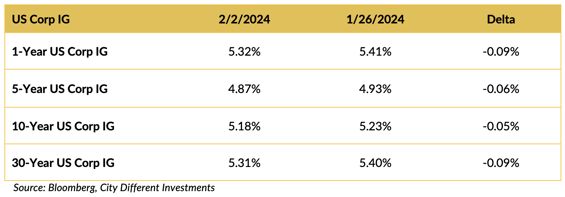

This market segment was lower on the week but moved higher after Friday’s jobs report.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

The conflict in the Middle East just got hotter. The United States carried out successful retaliatory strikes in Iraq and Syria in response to attacks on a U.S. base in Jordan that saw three U.S. service members killed and about 50 injured. These strikes were carried out after the President and First Lady attended a ceremony bringing back the remains of our fallen soldiers.

The impeachment vote of Department of Homeland Security Secretary Mayorkas is moving forward in the House.

“ Washington — The House is expected to vote in the coming days on whether to impeach Homeland Security Secretary Alejandro Mayorkas for the Biden administration's handling of the situation along the U.S.-Mexico border.”

The next line of the article caught our interest: “If successful, it would mark just the second impeachment of a Cabinet secretary in U.S. history, and the first in nearly 150 years.”

A quick Google search yielded the following results: in U.S. history, there have been 20 impeachments of 21 federal officers. 15 judges have been impeached. And only three presidents have been impeached (although many have been threatened): Andrew Johnson in 1868, Bill Clinton in 1999, and Donald Trump (twice) in 2019.

It still takes a 2/3 majority vote in the Senate to convict, so these House actions seem to be more Kabuki Dance than effective governance. As Captain Renault said to Rick in Casablanca, “I’m shocked! Shocked to find that gambling is going on in here,” as the croupier handed him his winnings.

A Senate deal on border policies is at hand, as reported by PBS:

“WASHINGTON (AP) — Senate negotiators on Friday reached a deal on a proposal to overhaul the asylum system at the U.S. border with Mexico, clearing the way for Democratic and Republican Senate leaders to begin the difficult task of convincing Congress to pass a national security package that will include tens of billions of dollars for Ukraine and immigration enforcement, as well as funding for Israel and other American allies.”

Passage of that bill in the House of Representatives, however, looks doubtful. What’s good for the Country may not be good politics.

“On the right, many conservatives oppose both continued funding for Ukraine as well as compromises on border enforcement. House Speaker Mike Johnson has repeatedly declared he won’t compromise on hardline border enforcement measures, but he has said he will not pass final judgment until he is able to read the bill.”

We wish we knew the lyrics to Taylor Swift songs so we could parody them for the next section, but alas, we don’t. Even if it is a generational thing, we don’t understand why Republicans would engage in absurd theories about her, assuming she’ll influence the election in favor of Biden. Not since Kanye West interrupted her at the Grammys has a group or individual successfully intimidated her.

“Some Republicans have speculated that Swift is some sort of Pentagon plant, ginned up by secret liberal forces to swing the 2024 presidential election while also boosting the fortunes of the Kansas City Chiefs, who are headed into the Super Bowl with Swift's boyfriend, Travis Kelce, a tight end. Others suggest her prior support for Democrats and opposition to Republicans is misguided.”

From what we know about her, she is too smart and too tough to pick on. Plus her “Swiftie” fans (and there are a lot of them, including our Marketing Director) are rabid!

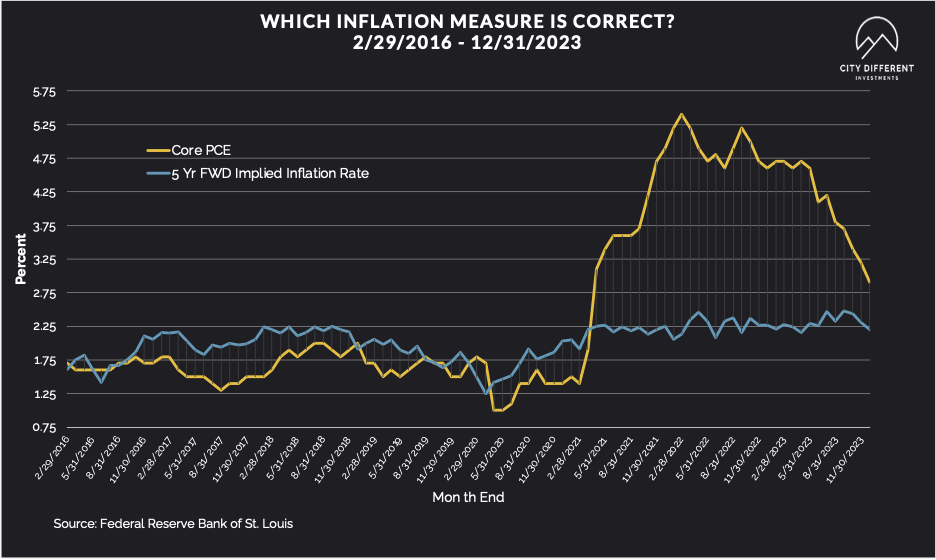

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week of February 2 at 2.23%, 11 basis points lower than the January 26 close of 2.34%. The 10-year Breakeven Inflation Rate finished the week at 2.21%, nine basis points lower than the close of January 26.

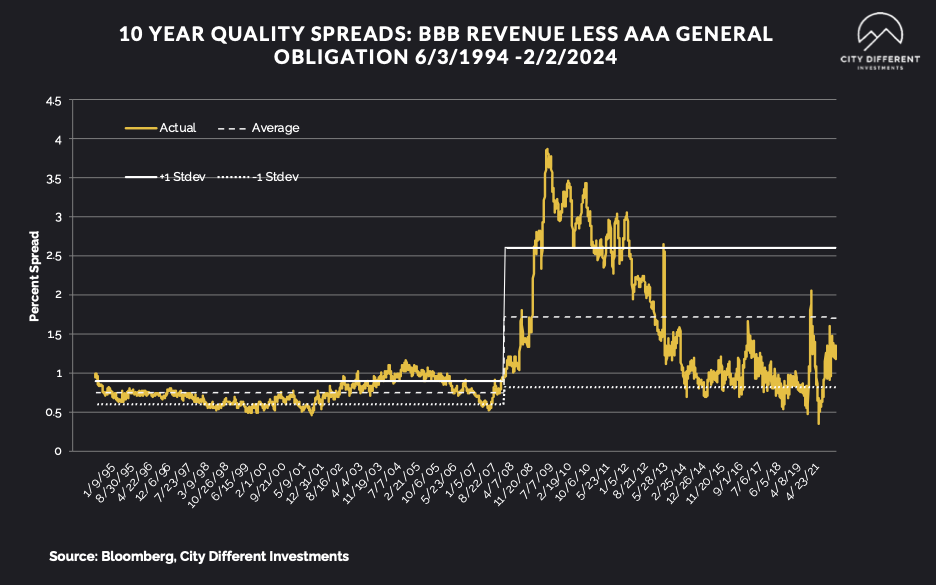

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of February 2 were 1.35%, 17 basis points higher than the January 26 reading of 1.18% (based on our calculations). The long-term average is 1.71%.

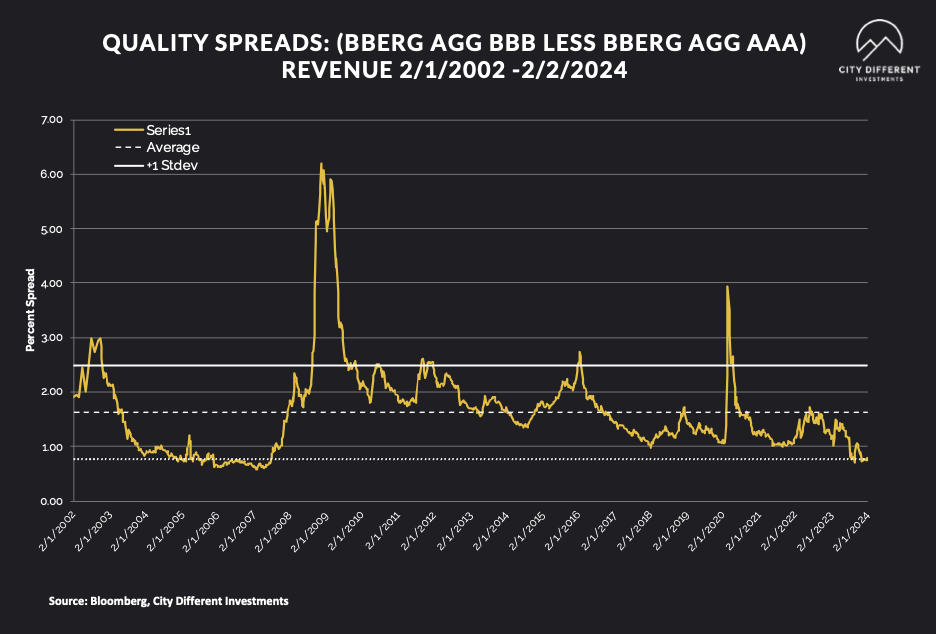

Quality spreads in the taxable market are not attractive but were slightly higher, ending the week at 0.78%, four basis points higher than last week. High-yield quality spreads were 3.21% on February 2.

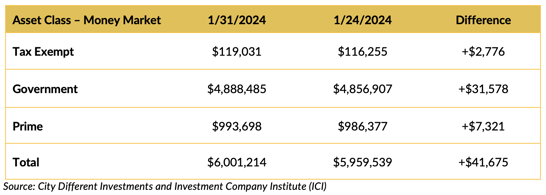

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds win the week across all segments. Beware of the “Cash Trap.” I know we are sounding like a broken record, but reinvestment risk is a big money market risk.

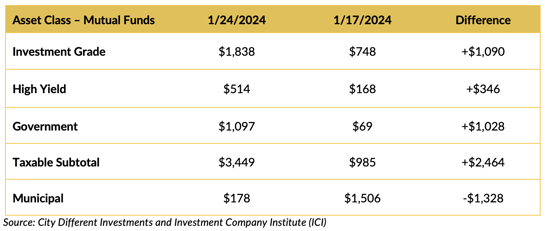

Mutual Fund Flows (millions of dollars)

Bond funds saw positive cash flow; we will see if Friday’s higher yields impact next week's numbers.

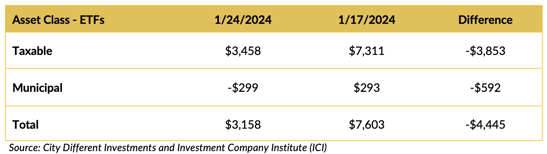

ETF Fund Flows (millions of dollars)

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Supply for municipal tax-exempt calendar will likely remain uneven for the next few weeks at the start of the new year. This week’s municipal tax-exempt calendar estimates are $8 billion in new issuance. Now, things will start to get interesting.

CONCLUSION

Market participants have been anticipating the start of a Fed easing program. These views may be premature. Friday’s jobs report does not indicate a slowing economy; quite the opposite. Inflation does not normally move in one direction. With higher incomes and conflict in the Middle East disrupting supply chains, participants looking for lower short-term rates may be disappointed; the economy is doing fine with short-term rates where they are.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.