Vin Walden recently sat down with the Wall Street Transcript to discuss potential dangers lurking in the stock market. Find out which companies he thinks investors should avoid.

.png?width=793&height=264&name=Copy%20of%20Copy%20of%20bullet%20barbell%20ladder%20(2).png)

Electric Cars and AI Fuel Long-Term Electricity Demand

Read the PDF version HERE.

SECTOR — GENERAL INVESTING

TWST: Just to start things off, could you tell us how long you have been with City Different and what do you do there?

Mr. Walden: Sure. I’ve been a full-time investor since 2002 with my colleagues at City Different. However, the City Different team specifically was set up about three years ago, whereby we left our previous shop and started this boutique investment firm.

So we’re on our third year now for our global equity strategy. And, knock on wood, it’s a continuation of what we’ve been doing together for many years; we have a tradition of client satisfaction, and we’re happy to see that carrying on.

TWST: Could you give us an idea of how many holdings make up your global equity portfolio and if there are any sort of criteria that you’re employing with regards to capitalization or geography?

Mr. Walden: This is a global, opportunistic, focused portfolio of equities. It’s 20 to 30 holdings. We’re flexible with respect to geographic diversification and industry exposure.

It tends to be 50% or 60% U.S. Right now we’re about 60% U.S., 40% non-U.S. and important countries for us are Canada and Norway. We’re happy to invest internationally, but we’re looking for stable law-and-order jurisdictions.

As far as market cap, it tends to be mid-cap and up, $500 million and up. Right now our median market cap is around $5 billion.

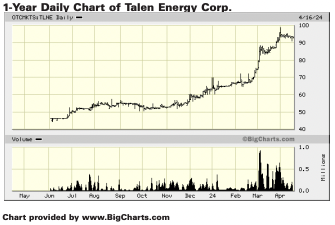

TWST: Taking a look at some of the top holdings in your portfolio as of the end of last year, for example, Cameco Corporation (NYSE:CCJ) and Golar LNG (NASDAQ:GLNG) and Talen Energy (OTCMKTS:TLNE), you guys have employed a greater emphasis on energy and utilities versus the MSCI ACWI despite employing that as your benchmark. Could you give me your reasoning behind that deviation?

Mr. Walden: Sure. We cottoned on to this energy transition as a mega theme several years ago in connection with decarbonization goals for the world as well as the war in Ukraine. There’s a lot of big changes underway in both the supply and the demand for energy and electricity, and we think these long-term structural shifts can produce opportunities.

For example, electricity in the U.S. has been a no-growth industry for most of this century, but that has now changed dramatically. Steady demand growth is now coming from electric cars and the advent of artificial intelligence. These trends underpin a handful of our investments.

TWST: Before we get into those specific companies, I understand you spent several years in the post-Soviet Commonwealth of Independent States.

Mr. Walden: Yes.

TWST: Perhaps you could share your thoughts on how geopolitics in that region will shape world energy markets. I’m also curious, with the war in Ukraine now over two years old, what further effects you might see on commodity markets and securities and the like, given that that conflict is ongoing and it would seem that, if anything, we’re getting closer to a new cold war rather than moving towards greater globalization and peace?

Mr. Walden: It’s a great question. Over the course of my career, I came to appreciate Russia’s power as a commodities supplier for the globe. It’s a vast country with tremendous natural resources and so important in the world economy with respect to many commodities, including oil and gas and wheat and many precious metals and so on.

And now with the war going on, there’s been a scramble for the former customers of Russian commodities to diversify and essentially to get out of those arrangements and find other suppliers. An obvious example would be Western Europe used to get most of its natural gas from Russia, and they want to end that arrangement as quickly as possible.

We’re very bullish on nuclear energy, but so much of the nuclear ecosystem has revolved around the former Soviet Union in terms of production and enrichment of nuclear fuel. And those arrangements must be restructured. We have far too much dependency in the West on Russia. Still today, the U.S. is buying 25% of its nuclear fuel from Russia.

So that’s not a comfortable status quo. So I think, just to follow on those two aspects, there’s a strong demand for non-Russian natural gas and a strong demand for non-Russian nuclear fuel and nuclear services. That’s what we see as a potential opportunity.

TWST: Certainly this is a very viable backdrop for a company such as Cameco to grow within. Looking at some of your other top five holdings, such as Talen and Golar, why would you choose those companies over other energy companies? Are there special opportunities within the spaces that they’re working in?

Mr. Walden: Yes. So as I mentioned, we’ve been digging around this area for quite a while and last summer we uncovered this power company called Talen Energy. Talen is essentially a pure play of nuclear energy production based in Pennsylvania. They own one of the biggest and best power plants in the United States. Since Talen is a carbon-free, super-efficient source of electricity production, we think that’s a good place to be.

Electricity happens to be a growth sector from now on, in my opinion, for a number of reasons, including the growth of electric vehicles as well as the rise of AI, which is very energy-intensive. In my entire career, electricity has been a no-growth industry, not even growing with GDP, but now it’s a secular growth area. When you buy an electric vehicle, as you can imagine, your household consumption of electricity goes up. And it goes up by a lot.

Pete Buttigieg pointed out that if a household switches from traditional internal combustion engine cars to electric vehicles, that’s the equivalent of purchasing 20 refrigerators for one house. So you can imagine if we all went out and bought 20 refrigerators and plugged them in in the basement, that’s a lot of new electricity demand. Talen Energy is helping to meet that demand, and we think that’s conceptually pretty sound.

By the way, I should mention that we periodically publish synopses of our investments on our website, and we did so with Talen. So you can see our synopsis of Talen Energy on our website, which is at citydifferentinvestments.com.

TWST: And aside from energy and utilities, I also noticed quite a heavy weighting of consumer discretionary and materials compared to the ACWI within your portfolio. What is the reasoning behind your higher weightings?

Mr. Walden: In consumer discretionary, we think there’s still a big opportunity for technology and AI to strengthen some of the business models in that sector. And specifically, we have an important investment in Mercado Libre (NASDAQ:MELI) in South America, which is sort of Latin America’s Amazon.com. It’s essentially an e-commerce and financial technology company for South America. Their largest markets are Brazil and Mexico, And in this case, we think that the core e-commerce proposition is still very compelling. Broader selection, lower prices, more convenience, faster delivery — all of that still resonates.

Mercado Libre is the kind of business that gets stronger over time. Every year, they have a broader selection, a bit more scale, they can lower prices a little bit more, and they get better at logistics. So the business really has legs. Fundamental progress at Mercado Libre has been impressive, and we see a bright future for that company. In fact, I am going to Brazil soon to do more research and kick the tires on that.

TWST: That sort of leads into my next question, which is, are there any markets or geographies, sectors, what have you, that you feel us investors are unfairly overlooking at the moment?

Mr. Walden: I look at our portfolio, which is very different from the benchmark, and yet we’re very happy with it, and we’re off to a good start again in 2024. So I think maybe it illustrates the benefits you can get from active management. And thinking a little more outside the box, beyond the Magnificent Seven.

The Magnificent Seven are plainly magnificent companies, but there’s an awful lot of capital that’s been chasing those seven ideas for quite a while. And we think there could be significant advantages, that’s been our experience, in broadening your scope of view and being different from the crowd.

TWST: Continuing further on geographies, since you mentioned possibly going to visit Latin America soon, do you feel growth in Latin America could be a spur for worldwide economic activity in general in the coming years?

Mr. Walden: I don’t know about that, per se. These are still relatively small economies in the context of the world. But the point there is, these are young, vibrant countries where some of these business models, we think, are in their early stages.

Interest rates in Brazil are still very high but trending down now, importantly. In Argentina, you have a new government that may be bringing in some fiscal responsibility and economic stability. So it all seems very promising to me, and we take a long-term view on our holdings.

With respect to Mercado Libre, they have seen, call it, 20 years of profitable growth, and yet it’s very early days.

TWST: Now, are there any kind of areas of the market that you would advise investors to avoid at the moment, whether that be in the sense of some sector or a geographic region?

Mr. Walden: Yes, actually I would. I think this is a timely topic right now. In general, you want to avoid hype and you want to avoid frauds. And right now we have a ripe environment for hype and for frauds. In the case of artificial intelligence, there’s elements of truth and legitimate excitement there, but inevitably there are pretenders that want to ride along and clothe themselves in the AI wrapper. So I’d be very careful about that.

I think, similarly, in the ESG space and among the environmentally friendly types of companies, there’s a lot of unproven business models. The essential economics of some of those companies are still to be determined, to put it politely.

In the frenzy of late 2020 and into 2021, you had many companies going public in the ESG area, as well as these blank-check companies that you’ve probably heard about, special purpose acquisition companies. And it became pretty ridiculous. At one point you had about 350 companies with a substantial market cap, over $1 billion, and yet no profits at all. So that’s a risky setup.

Today you have fewer of those companies, but still an awful lot. So it’s good news, bad news. The bad news is, there’s still a lot of rationalization that needs to play out, and there will be losses along the way, but it’s also a great opportunity for active managers to avoid those situations. The Russell 2000 has been chronically underperforming other indices, and my guess is that will continue. The Russell 2000 contains a lot of those types of risky businesses.

TWST: By comparison, it seems, at least based on your top holdings, that your portfolio is made up of, by and large, quite established companies rather than ones that are, I wouldn’t say speculative necessarily, but not as far along in their development cycle, let us say.

Mr. Walden: Yes, thank you for pointing that out. We think our companies are durable and have been around profitably for a long time. It’d be a little bit tongue-in-cheek, but I’d say we’re going to avoid any company that went public in 2021, for instance.

TWST: I understand that within your fourth quarter of 2023, the net return for the strategy was a little bit under 10%, and the year-over-year difference was nearly 42%. Are you expecting a similar kind of return within 2024?

Mr. Walden: Yeah, there’s a fair bit of luck involved in this industry, and we had a very strong run in 2023. And now continuing into 2024, we’ve been well ahead of the benchmarks. So we’re pleased to report that for our investors.

But it’s important to recognize that there’s ups and downs in the markets. There’ll be setbacks for any strategy over time, and I think it’s important to have more moderate expectations in general going forward.

For 2024 we don’t have a specific expectation for a full-year result. But since 2002, since I joined the business full-time, my experience has been to buy good companies with compelling valuations and catalysts for change, catalysts for success. Over time, if you do that on a diversified basis, things work out well.

TWST: Just quickly, are many of your holdings’ dividend payers, and is that something that you watch out for when you’re building your portfolio?

Mr. Walden: For this strategy, we’re focused on global opportunities, valuations, catalysts. We consider those other factors, including dividends, but it’s not core to what we’re trying to achieve. I would say overall, we’re sort of indifferent to dividends.

We have a terrific dividend from our investment in Golar LNG, but it’s not the essence of the opportunity. We spelled out our Golar investment thesis on our website just about six months ago, how we think the company could increase its profits by about 200% in the next four years. So if Golar can increase its profits by 200% in the next four years, more or less, we should be good. The dividend is nice to have, but it’s not essential.

TSWT: Finally, then, your strategy is only in its third year, but it launched within the peak of COVID. So here we are in March of 2024. Compared to, say, 2019, has the market changed in any fundamental ways where you feel the need to adjust your overall strategy?

Mr. Walden: The obvious important change is the interest rate backdrop. Interest rates matter now. There’s a tangible cost of capital. There’s inflationary considerations and tendencies in some parts of the economy. So candidly, I think that’s good for our fundamental-based, value-based framework.

There could be lingering inflation. I think there just may be in the economy this year, which would be, again, all else equal, good for a value-oriented approach and for hard assets, that kind of thing. So that’s one big factor that’s important to recognize versus five years ago.

But in general, I’ve been doing this since 2002, but I also studied, call it, 100 years of market history and the essence of success and failure over the past century. And like I said, I think it boils down to being opportunistic, value-oriented, quality-oriented, and then having an eye for catalysts or positive inflection points.

TWST: Just to follow up then, since you mentioned interest rates, that’d be a good segue to asking about the last of your top five holdings,American Coastal Insurance Corporation (NASDAQ:ACIC). Could you give us a bit of your reasoning behind that pick?

Mr. Walden: Sure. American Coastal is a very interesting niche insurance company in Florida. They specialize in commercial residential property insurance — P&C it’s called, property and casualty insurance — in that market. We just published a profile of American Coastal on our website.

We’re attracted to American Coastal’s long track record of profitability and good economics. Management there seems competent and well-aligned with our own interests, and the valuation is low any way you cut it. So those are the elements for success.

TWST: Thank you. (RP)

IMPORTANT DISCLOSURES

The information and statistics contained in this communication have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or forecasts discussed herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, or any non-investment related content, made reference to directly or indirectly in this communication will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. No discussion or information contained herein serves as the provision of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability above to his/her individual situation of any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal, tax, or accounting advice.