WEEK ENDING 2/23/2024

• Fed speakers lay out slow-and-steady rate policy.• Market reprices 2024 rate cuts.

• Where is the new terminal or neutral rate for fed funds?

A CITY DIFFERENT TAKE

The message from Federal Reserve speakers last week emphasized a slow and steady rate policy.

The same theme could be picked up from the minutes of January’s FOMC meeting. That meeting’s discussion on the balance sheet reduction also suggested a lack of urgency to lower rates.

The bottom line is that the Fed remains vigilant.

This has quickly seeped into the market expectations of repricing Fed rate cuts. Currently, any expectation of cuts does not materially kick in until the Fed’s June meeting with a 59% probability of a 25-basis points rate cut. Currently, the market is pricing fewer rate cuts and a higher terminal rate for 2024.

What is a terminal rate? It is the longer target rate at which economic policy is neither restrictive nor stimulating. The rate that “does nothing at all” is also called a neutral rate and is r* (r-star) in economic models. Rate estimates can be a good indication of whether the Fed’s monetary policy is accommodative, restrictive or neutra.

So why do we need to delve into this academic concept? The Fed’s policy is to be consistent with what this neutral rate should be. However, this rate remains a moving target and is less than perfect.

Come on a historical journey with us. From the mid-‘70s to 2007 the neutral rate remained between 2.5% to 4%. From 2008 to 2018, it remained below 1%. The meandering path from 2018 to 2021 saw the rate rise by 1.5% and then fall back to 0.9% in 2023.

At 5.50%, the federal funds rate would lead to a current neutral rate of 3.25% (after subtracting inflation). This is much higher and more restrictive than 0.9%. According to this logic, the U.S. economy would be in a deep recession by now.

But it isn’t.

The way to think about it is that there is a lag between fed funds and their impact on the “real economy.” The Fed is still looking for a “hard slowdown” in GDP in 2024 and 2025 to reflect the full impact of the high federal funds rate.

The point of this exercise is to show it is very hard to predict the impact of the Federal Reserve’s actions because of various economic lags. The Fed is unified (for now) in its path to go slow and to see inflation drop. To that end, it is leaving rates unchanged while it achieves “greater confidence” for its dual mandate.

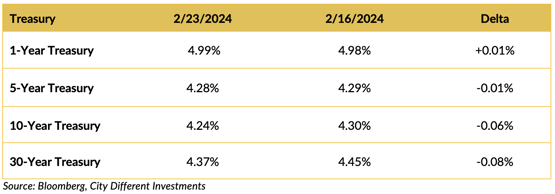

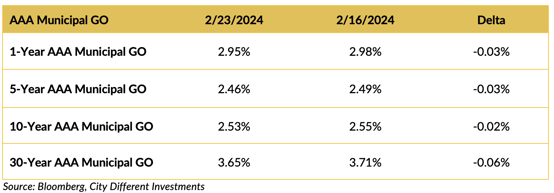

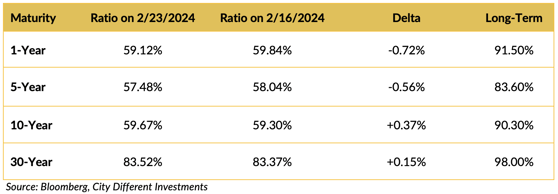

CHANGES IN RATES

Treasury rates moved marginally lower in the front end, with bigger moves in the longer end.

Municipal market yields moved in the same direction as Treasury rates, which is lower.

The municipal/Treasury ratio which is already rich decreased further during the week.

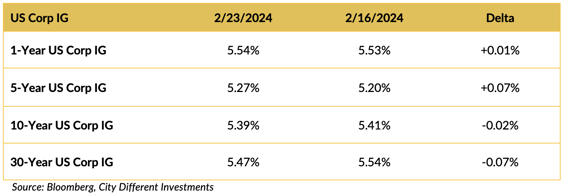

Rates in the corporate market segment were higher in the short end of the curve and lower on the long end.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Congress is back this week from recess. But is there already another threat of a government shutdown in March? As the Senate struggles to pass a budget bill, Friday marks a potential partial government shutdown. March 8 is the deadline for a full government shutdown. According to Rep. Patrick McHenry, a North Carolina Republican, "I think the odds [of a shutdown] are 50-50 at this point." Forecasting site Kalshi puts the chance of a March 4th shutdown at a much lower 23% as of this writing. We don’t like the fact that it’s even an option, but welcome to Congress.

In other political news, former President Trump seems to be rapidly moving toward the GOP nomination. His polling numbers have stayed above 40%. Meanwhile, his only opposition, Nikki Haley, lost by sizable margins in the first five contests, including her home state of South Carolina. The next significant Republican primary date is Super Tuesday on March 5.

WHAT, ME WORRY ABOUT INFLATION?

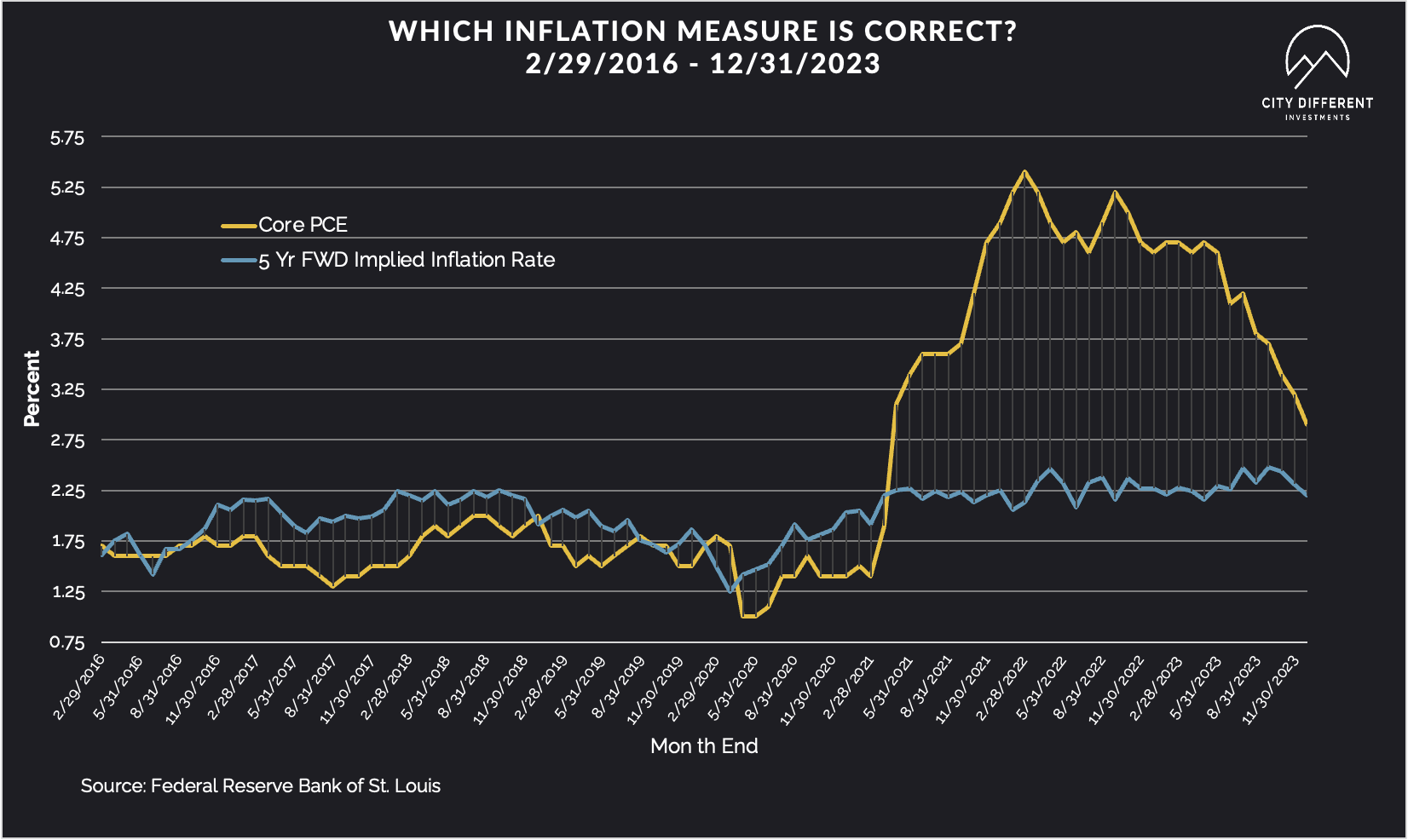

The 5-year Breakeven Inflation Rate finished the week of February 23 at 2.26%, twelve basis points lower than the February 16 close of 2.38%. The 10-year Breakeven Inflation Rate finished the week at 2.30%, three basis points lower than the close of February 16.

MUNICIPAL CREDIT

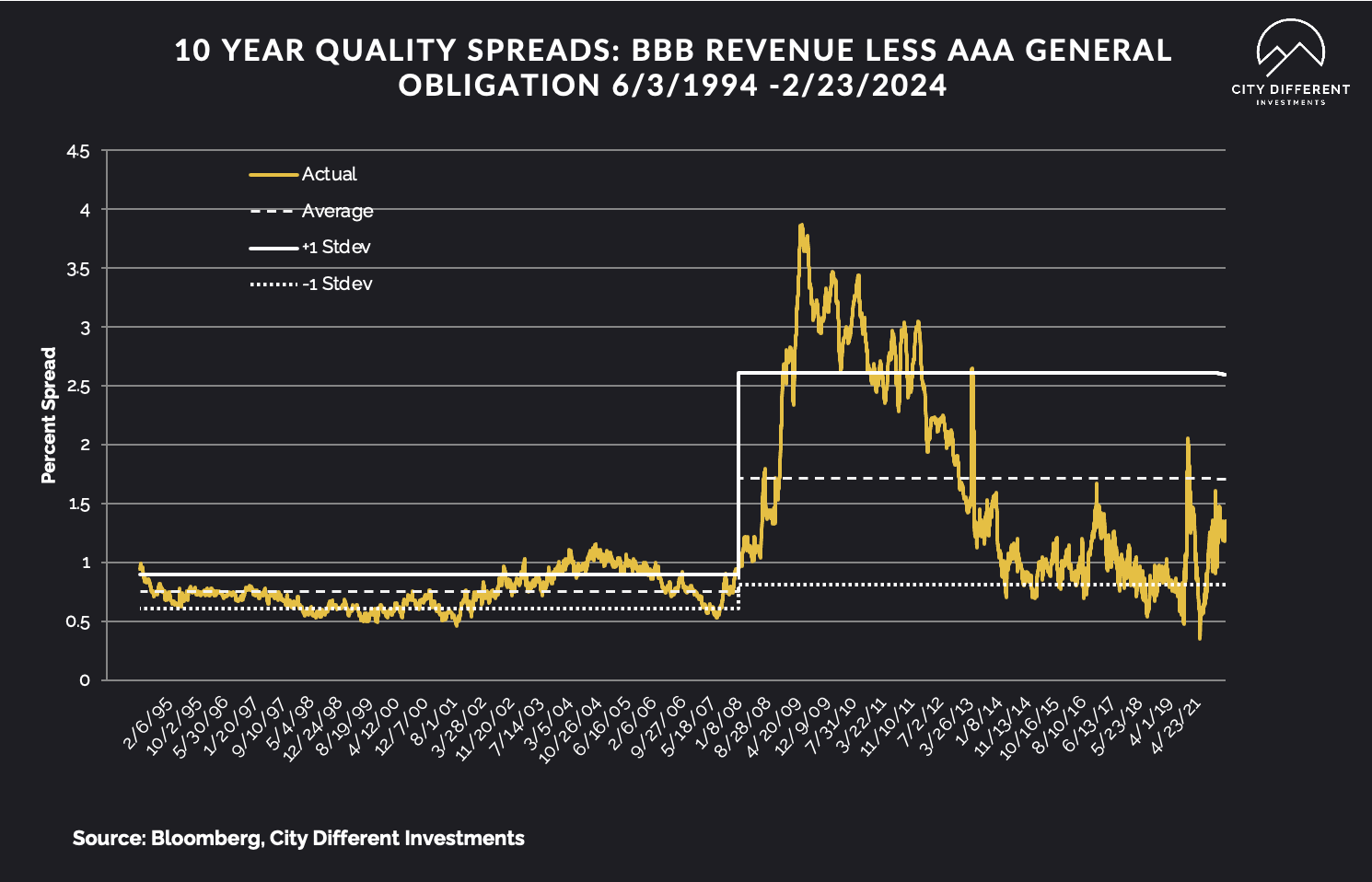

10-year quality spreads (AAA vs. BBB) as of February 23 were 1.70%, ten basis points higher than the February 16 reading of 1.60% (based on our calculations). The long-term average is 1.71%.

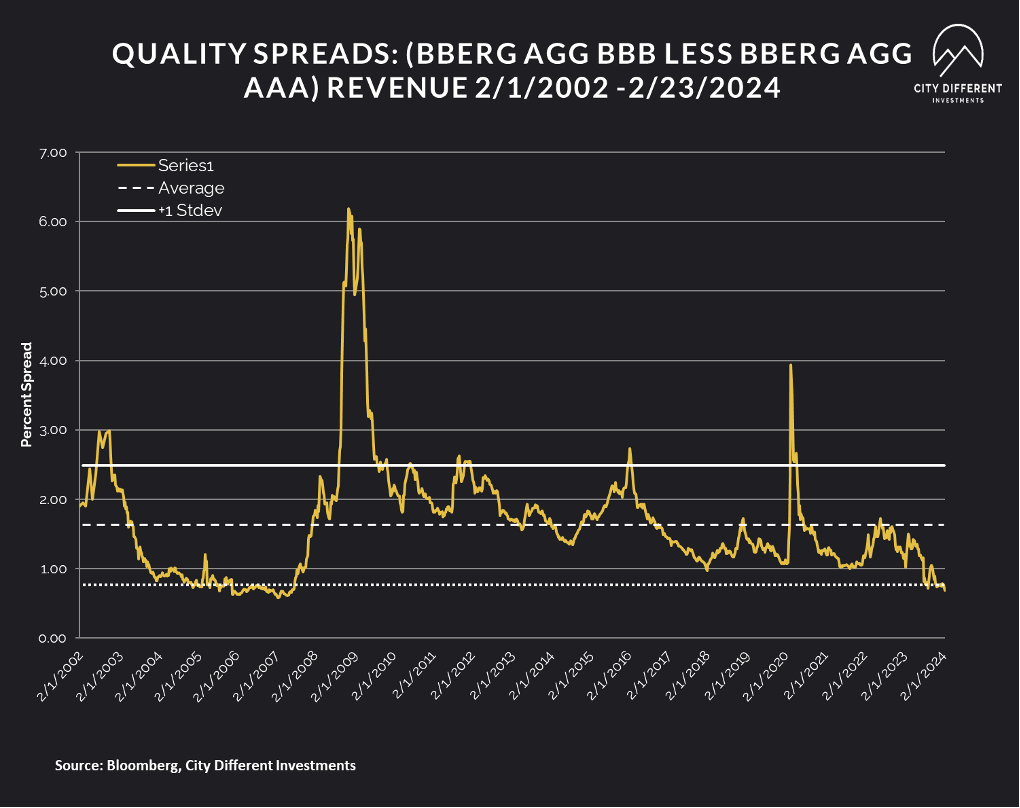

Quality spreads in the taxable market are not attractive but were lower by 3 basis points at 0.68% from last week. High-yield quality spreads on February 23 were at 2.87% versus 2.95% last week.

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

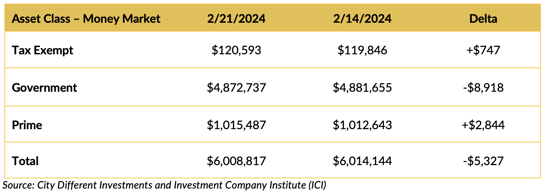

Money Market Flows (millions of dollars)

Money market funds saw lower flows last week driven largely by government money markets.

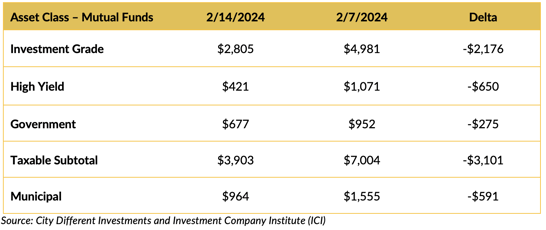

Mutual Fund Flows (millions of dollars)

Bond funds saw lower inflows in almost all bond offerings.

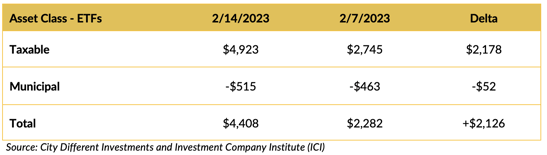

ETF Fund Flows (millions of dollars)

Positive weekly net issuance in the ETF space for taxable bonds and a drop, with net outflows in the municipal space.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

The calendar this week is expected to be around $7.8 billion. Spreads in the municipal market have been really tight, and the increase in supply should be a good test for the market.

CONCLUSION

With regard to rate cuts, the Federal Reserve is nearly unified in its messaging of patience. The market has repriced rate cuts for 2024, with, according to the options market, the first cuts starting in June.

Currently, the market is pricing fewer rate cuts and a higher terminal rate for 2024. An academic consideration of the neutral rate is less than perfect as the varied and lagged effect of a tight monetary policy still makes its way into the economy.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.