WEEK ENDING 12/15/2023

- Holiday markets rally after turtle-dovish message from Fed.

- Fed hints tightening finished; cuts to come.

- Dot plot changes significantly.

- Happy holidays to you, and a fantastic New Year!

A CITY DIFFERENT TAKE

At its last meeting of the year, the Federal Reserve paused rate hikes again while Chair Powell struck a surprisingly dovish tone, mentioning that the committee has discussed when to begin lowering the fed funds rate.

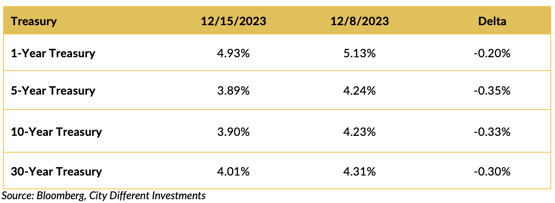

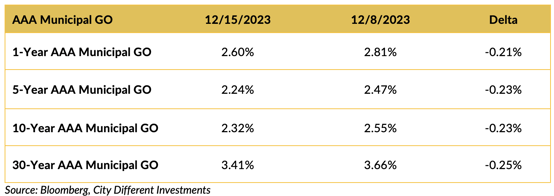

This only added fire to an already-rallying fixed income market. The two-year was down 0.27%, while the 10-year was down 0.16% (a bull steepener). Municipal bond rates were lower, but lagged the move in the Treasury market (2-year AAA down 0.03%, 10-year AA down 0.03%). The rally continued within 10-year securities. Treasury yields fell to 3.92%, and the 10-year AAA Muni yield dropped to 2.32%.

This rally drew strength from the apparent pivot by the Fed from a tightening regime to a potential easing regime. The markets, both fixed income and equity, seemed to be priced for perfection. We at CDI are big believers in the old saw that, “if it seems too good to be true, it probably is.”

The other key takeaway from the Fed’s meeting was the message that tightening is finished and cuts are on the way. Remember, the Federal Reserve does not directly announce a cut. The Fed signals a pause with language indicating a future cut is about as likely as a future hike. Powell may decide to be more explicit. (He tends to be more verbose in his guidance about the Fed’s plans compared to past Fed chairs.) The message delivered at last Wednesday’s press conference is already very close to this traditional Fed-on-hold signal.

Lastly, we want to bring attention to how significantly the Fed’s dot plot has changed. The 2023 consensus fell because the year ended before the FOMC could hike. More importantly, 2024 averages are between 4.25% and 5%. This is a tight range, considering the year has not yet even begun. Interestingly, the 2024 median forecast has dropped 50 basis points to 4.63%. The 2025–26 dots dropped and consolidated, too, despite one high holdout. The dots’ tight dispersion suggests a great deal of confidence that inflation is falling and will continue to fall.

CHANGES IN RATES

The rally in Treasury yields reflects the market’s belief that tightening is behind us and we can look forward to 2024 rate cuts.

This week, both fixed income markets showed big moves. The municipal market continued to rally along all tenors on the curve, much like the Treasury market.

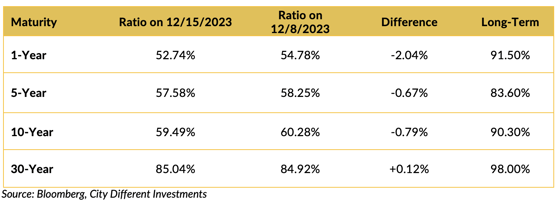

The municipal/Treasury ratios reflect the wild ride in rates. Ratios are lower for 1, 3, 5, and 10-year maturities (and marginally higher for 30 years).

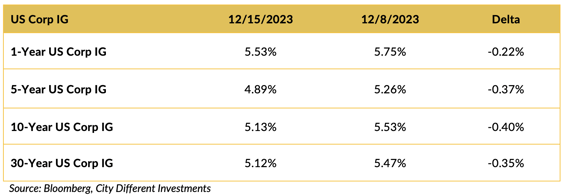

Corporate yields moved lower last week; corporates mostly followed suit with the rally in the Treasury market.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

White house economic advisor Lael Brainerd is echoing the sentiment that inflation is dropping and poised for drop further. In a call with reporters, she spoke about supply chain pressure easing. President Biden has lost points with the public on his handling of inflation and it is sure to be an issue in the 2024 general election. Ms. Brainerd said that the President will continue to look for ways to use legislation he’s signed to fight price growth.

This sentiment is echoing throughout the administration. Treasury Secretary Janet Yellen mentioned along similar lines that the U.S. economy is on the path to a soft landing.

In other Washington news, the House has passed an impeachment probe with regards to President Biden. This is after his son, Hunter Biden, defied a congressional demand to testify.

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.20%, eleven basis point lower than the December 8 close of 2.31%. The 10-year Breakeven Inflation Rate finished the week at 2.22%, one basis point higher from the December 8 close.

Inflation looks tame and that is the reason for the rally last week. The market (as measured by Bloomberg’s WIRP function) is implying a 79% probability of significant easing in March of 2024 and a 102% probability by June. The Bloomberg U.S. financial conditions index reached +0.55 on December 13, up from -0.30 on October 30. (Positive numbers indicate accommodative financial conditions and negative numbers indicate restrictive financial conditions.) Last week’s releases show a stable consumer (retail sales m/m are +0.3% compared to a revised -0.2% last month and expectations of -0.1%). Initial jobless claims came in at 202,000 versus last month’s revision of 221,000 and expectations of 220,000.

MUNICIPAL CREDIT

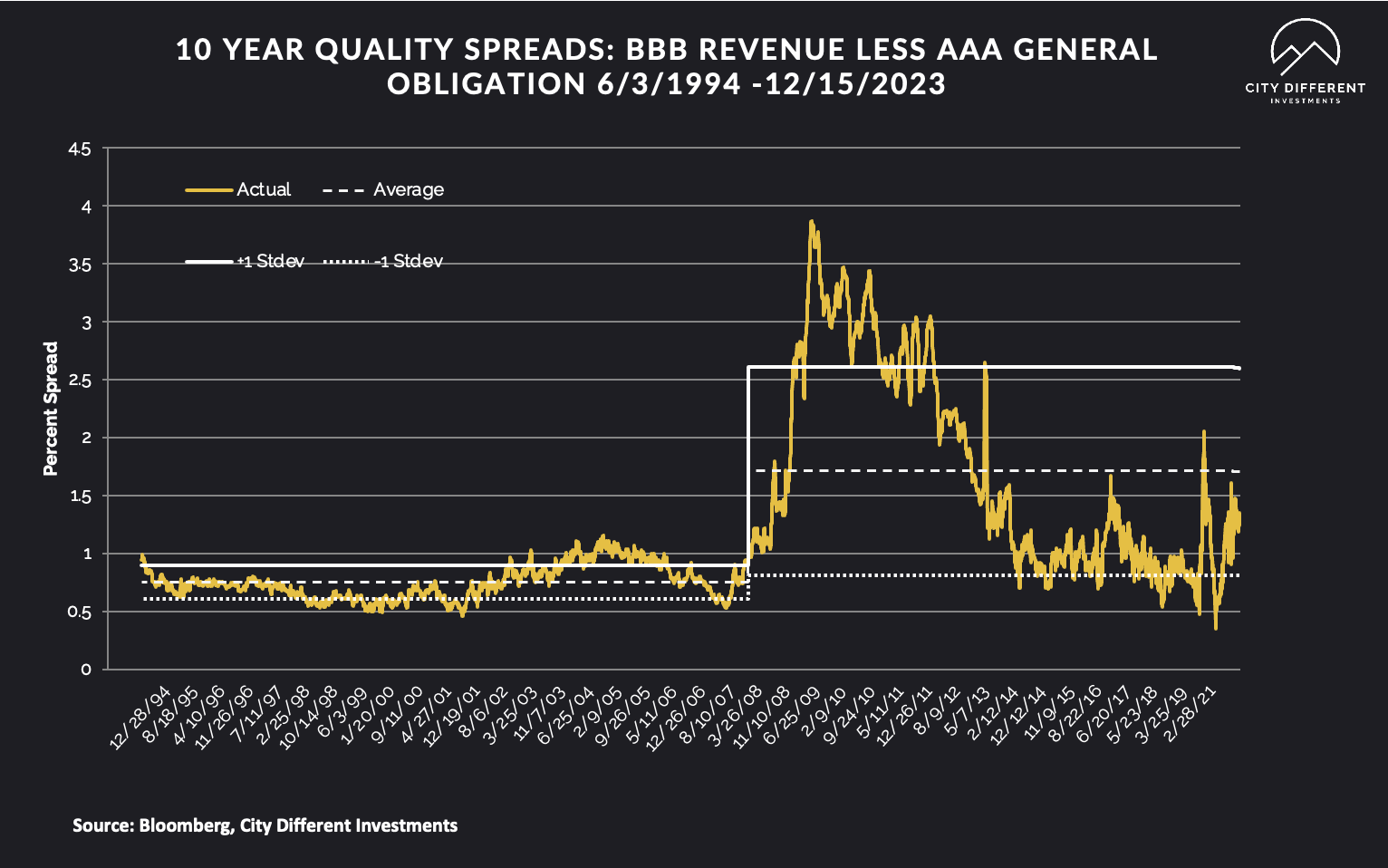

10-year quality spreads (AAA vs. BBB) as of December 15 were 1.37%, two basis points higher from the December 8 reading of 1.35% (based on our calculations). The long-term average is 1.71%.

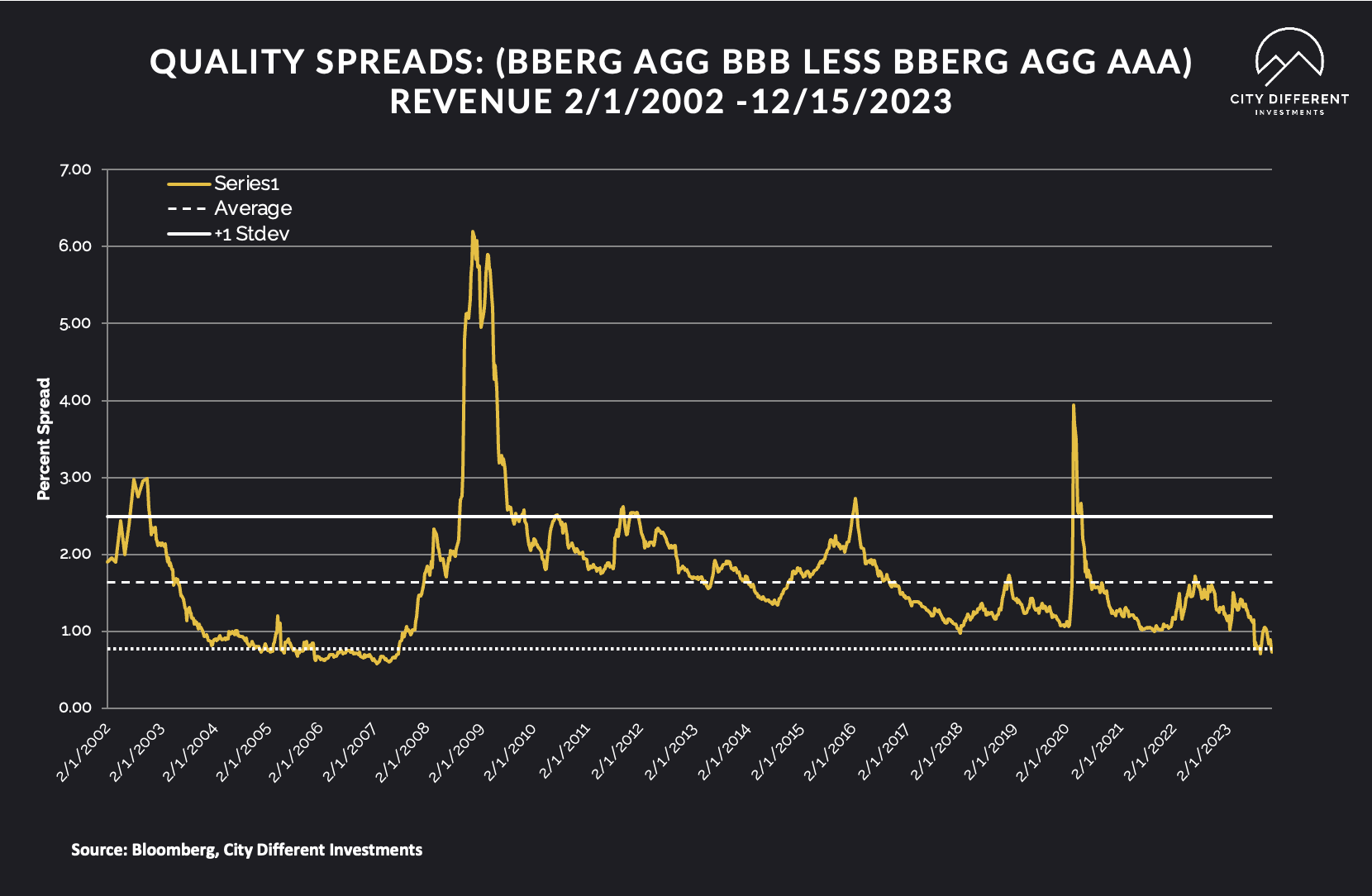

Quality spreads in the taxable market are not attractive but were wider by a few basis points last week, ending the week at 0.75%. High-yield quality spreads moved from 3.26% on December 15 to 3.44% on December 8.

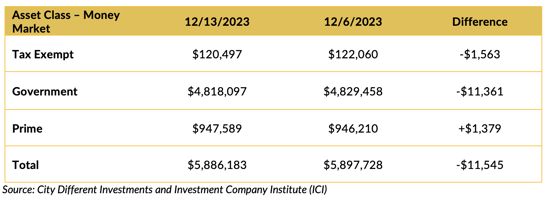

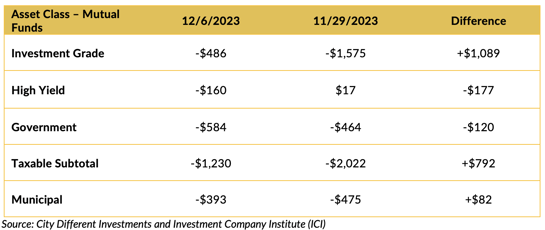

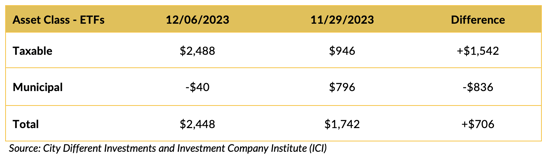

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Mutual Fund Flows (millions of dollars)

ETF Fund Flows (millions of dollars)

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Supply for municipal tax-exempt calendar will remain uneven for the next few weeks going into year end. This week’s municipal tax-exempt calendar totals only $1.5 billion in new issuance.

CONCLUSION

This week the message was clear to the market. A dovish Fed has arrived, inflation is somewhat under control, and rate hikes are done and dusted. The fixed income market massively rallied reflecting the hopes of rate cuts ahead for 2024. The market is slowing down for year end with dwindling supply — and so are we. We won’t be publishing our weekly commentary until January 8 as we take a break to observe the holidays.

We hope you all softly land into a happy 2024!

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.