WEEK ENDING 10/13/2023

- Rising geopolitical risk adds another consideration for the Federal Reserve.

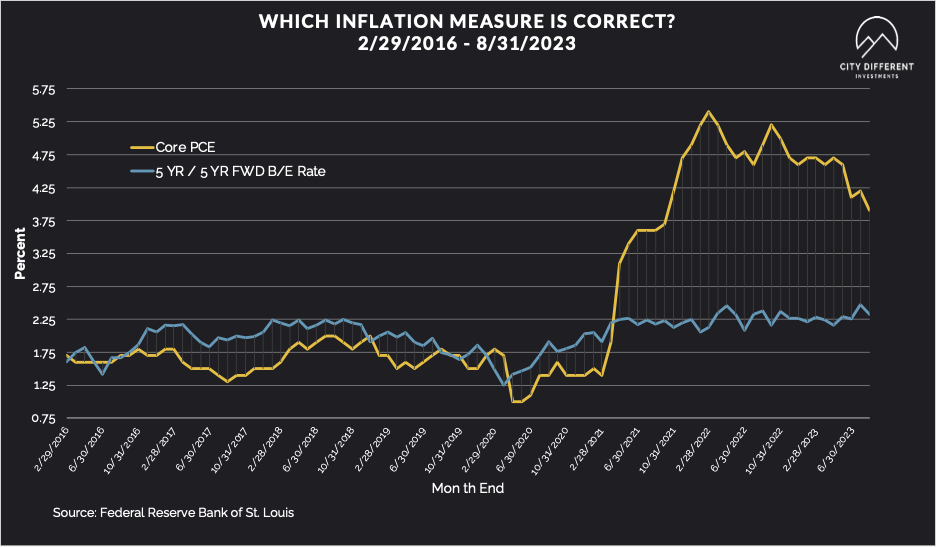

- Supercore inflation is double the Fed's target.

- Yields rise in long end of the curve; tightens financial condition.

A CITY DIFFERENT TAKE

The week before last was all about higher rates due to uncertainty. Last week was about flight to quality in both the Treasury and municipal markets.

Both weeks witnessed a big reversal in the direction of rates, reflecting the state of risk in the market. Now the Federal Reserve must contend with changes in macroeconomic indicators and tremendous geopolitical risk. (The safe-haven trade was a consequence of this risk.)

The Federal Reserve has hiked rates through the course of the war in Ukraine as well as the banking crisis. We do believe, however, that the biggest difference between now and past events is that the Fed is heading toward the end of its tightening cycle.

The other uncertainty is inflation itself. CPI rose 0.4% in September. Owners’ equivalent rent (the biggest component of CPI) rose by 0.6% to its highest level since February. “Supercore” is the new favorite measure for the Fed. Remember, supercore inflation comprises the price of services, excluding energy and housing. Supercore rose by 0.44%. This Is worrisome as the Fed was focused on lower supercore inflation. Supercore is running at about twice the Fed's target.

As we contemplate another rate increase, let’s talk about the long end of the yield curve. The long end has been relentless in its climb for yield. Higher yields tighten financial conditions. Think auto loans, mortgages, etc., that all reside at the long end. Higher long end rates could point to the possibility that the Fed does not need to increase rates since the long end yields are tightening financial conditions for them. The economic impact of the long end rising will take time and goes back to the adage that the lags of monetary policy are long and varied.

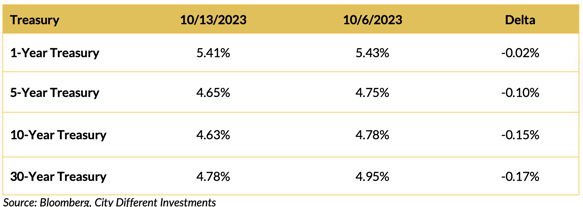

CHANGES IN RATES

The yield curve inverted more, from -0.30 to -0.41, while Treasury yields moved lower on the week. Increasing conflict in the Middle East is leading to a flight to quality and lower Treasury rates. Sprinkle in some chaos in Congress for good measure. The House went home for the weekend without electing a speaker. We guess that given all the labor unrest, their contract has a no-overtime clause. We know they still get paid if the government shuts down. Nice work if you can get it. Friends, how would that play with your employer? Wait, we are their employers. Fire the bums!

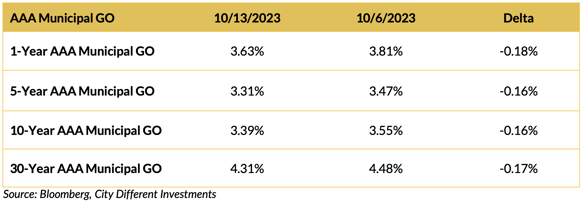

The municipal bond market outperformed the Treasury market last week as muni yields moved much lower than their Treasury equivalents. The reasons for the move are the same as for the Treasury market. But given the low supply holiday week, the picture is complete. Next week's supply looks to be about $10+ billion.

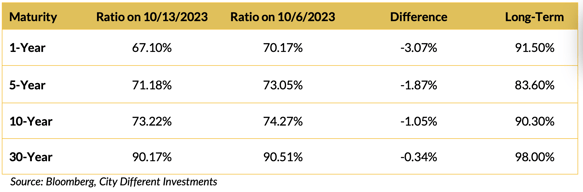

The municipal/Treasury ratios were lower across the board, as the municipal market adjusts to the unique challenges facing it.

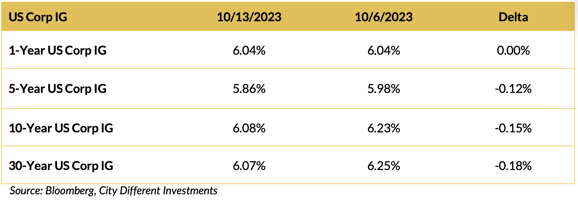

Corporate yields moved lower last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Washington is focused on containing geopolitical risk. To that end, President Biden is considering a trip to Israel in hopes of reducing the risk of a war spreading throughout the Middle East. According to Bloomberg, the U.S. has been in “back-channel talks” with Iran to prevent any escalation.

President Biden also announced that the U.S. can support Ukraine and Israel and still maintain its own defenses.

Treasury Secretary Janet Yellen supported the sentiment that the U.S. economy is strong enough to support Israel with aid in its conflict with Hamas. The interest on U.S. debt stands at 98% of the economic output and “remains manageable,” according to Sec. Yellen. With a $2 trillion budget deficit, the Treasury secretary does not find the fiscal situation “unsolvable.” We commend her enthusiasm but are not believers that the deficit problem as it stands currently, is solvable.

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.45%, flat versus the October 6 close of 2.45%. The 10-year Breakeven Inflation Rate finished the week at 2.34%, three basis points higher than the October 6 close.

MUNICIPAL CREDIT

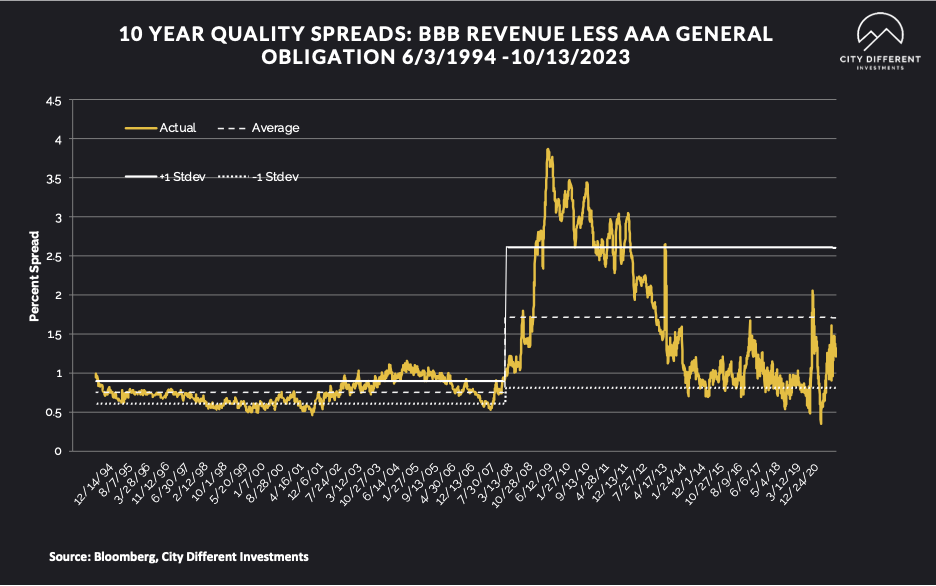

10-year quality spreads (AAA vs. BBB) as of October 13 was 1.26%, six basis points lower from the October 6 reading of 1.32% (based on our calculations). The long-term average is 1.71%. By our way of thinking, we still believe lower-quality securities are not attractive. Municipal market credit spreads usually take a little more time to adjust, given a significant baseline market revaluation.

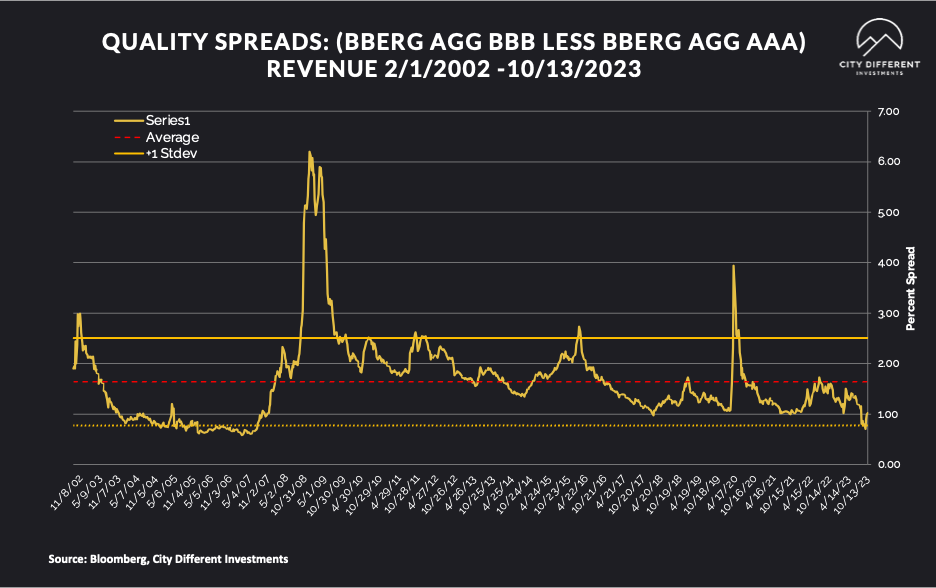

Quality spreads in the taxable market are not attractive but were wider last week, ending the week at 1.02%. High yield quality spreads moved from 3.70% on October 6 to 3.63% on October 13.

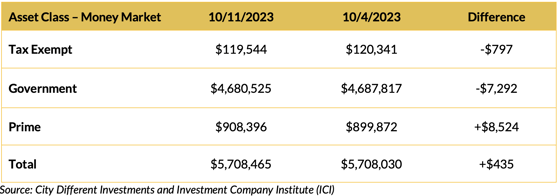

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money funds, in total, saw mixed cash flows last week.

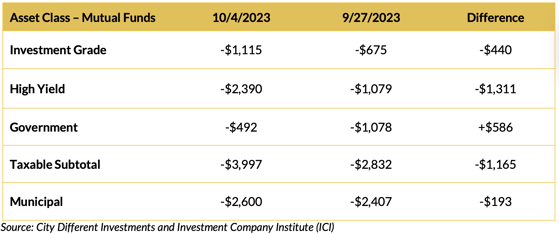

Mutual Fund Flows (millions of dollars)

Cash flows for bond mutual funds were negative across the board.

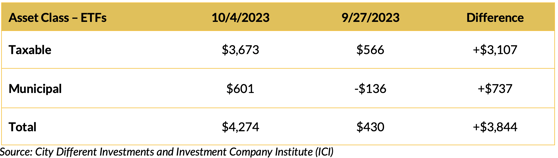

ETF Fund Flows (millions of dollars)

ETF flows were positive last week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $10+ billion.

SUPPLY OF NEW ISSUE INVESTMENT GRADE BONDS

The investment grade market has been abuzz with deals. Currently, YTD investment grade supply is running 0.9% ahead of the same period in 2022 ($1,031.4 billion versus $1,021.9 billion). Industrial issuance is up 24.6% from last year, while FIG issuance is down 17.0%. Utility issuance is up 25.4%.

CONCLUSION

We are currently facing tremendous geopolitical uncertainty. President Biden, however, is committed to supporting both Israel and Ukraine. Treasury Secretary Yellen declares the U.S. deficit isn’t completely “unsolvable.”

On the market side of things, supercore inflation was disappointing for September. But the Federal Reserve might not have to raise rates as the long end of the yield curve is helping the Fed by tightening financial conditions.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.