WEEK ENDING 1/5/2024

- We hope everyone had great holidays!

- Fixed income and equity markets continued year-end rallies.

- Realism befalls the markets in the first days of 2024.

A CITY DIFFERENT TAKE

The markets have moved on from the holidays with a new sense of realism overcoming participants. A healthy JOLTS number was released, followed by a jobs report that beat expectations (216,000 versus 175,000, though revisions were less comforting). The unemployment rate held steady at 3.7%. Month-over-month and year-over-year average hourly earnings also beat expectations (0.4% versus 0.3% M/M; 4.1% versus 3.9% Y/Y).

The market implied probability of a rate cut, and the magnitude of that cut lost some of its holiday enthusiasm (see below). It’s hard to think of 6 rates cuts in the first 3 months of 2024 when financial conditions (as measured by the Bloomberg US Financial Conditions Index) are the most accommodative that they were in all of 2023. (Note – a positive value indicates accommodative financial conditions, while a negative value indicates tighter financial conditions.)

Source: Bloomberg

We get the first inflation reading of the new year on January 11 and we expect 2024 will be a volatile year.

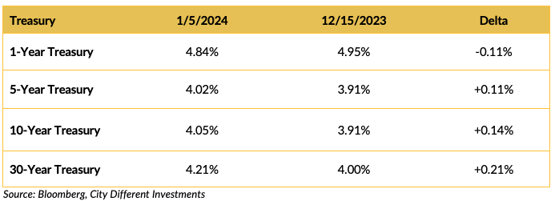

CHANGES IN RATES

The rally in Treasury yields continued through year-end, with the 10-Year Treasury security hitting 3.88% before backing off in the first week of 2024. On the last day of trading in 2023, the market priced in an 84.3% probability that the Fed would reduce short-term rates by 1.00%; as of the close of business Friday, that probability was 66.8%, and the rate reduction was 0.73%.

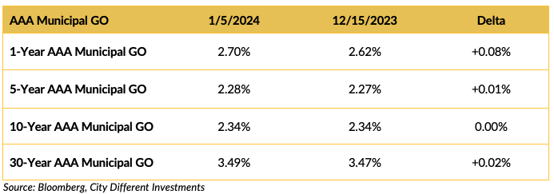

The municipal market outperformed the Treasury market in all maturities except 1-year. The “January Effect” continues. The next question is, “When will it subside?”

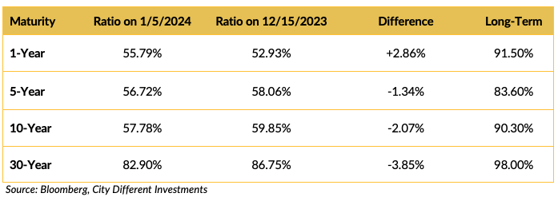

The municipal/Treasury ratios reflect the impact of the “January Effect.”

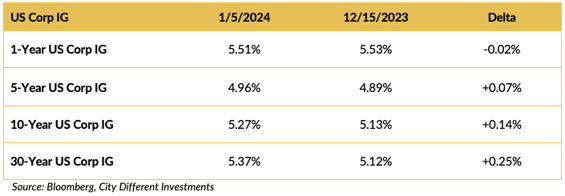

Corporate yields followed Treasuries higher last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

It’s an election year. God help us! President Biden started his re-election campaign on Friday. The Iowa caucuses are days away, as is a potential partial government shutdown.

Congress is still out on vacation, except for a partial class trip to the southern border.

And now for some observations from Chris while on the road this holiday break:

I am a very skeptical person by nature. I tend to have a biased opinion of my fellow humans. But when I come back from driving across the country, that bias is challenged. My daughter, her dog, and I have driven across the country 4 or 5 times, stopping in various cities — Kansas City, St Louis, Cincinnati, Columbus, Tulsa, Oklahoma City, Nashville, and Charlottesville. Here are some of my observations from these trips:

- This is a beautiful country.

- Many trucks are on the road, and, in the west, the freight trains are double stacked with containers.

- Family ranking of gas stops along the way: Pilot is 1, Loves is 2, and all others are 3.

- Holding a door for someone, smiling, and saying please and thank you is, more times than not, reciprocated. There is much more that binds us together than separates us.

So, when I come back from these trips, I realize that my bias may be too harsh. Americans have a lot in common, so it makes me question our deep political division. Then, I turn on the Sunday morning news/interview shows to find politicians doing nothing but trying to divide. Question answered.

With public trust in institutions suffering and partisan media outlets fueling the deterioration of that trust, something has got to change. Americans need to do more to build bridges, put a stop to blaming the other side, and align our nation. We’re all Americans – even those jerks who park next to the gas pumps and go shopping inside the station.

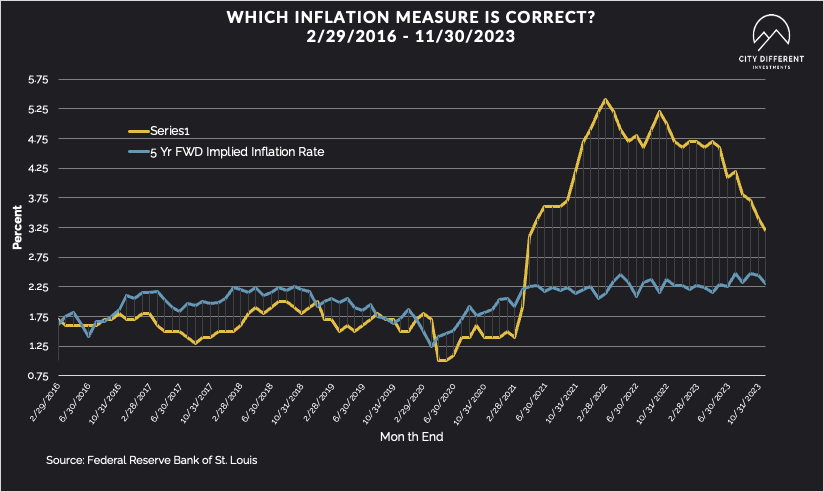

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week of January 5 at 2.25%, two basis points lower than the December 15 close of 2.27%. The 10-year Breakeven Inflation Rate finished the week at 2.22%, the same as the close of December 15.

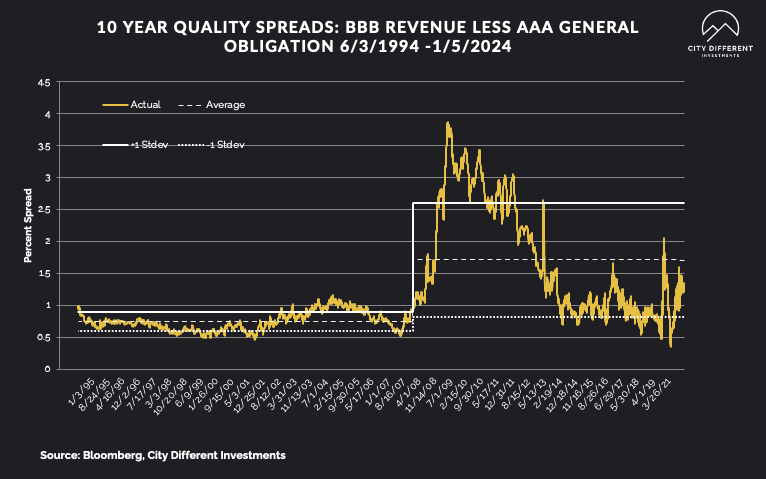

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of January 5 were 1.21%, nine basis points lower from the December 15 reading of 1.30% (based on our calculations). The long-term average is 1.71%.

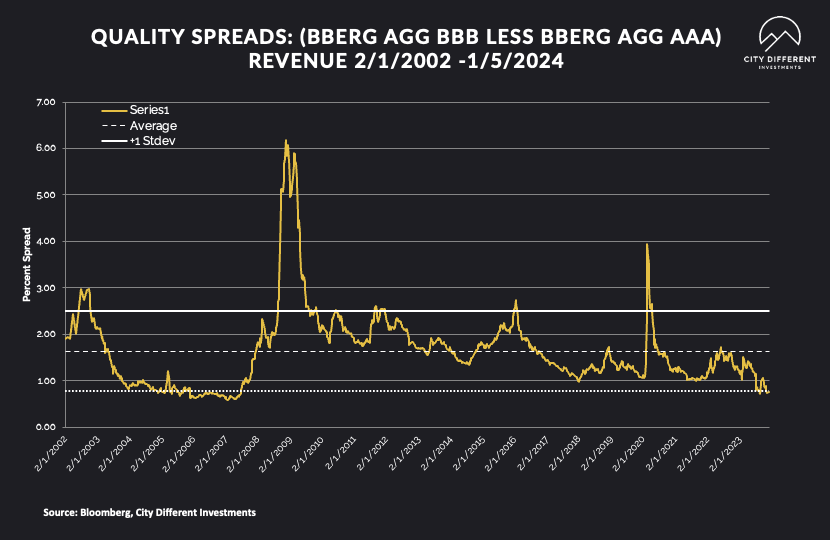

Quality spreads in the taxable market are not attractive but were wider by a few basis points last week, ending the week at 0.76%. High-yield quality spreads were 3.26% on January 5.

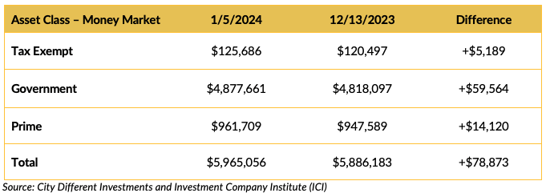

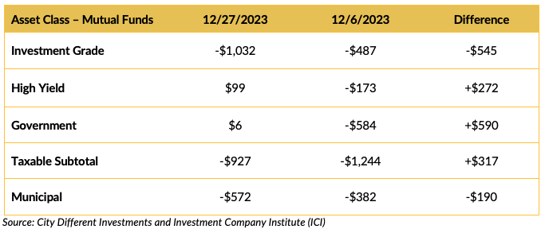

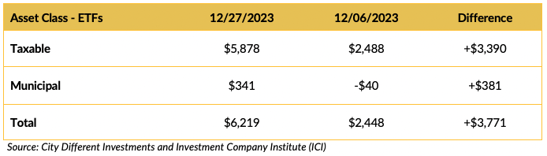

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds are attracting significant assets. Beware the “Cash Trap”!

Mutual Fund Flows (millions of dollars)

ETF Fund Flows (millions of dollars)

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Supply for municipal tax-exempt calendar will remain uneven for the next few weeks coming out of year’s end. Estimates for this week’s municipal tax-exempt calendar totals only $8.9 billion in new issuance.

CONCLUSION

The fixed income markets seem to be shaking off the holiday views of expected Fed moves in the early part of 2024. The municipal market has outperformed its taxable equivalents but that may be short-lived if new issuance supply begins to build.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.