WEEK ENDING 1/26/2024

- GDP and core PCE data trends in the right direction.

- Fed meets this week with no expectations of rate cuts.

- Hong Kong judge orders China’s Evergrande to liquidate.

A CITY DIFFERENT TAKE

Speculation on the Federal Reserve cutting rates this week currently stands at 2.5% probability. So, even though we are not expecting a rate cut this Wednesday, the market is expecting some guidance on the path of rates for the year. Federal funds future is still betting on a 45% probability for a rate cut in March. This is not the same as definitive language from the Fed communicating a rate cut path.

The FOMC median expectation (from its dot plot) is for three rate cuts in 2024. Even though the market has suggested six cuts, the confirmation here is not in the number of rate cuts but the directionality of interest rates. The mismatch in the market’s expectation and the actual pace of the interest cuts creates opportunities in the fixed-income market as entry points.

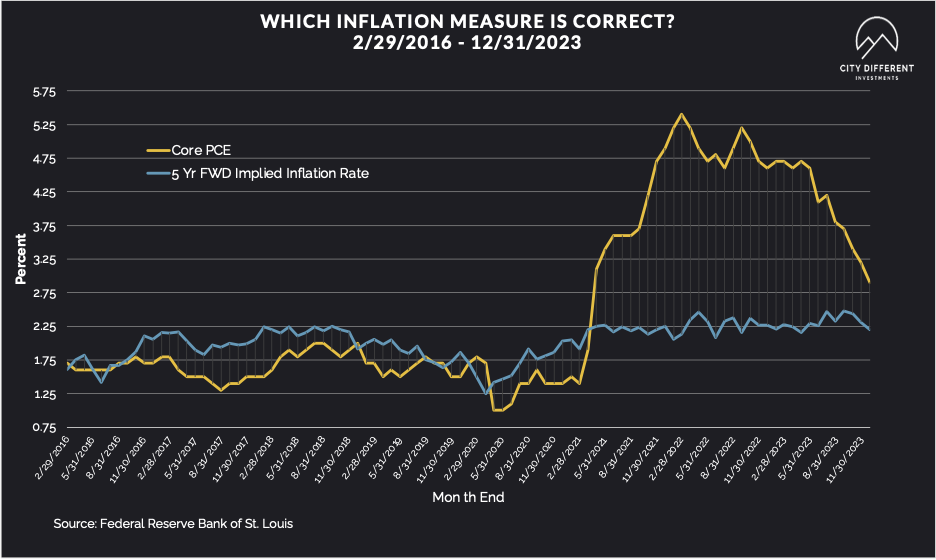

The Fed has told us that the current real Fed funds rate is high enough or nearly high enough to achieve its mandate of 2% inflation. Supporting a case for a no-landing/soft-landing scenario is December’s core PCE inflation number. 2.9% for core PCE is the lowest inflation number since April 2021. This is a comforting number for both the Fed and the markets to close out the year. Both headline PCE and core PCE inflation rose 0.2% in December, as expected.

On Wednesday, all eyes will be on the Fed’s communication of its rate cuts and tapering of quantitative tightening.

If the Federal Reserve goes down the rate-cut path, it would be unusual in a healthy economic environment with strong GDP and labor conditions. We also saw an economic release of strong U.S. GDP for Q4 2023 at 3.3% driven by strong consumer spending. Growth remains robust.

The debate that the Federal Reserve has to balance is that if inflation is now in the acceptable range, a higher interest rate policy is restrictive. Yet, at the same time if the economy is functioning at strength, does it mean the market is demonstrating that it can tolerate higher rates?

Finally, in global economic news, Evergrande, once the largest property developer of China, was asked to liquidate by a Hong Kong judge. This will clearly have ripple effects across China’s beleaguered real estate market. It will be key to see if mainland China (which follows a separate legal system than Hong Kong) will come to the same decision. Internationally, this case has significance to see if China’s investors/creditors come second to the Communist Party.

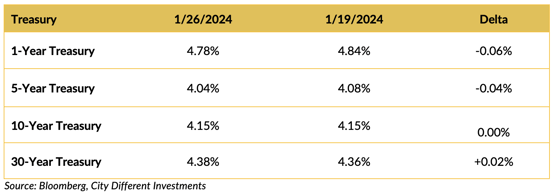

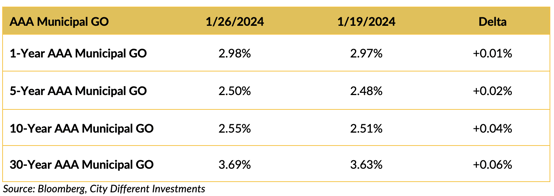

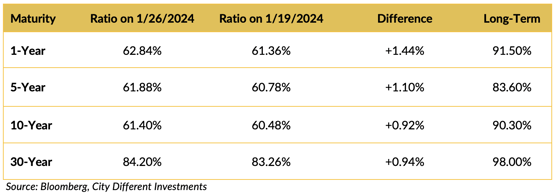

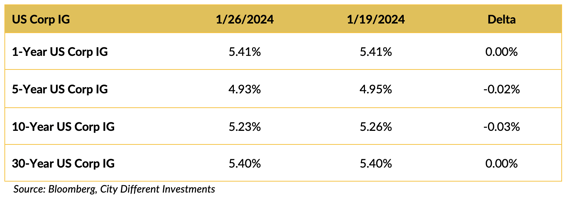

CHANGES IN RATES

Treasury market yields “wobbled” last week. Short rates decreased, and long rates increased (10-year rates were unchanged). The rate changes were not significant, but they do hint at the risks of the “Cash Trap.”

The municipal market meandered last week; one-year rates were slightly lower, and longer rates were slightly higher.

The municipal/Treasury ratios increased (municipal bonds became less expensive) during the week. It’s about time, and not surprising with the end of January approaching. They are still past the breakeven rate versus their Treasury equivalents.

Another meandering market segment. The credit market remained somewhat firm and the same in terms of rates for week over week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

The world stage grows grimmer. Three U.S. soldiers were killed over the weekend during a drone strike on an American base in Jordan. Iran is backing away from any involvement in a proxy war. President Biden is facing pressure to launch a counterstrike against Iran.

Meanwhile, the presidential primary moves on to South Carolina. After big wins in Iowa and New Hampshire, former President Donald Trump faces Nikki Haley in her home state. Hayley lags in the polls but the Republican National Committee recently pulled a resolution to consider declaring Trump the party’s “presumptive 2024 nominee.”

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week of January 26 at 2.34%, four basis points lower than the January 19 close of 2.38%. The 10-year Breakeven Inflation Rate finished the week at 2.30%, four basis points lower than the close of January 19.

MUNICIPAL CREDIT

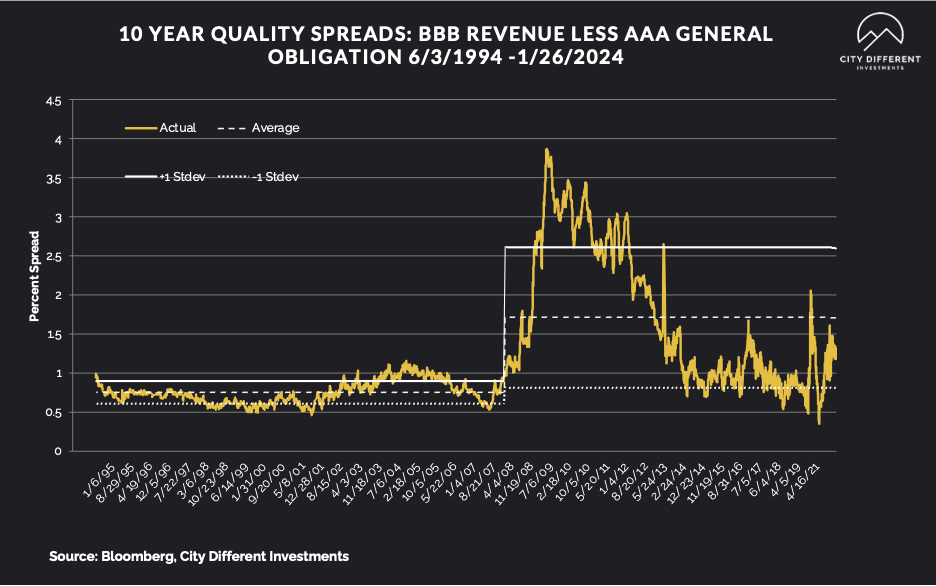

10-year quality spreads (AAA vs. BBB) as of January 26 were 1.18%, six basis points lower than the January 19 reading of 1.24% (based on our calculations). The long-term average is 1.71%.

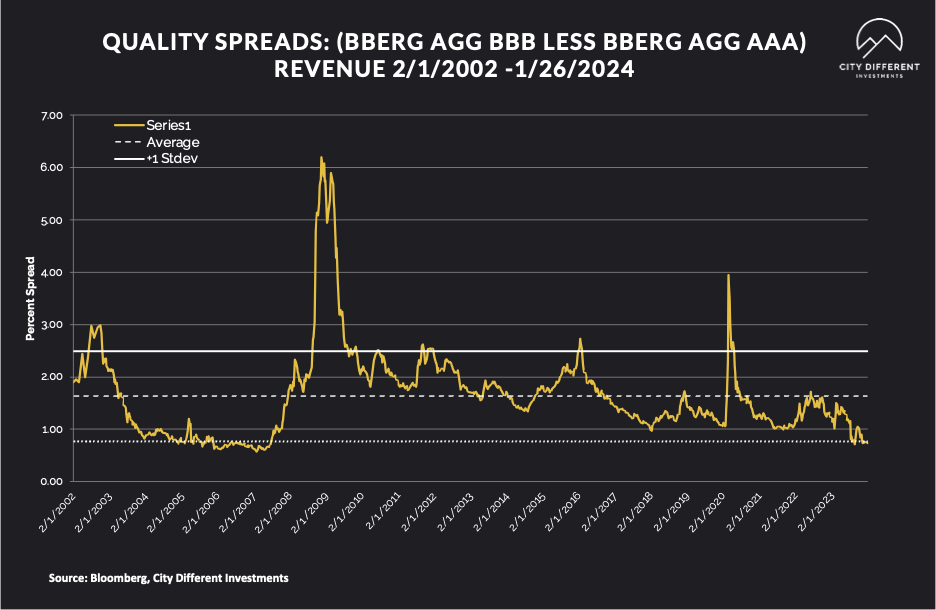

Quality spreads in the taxable market are not attractive but were unchanged (kind of), ending the week at 0.74%, one basis point lower than last week. High-yield quality spreads were 3.06% on January 26.

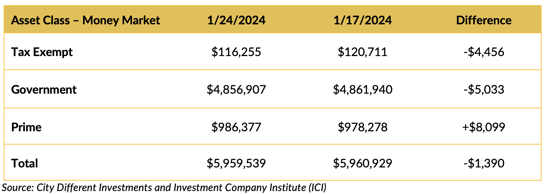

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds flows reversed last week for all categories other than Prime.

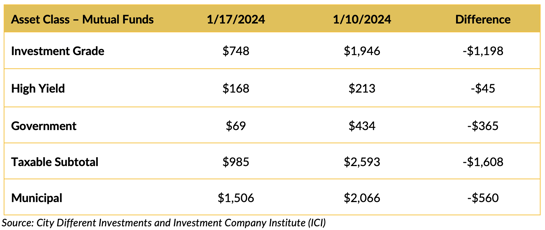

Mutual Fund Flows (millions of dollars)

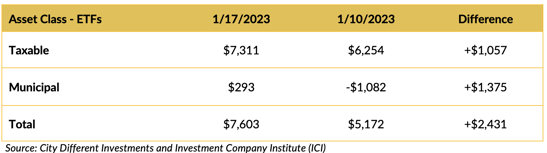

ETF Fund Flows (millions of dollars)

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Supply for the municipal tax-exempt calendar will likely remain uneven for the next few weeks at the start of the new year. This week’s municipal tax-exempt calendar estimates are $4.1 billion in new issuance.

CONCLUSION

All eyes are on FOMC this week, seeking guidance from the Federal Reserve. The markets are poised for communication on easing of quantitative tightening and a path for rate cuts. A Hong Kong court’s decision on Evergrande is being watched closely by international investors to see if investor claim has sovereignty over Chinese communist party agenda. Finally, a grim scenario grows as Iran distances itself from attacks on American soldiers in Jordan.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.