WEEK ENDING 1/19/2024

- Year-end wishful thinking dissolves, and it’s about time.

- Probabilities fade for significant March rate cuts.

- The voters of Iowa have spoken.

A CITY DIFFERENT TAKE

As we finish up the third week of the new year, more realistic views of potential rate moves are coming into focus. Recent economic releases show that the economy is moving along at a reasonable pace and jobs are plentiful despite recently announced tech job cuts.

Most of the data releases beat estimates. Retail sales were 0.6% compared to 0.4%. University of Michigan consumer sentiment came in at 78.8 versus 70.1. And topping them all, initial jobless claims were 187,000 versus 70,100.

Couple these releases with statements from some Federal Reserve governors that chilled future rate-cut expectations and, as of January 19, the market-implied probability of a 50 bps move in the Fed Funds rate is now 46.5%. Compare that to an 85.3% probability of a 100 bps move by March (reported on December 20).

President Biden signed a short-term funding extension (the same responsible kind of thing that lost Kevin McCarthy his job).

“In a rare event, lawmakers had been confronting not one but two government shutdown deadlines on January 19 and February 2. The short-term funding extension sets up two new funding deadlines on March 1 and March 8.”

Not quite the Ides of March, but close.

The Middle East is a hotbed of unrest and the shipping channels in the Red Sea are not safe, forcing much of the world trade goods to take a longer and much more expensive route to market. This could be a factor influencing future inflation.

CHANGES IN RATES

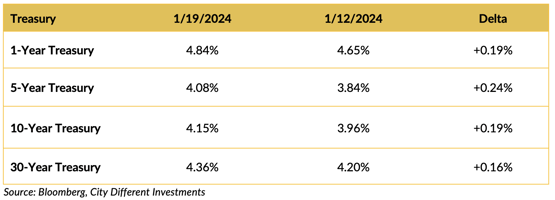

Treasury market yields moved higher in the shortened holiday week.

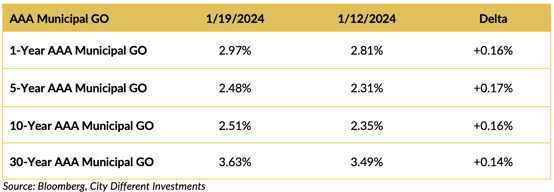

The municipal market followed the Treasury market higher in yield. Except for the 30-year maturity, most maturities are still not attractive on a tax-adjusted basis versus their Treasury equivalents. The “January Effect” continues!

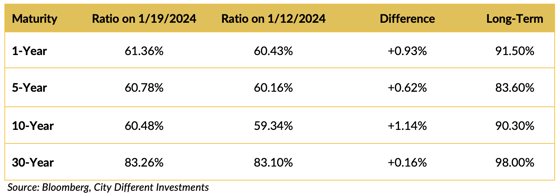

The municipal/Treasury ratios increased (municipal bonds became less expensive) during the week. They are still past breakeven rate versus their Treasury equivalents.

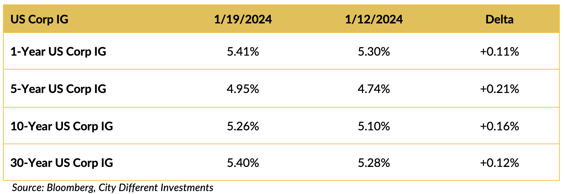

Corporate yields followed Treasuries higher last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

The voters of Iowa have spoken. On to New Hampshire. The former president’s momentum is very impressive. We will see if any convictions hurt the “Big Mo.”

As mentioned earlier, Congress has come up with another short-term spending plan to avert a government shutdown. Seems like the House of Representatives are more concerned with giving the president a “win” than effectively managing border security or aid to Ukraine and Israel.

On the national security front, Hunter Biden agreed to be deposed in the impeachment inquiry.

“Speaking with reporters later Thursday, Comer said, "He's going to be able to come in now and sit down and answer questions in a substantive, orderly manner."

In summary, the political “clown show” is in full swing as the new year begins. We feel so secure knowing that our national interests are so well protected. Will Rogers once said, “Democrats take the whole thing as a joke. Republicans take it serious but run it like a joke.” Now there was a wise man!

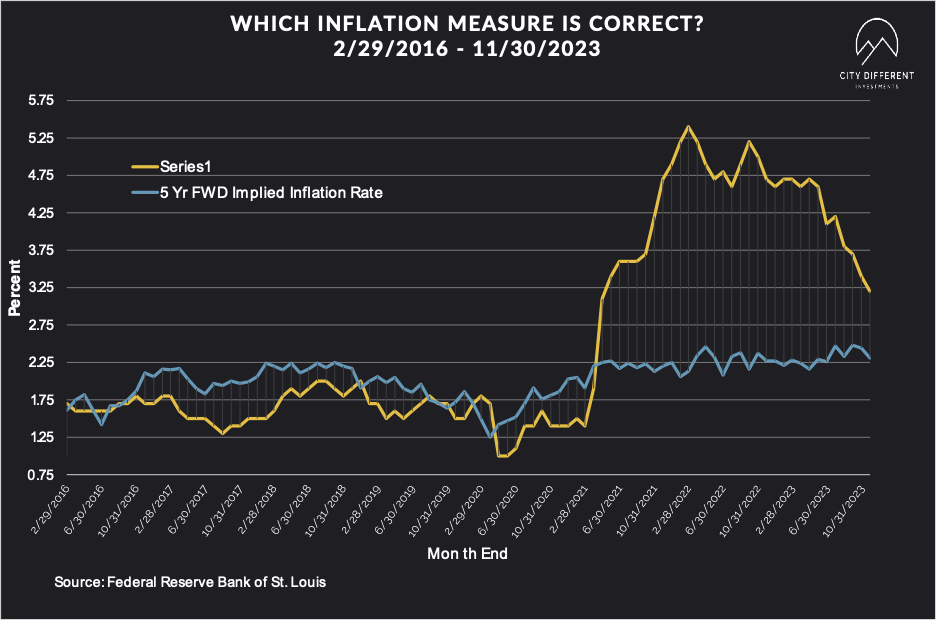

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week of January 19 at 2.38%, six basis points higher than the January 12 close of 2.32%. The 10-year Breakeven Inflation Rate finished the week at 2.34%, seven basis points higher than the close of January 12.

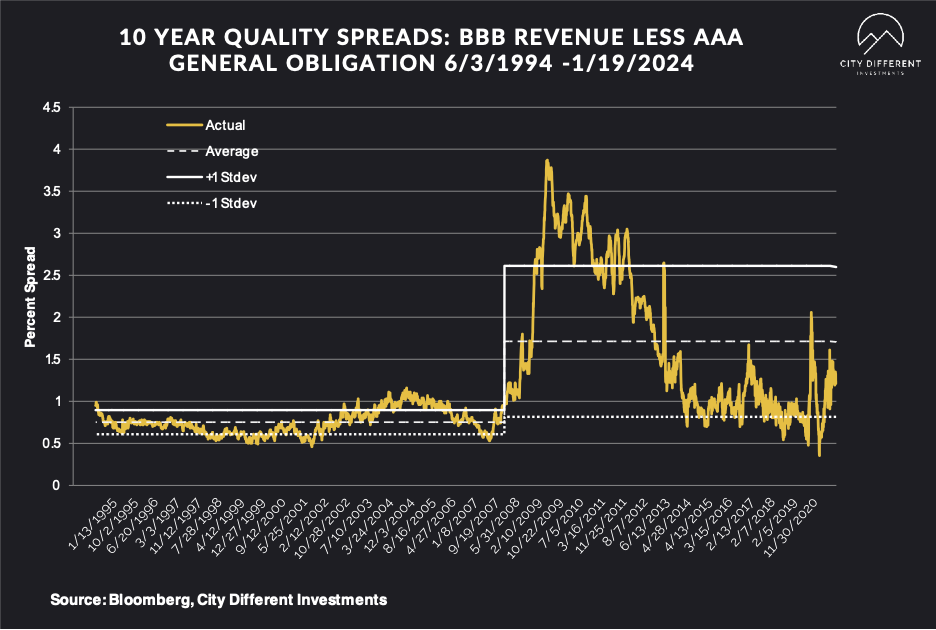

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of January 19 were 1.24%, three basis points higher than the January 12 reading of 1.21% (based on our calculations). The long-term average is 1.71%.

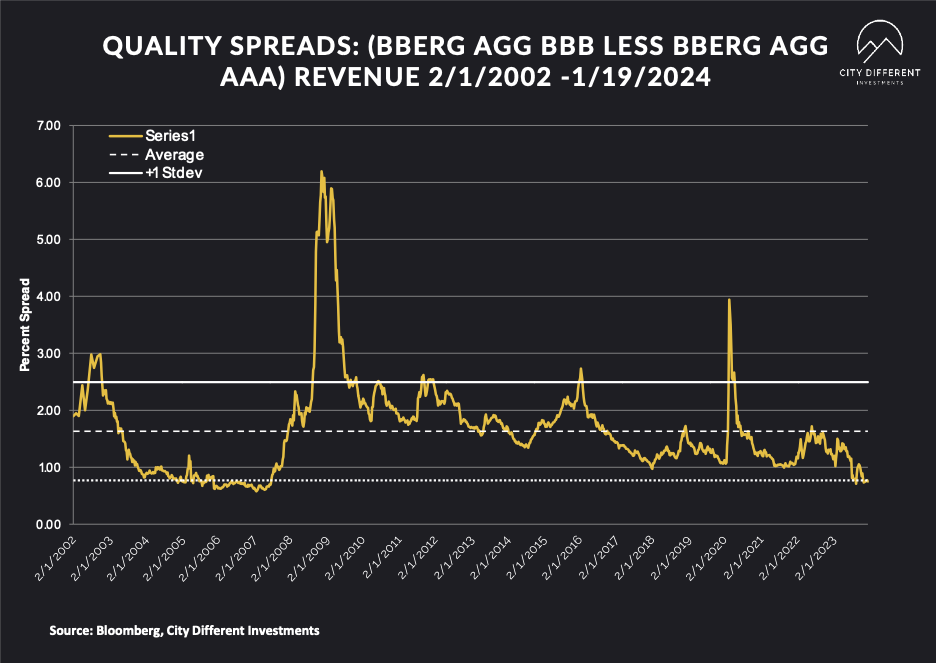

Quality spreads in the taxable market are not attractive but were unchanged (kind of), ending the week at 0.75%, two basis points lower than last week. High-yield quality spreads were 3.16% on January 19.

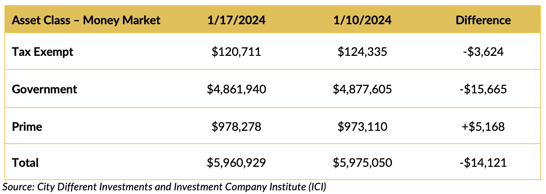

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds flows reversed last week for all categories other than Prime.

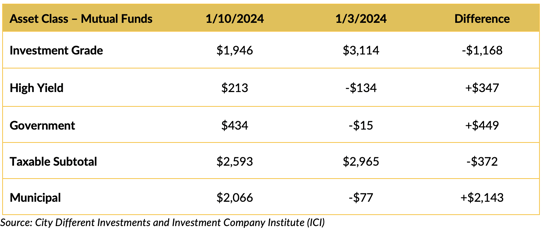

Mutual Fund Flows (millions of dollars)

Winner, winner chicken dinner — municipal cash flows led the way. More evidence of the “January Effect.”

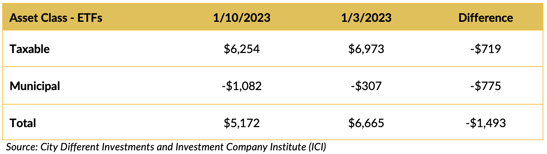

ETF Fund Flows (millions of dollars)

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Supply for municipal tax-exempt calendar will likely remain uneven for the next few weeks at the start of the new year. This week’s municipal tax-exempt calendar estimates are $7.8 billion in new issuance.

CONCLUSION

Economic indicators suggest a reasonable pace of growth and job availability, with data releases surpassing estimates. Federal Reserve governors' statements have tempered rate-cut expectations, leading to a 46.5% probability of a 50 bps move in the Fed Funds rate. Meanwhile, the "January Effect" continues.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.