WEEK ENDING 4/12/2024

- Hope springs eternal and dies hard.

- Equity market declines and rising Middle East tensions aid Treasury’s end-of-week recovery.

- Back to the future, at least in Arizona.

A CITY DIFFERENT TAKE

Wednesday’s CPI release gave both the equity markets and the fixed income markets a swift kick in the…shin. (An anatomical reference higher on the body won’t pass compliance.)

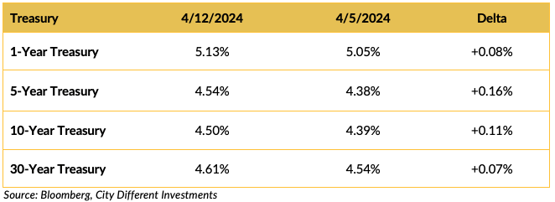

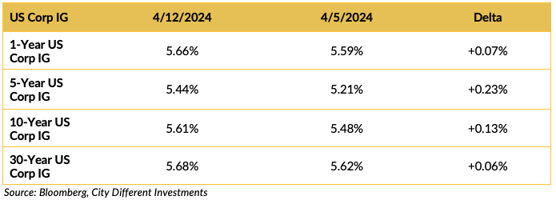

10-year Treasury bonds increased in yield by 0.19% (lower in price). The S&P 500 was down 49.27 points. Both numbers are significant. In addition, both headline CPI YOY (3.5% versus 3.4% expected) and core CPI YOY (3.8% versus 3.7% expected) came in above expectations.

It seems the “exuberance” of last December has turned out to be a little “irrational” (please excuse us, Dr. Greenspan). Thursday’s PPI and jobless claims numbers gave the market a brief respite. But by day’s end, the 10-Year Treasury bond was an additional four basis points higher in yield, continuing the shin-kicking. The only difference is that on Wednesday, the Treasury curve became more inverted, and on Thursday, the Treasury curve was steepening. The yield spread between 2-year and 10-year Treasury securities closed Wednesday at -0.42%, closed Thursday at -0.37%, and closed Friday at -0.35%.

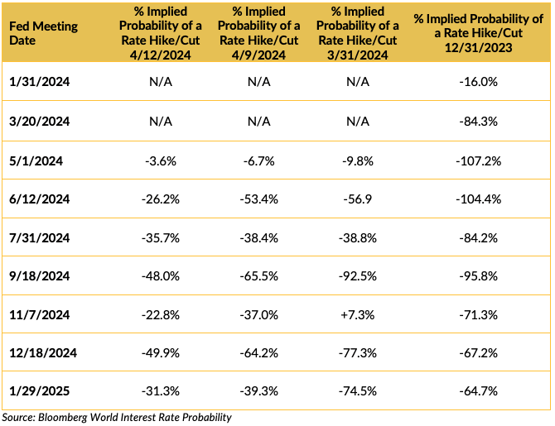

The following table illustrates how market expectations for future rate cuts by the Fed have changed since December 2023. Friday brought a bit of relief; 10-Year Treasury bonds moved lower in yield by 0.07%. The decline in the equity market could have brought about this flight to safety. The S&P index was down 75.65 points (or -1.46%).

Rising tension in the Middle East between Israel and Iran probably did not help matters. We will have to wait to see if Friday’s move was significant or just a “dead cat bounce.”(As of Monday morning, the dead cat did not bounce very high; the 10-Year Treasury was yielding 4.63%, which is 0.11% higher than Friday's close).

As the above table illustrates the probabilities of a 2024 Fed rate cut went from a sure thing in December 2023 to just less than even money on April 12, 2024. In a recent article, The Wall Street Journal reported “Fed Whisper” Nick Timiraos questioned if 2024 Fed rate cuts were still on the table.

As the above table illustrates the probabilities of a 2024 Fed rate cut went from a sure thing in December 2023 to just less than even money on April 12, 2024. In a recent article, The Wall Street Journal reported “Fed Whisper” Nick Timiraos questioned if 2024 Fed rate cuts were still on the table.

On a brighter note, Tax Day is today and we expect to see investors sell fixed income securities with unrealized losses attached to fund tax payments. This, coupled with recent rate moves, can provide investors with cash and, being short of their duration targets, an opportunity for investment. For all the others, hang on. It can be a bumpy ride, and fear is never a good investment strategy.

CHANGES IN RATES

Treasury rates moved higher on the week. The increase in the CPI report brought into question whether the Fed cut short term rates in 2024. The market’s drubbing took a respite on Friday as the equity markets continued their decline. The S&P 500 was down 80.93 points (or -1.6%) on the week.

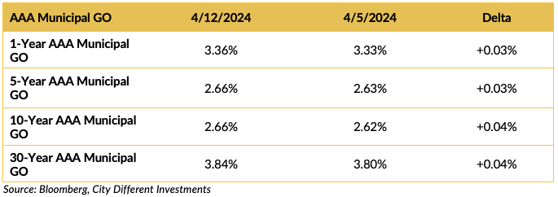

The municipal market’s yields moved higher on the week (but only slightly compared to the Treasury market’s moves). The market is seeing lower supply than anticipated and positive cash flows into mutual funds.

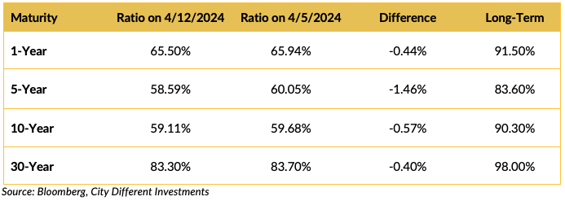

The municipal/Treasury ratios decreased last week, the result of the municipal market’s relative outperformance versus their Treasury equivalents.

This market segment saw higher rates last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

The House of Representatives is back in session. Wasn’t it peaceful while they were on vacation? You might be wondering how the government would run if they remained on vacation, but the real question is how will the government run with them back? Remember, on Tax Day, we get to pay for all this!

Tensions are on the rise in the Middle East. Iran executed a retaliatory attack on Israel. President Biden told Iran “don’t” attack Israel — which they did. We don’t know, feels like telling teenagers not to drive fast. This is one factor in Friday’s relief rally.

And now we turn to Arizona, or as Google puts it, “a state known for its mile-wide deep chasm carved by the Colorado River.”

“PHOENIX — The Arizona Supreme Court ruled Tuesday that a 160-year-old near-total abortion ban still on the books in the state is enforceable, a bombshell decision that adds the state to the growing lists of places where abortion care is effectively banned.”

Seems like the Arizona State Supreme Court cut another “deep chasm” in the GOP’s approach to abortion, possibly putting Arizona in play for Democrats in the presidential election. It seems like one of the parties is the dog that caught the car and didn’t know what to do with it.

WHAT, ME WORRY ABOUT INFLATION?

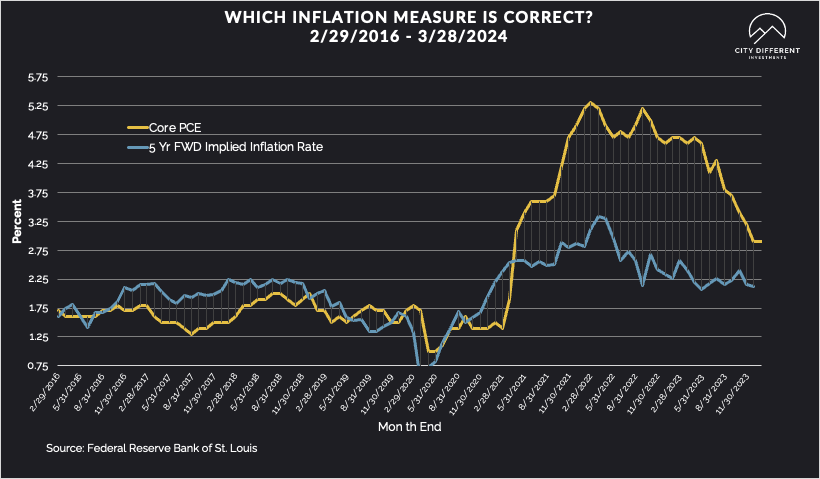

The 5-year Breakeven Inflation Rate finished the week of April 12 at 2.47%, two basis points higher than the April 5 close of 2.45%. The 10-year Breakeven Inflation Rate finished the week at 2.39%, two basis points higher than the close of April 5.

MUNICIPAL CREDIT

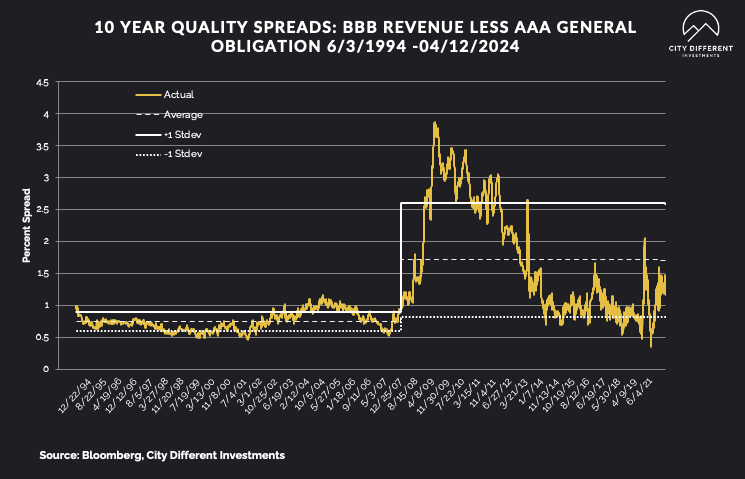

10-year quality spreads (AAA vs. BBB) as of April 12 were 1.17%, three basis points lower than the April 5 reading of 1.20% (based on our calculations). The long-term average is 1.70%.

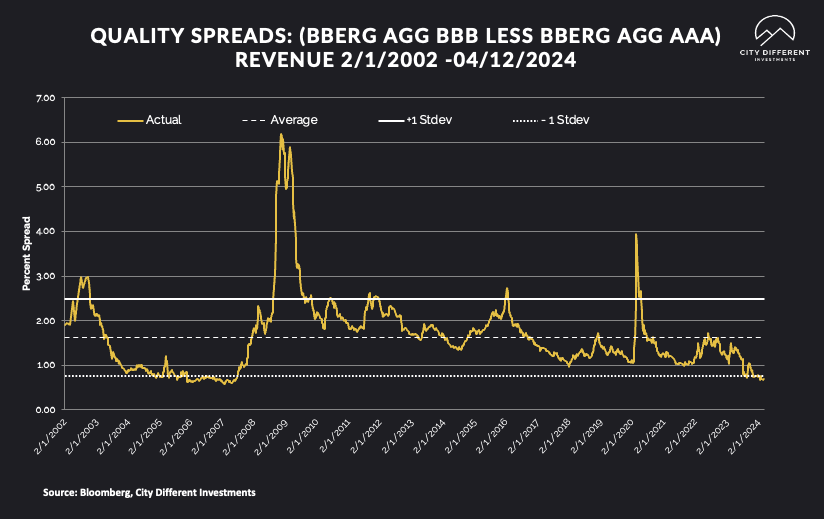

Quality spreads in the taxable market are not attractive but were slightly lower, ending the week at 0.69, one basis point lower than last week. High-yield quality spreads were 2.64%, unchanged from week of April 5.

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

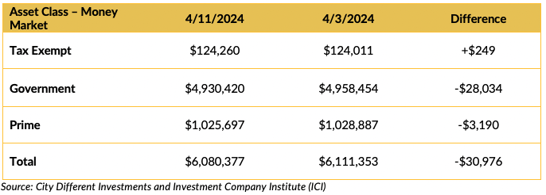

Money Market Flows (millions of dollars)

Money market funds saw a drop in cash flows.

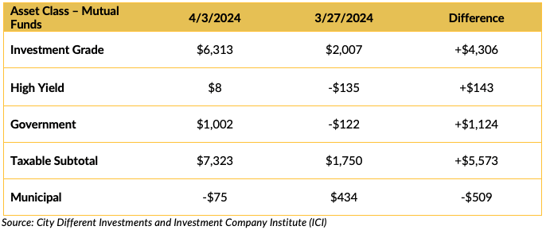

Mutual Fund Flows (millions of dollars)

Bond funds saw positive cash flows with the exception of Munis.

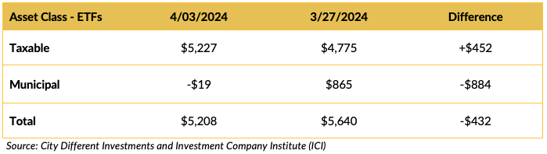

ETF Fund Flows (millions of dollars)

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Supply for municipal tax-exempt calendar will likely hit $5 billion this week.

CONCLUSION

It seems like the hopes for a 2024 rate cut have been exercised out of the fixed income market’s prevailing sentiment. We pride ourselves on being contrarians. When the markets were pricing six to seven rate cuts in December, we were skeptical. Now that the market seems to be reaching the opposite conclusion, we are getting interested.

We think this is a good time to buy fixed income securities. Yes, municipal bonds are a little pricey compared to their Treasury equivalents, but that could change quickly. We are still focusing on the shorted half of our strategies’ investment universes to overweight. We think we are getting paid to wait in that segment of the market. Our overall duration exposures are neutral (we would expect to be in that range 70% of the time). Based on 2.8% core PCE, the recent backup in rates makes the real yield on a 10-Year Treasury 1.72% at the close of April 12 with a long-term average of 1.9%. Using the same assumptions, the 5-year Treasury at the close of April 12 has a real yield of 1.76% versus a long-term average of 1.39%. You can see why we favor shorter-maturity securities.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.