.png)

WEEK ENDING 8/18/2023

Highlights of the week:

- Treasury continues to bring big supply to the market.

- China has another real estate problem: a snake in Country Garden.

- This time, maybe it will be different!

A CITY DIFFERENT TAKE

Rates continued to move higher last week.

Municipals lagged behind the Treasury market in the move to higher rates. Treasury investors were supposedly worried about the Fitch downgrade (we were not); a $102-billion increased supply of Treasury bonds (we share that worry); and more robust economic data (again, we concur).

Not to mention the snake in China’s Country Garden. China’s largest property developer faces default. Direct exposure to foreign investors is small, but the initial knock-on effect could initiate a flight to quality. 10-Year Treasuries hit high yields for the year, and municipal bonds followed but at a slightly slower pace. The Federal Reserve’s meeting in Jackson Hole is all set for August 24th, and given some more hawkish comments from Fed officials, it sets up to be interesting.

Stocks are down, and bonds are up in yield. Many street analysts are changing their outlooks from “a recession is around the corner” to “a soft landing is being engineered.” Some are even saying that no landing is likely. The Fed minutes and commentary before the Jackson Hole conference have led some to believe the Fed is not done raising short-term interest rates because of the economy's resilience.

The Treasury yield curve is experiencing a “Bear Steepener.” Long yields are increasing at a higher rate than short yields. The spread between two-year and 10-year Treasury securities has become significantly less inverted (1.06% on June 30 versus 0.69% on August 18). Real gross domestic product (GDP) increased by an annual rate of 2.4% in the second quarter of 2023. Unemployment is low; July’s unemployment rate was 3.5%. This is all happening before the full impact of Bidenomics kicks in (money from the Inflation Reduction Act and the Chips Act).

Why is this happening? Many economists thought that with such a significant increase in short-term interest rates, the economy would slow, with a lag. We believe they have miscalculated the impact of COVID-era government measures. Those include QE and the government’s pandemic relief programs. These programs led to ultra-low interest rates that corporations and homeowners took advantage of to refinance and, in many cases, extend their debt. These steps increased the amount of money supply and decreased the economy's sensitivity to changes in short-term interest rates.

See our blog "Why is the Economy so Resilient" for all the details or reach out to Sweta or Chris.

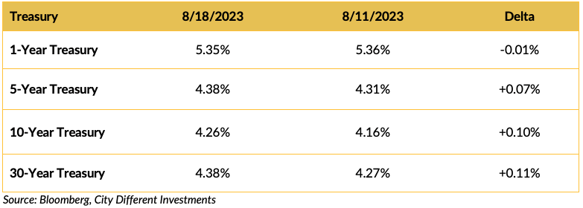

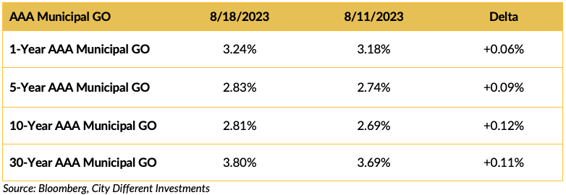

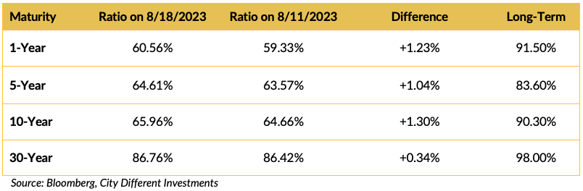

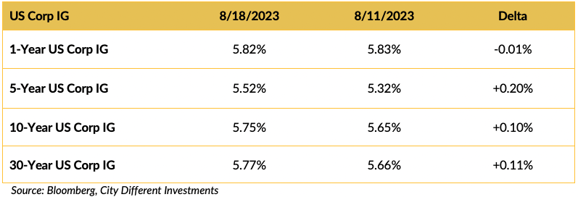

CHANGES IN RATES

Treasury yields continued to move higher despite some fixed-income-friendly inflation data. The “Bear Steepener” was sustained. The spread between two-year and ten-year Treasury security yields finished the week at 0.69%.

Municipal yields moved higher last week across the curve, catching up with prior Treasury moves. The municipal market is also experiencing a “Bear Steepener,” just at a different rate than the Treasury market. The supply of new issue municipal bonds was at a seasonally low point of about $7 billion last week (about the same for next week). Municipal bond mutual funds saw redemptions last week, which brings the year-to-date total to $7.4 billion.

Relative values can change rapidly and with little warning, as they did last week. Muni/Treasury ratios are higher but still well below the long-term averages.

Yields in the investment grade (IG) corporate market followed the Treasury market pattern. Yield curve steepeners all around!

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

The big news last week was not out of D.C., but rather Atlanta and Camp David.

Last Monday, former President Trump was indicted for a fourth time. The latest indictment comes out of Georgia over his efforts to overturn 2020 election results. This is getting to be old hat and sadder by the indictment.

And in Maryland, President Biden hosted two old enemies at Camp David: South Korea and Japan. The result is a “new era of partnership.” This administration sure has a knack for maintaining and building alliances. Not to mention not backing down from bullies on the world stage. No Neville Chamberlain is he!

As mentioned last week, Congress is still in recess. This upcoming week, the fixed-income market's attention will be focused on Wyoming and the Chair’s Jackson Hole speech on Friday. Last year’s 8-minute speech was a market mover!

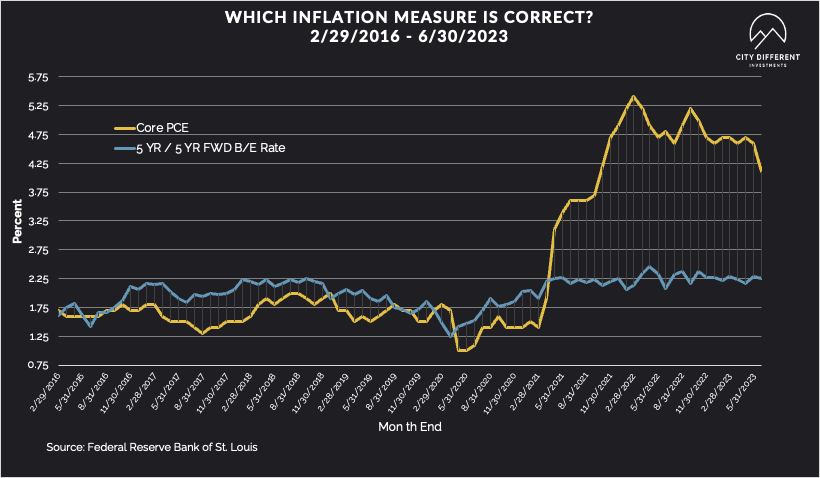

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.42%, no change over the August 11 close of 2.42%. The 10-year Breakeven Inflation Rate finished the week at 2.32%, a four-basis point decrease from the August 11 close.

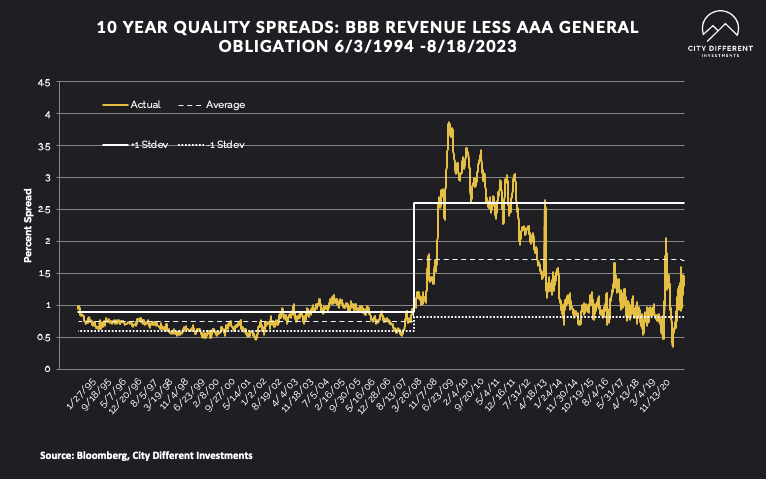

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of August 18 was 1.30% (based on our calculations), 8 basis points lower than the August 11 close of 1.38%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

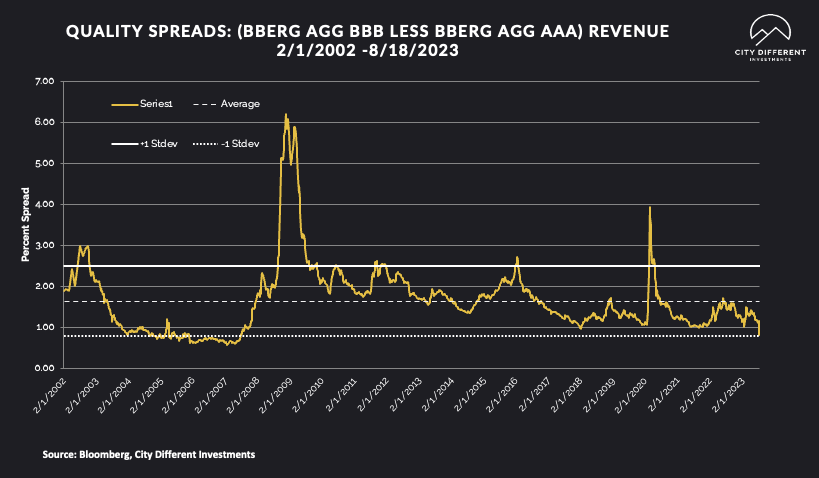

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 0.86%.

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money funds, in total, saw positive cash flows again last week. Money market yields are attractive, but how long will that last? Just like Joe Hallenbeck warned Jimmy Dix in “The Last Boy Scout”:

“Water's wet. The sky's blue. And old Satan Claus, Jimmy, he's out there. And he's just getting stronger.”

The cash trap is looming and growing. If you would like to discuss the implications of this risk, please reach out to City Different Investments, or read our last blog on the issue.

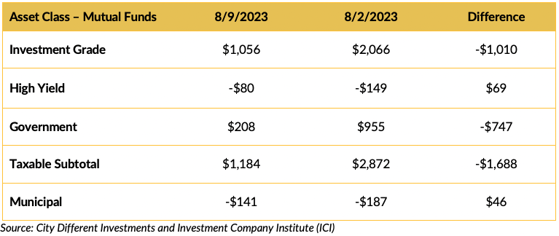

Mutual Fund Flows (millions of dollars)

Flows into bond funds are mixed for the week. It looks like municipal bond investors do not like higher yields.

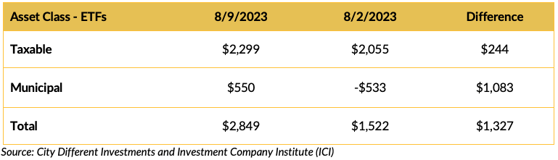

ETF Fund Flows (millions of dollars)

Bond ETFs were also mixed, with municipals recording a net inflow for the week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around a moderate $7 billion again. This should be manageable.

CONCLUSION

The curve is steepening, with rates moving higher. Chair Powell’s Friday speech should shed some light on the Fed’s thinking. The economy has proven to be much more resilient that many economists expected. The much-forecasted recession has found Godot and the market is waiting for both.

We shudder to say this out loud but maybe… just maybe… maybe it is different this time?

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.