WEEK ENDING 12/12/2025

- Federal Reserve nears policy pause after "insurance cuts"

- Mixed economic signals and upcoming key data

- Uneven global policy and US fiscal concerns

A CITY DIFFERENT TAKE

The Federal Open Market Committee (FOMC) delivered an expected interest rate cut of 25 basis points, bringing the federal funds rate to 3.5%–3.75%. However, Chair Powell strongly signaled that the period of "insurance rate cuts" is over, suggesting a reluctance to ease further unless the labor market shows more "worrying signs." This hawkish tone was reinforced by two dissents in favor of holding rates steady and Powell's repeated mention of the "neutral rate," implying policy is now close to a level that neither stimulates nor restricts growth. While the market still anticipates one more cut in January, the Fed's new forward guidance (referencing the "extent and timing" of further cuts) is similar to language used before its previous extended pause. Separately, the Fed initiated Reserve Management Purchases (RMPs) of T-bills at a pace of $40 billion per month, stressing that this is a technical move to maintain bank liquidity and not a return to quantitative easing (QE).

The incoming economic data presents a mixed picture, complicating the Fed's next move. On the one hand, strong September trade and inventory data led to an upward revision of Q3 GDP growth, tracking to 3.5%, which is above most estimates of potential growth and suggests that policy may not yet be restrictive. On the other hand, the labor market is showing signs of softness, with the unemployment rate rising by a full percentage point over the 30 months leading up to September. Next week's release of the November employment report is expected to show steady payrolls but a rise in the unemployment rate to 4.5%. Additionally, the November CPI report is forecast to show a 0.3% rise in both headline and core inflation. The market is also focused on the competition for the next Fed Chair, with former Fed Governor Kevin Warsh now reportedly the frontrunner over NEC Chair Kevin Hassett.

The Fed's pause comes amidst a period of uneven global monetary policy. Next week is expected to feature a diverse set of actions, including a forecast rate hike by the Bank of Japan (BoJ) to 0.75%, a resumption of rate cuts by the Bank of England (BoE), and the European Central Bank (ECB) remaining on hold. Furthermore, the growing U.S. budget deficit is emerging as a significant factor in determining longer-term interest rates. The trailing 12-month deficit was 5.27% of GDP as of November. Although fiscal 2026 is projected to be the first year since 2019 with a deficit-to-GDP ratio under 5% (a critical threshold for debt manageability), the need for increased government borrowing globally is expected to affect interest rates in the coming year.

CHANGES IN RATES

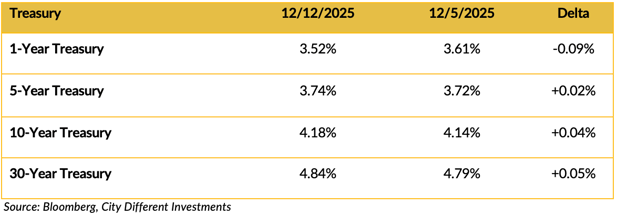

Treasury Market

The Treasury yields increased marginally in all tenors. The 2/10 spread is at 66 basis points for the week.

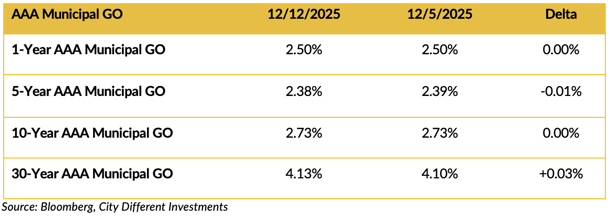

Municipal Market

Yield remained range-bound in the muni market, with the 30-year yield rising the most. The 2/10 slope is at 23 basis points, which is still very flat.

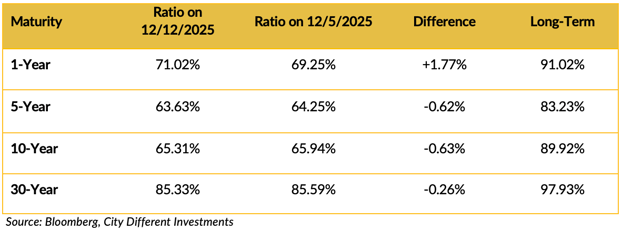

Selected Municipal AAA General Obligation Bond / Selected Treasury Bonds Yield Ratio

Treasury-muni ratios were slightly lower across the yield curve because of a higher Treasury yield curve and relatively unchanged yields for the muni curve.

Investment Grade Corporates

Investment-grade corporate bond yields moved higher week over week.

THIS WEEK IN WASHINGTON

The past week in D.C. was dominated by major action on the annual defense bill, key developments in healthcare policy, and new executive moves on technology and immigration.

The looming expiration of the enhanced premium tax credits under the Affordable Care Act (ACA) at year-end was a major point of policy gridlock. House Republicans unveiled a healthcare plan that did not include an extension of these enhanced tax credits, proposing an alternative strategy for health insurance coverage. This sets up a clash over how to address sharply rising health insurance premiums for millions of Americans.

The House of Representatives passed the annual National Defense Authorization Act (NDAA) on December 10, the key defense policy legislation that directs spending for the military. The Senate is expected to pass the measure as well, following a period of bicameral disagreement.

President Trump signed an executive order to limit state-level regulations of Artificial Intelligence, seeking to establish a national policy framework for the technology.

The administration announced $12 billion in "Farmer Bridge Payments" to support American farmers impacted by unfair market disruptions, utilizing existing legislation to facilitate this aid.

WHAT, ME WORRY ABOUT INFLATION?

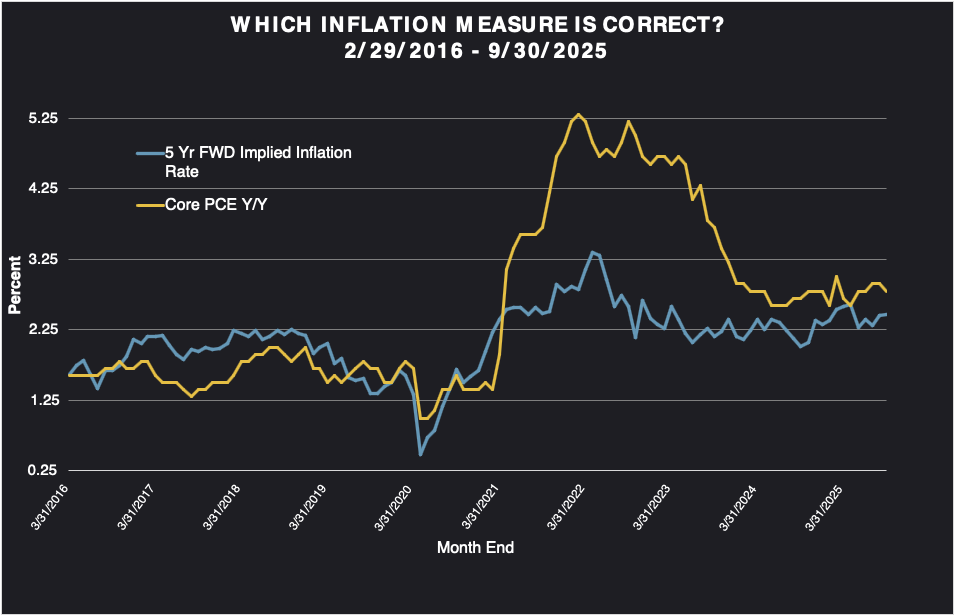

The 5-year Breakeven Inflation Rate finished the week of Dec. 12 at 2.32%, 2 basis points lower than the previous week. The 10-year Breakeven Inflation Rate finished the period at 2.26%, same as last week's observation.

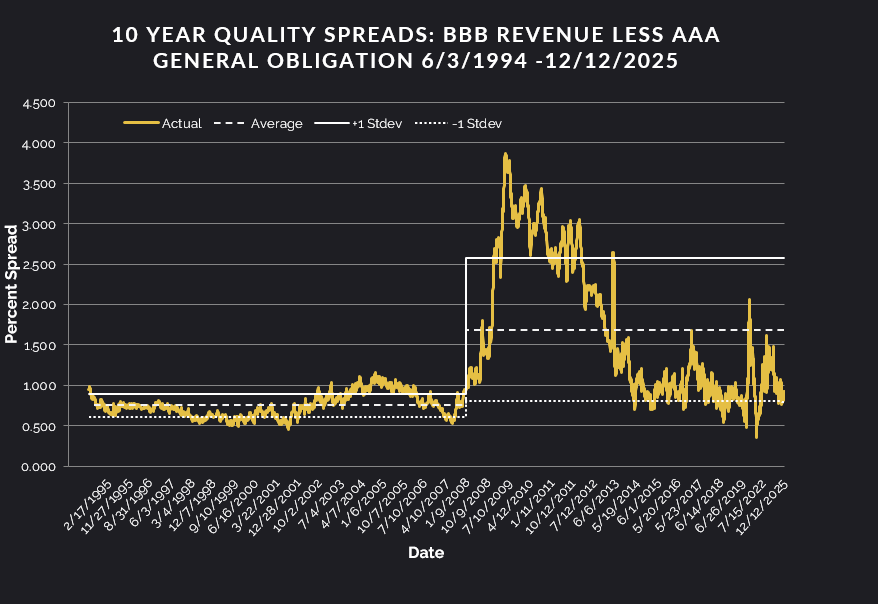

MUNICIPAL CREDIT

Last week's 10-year quality credit spread between BBB revenue bonds and AAA general obligation bonds was 0.92%, same as last week compared to a historical average of 1.68%, demonstrating very healthy and tight spread metrics.

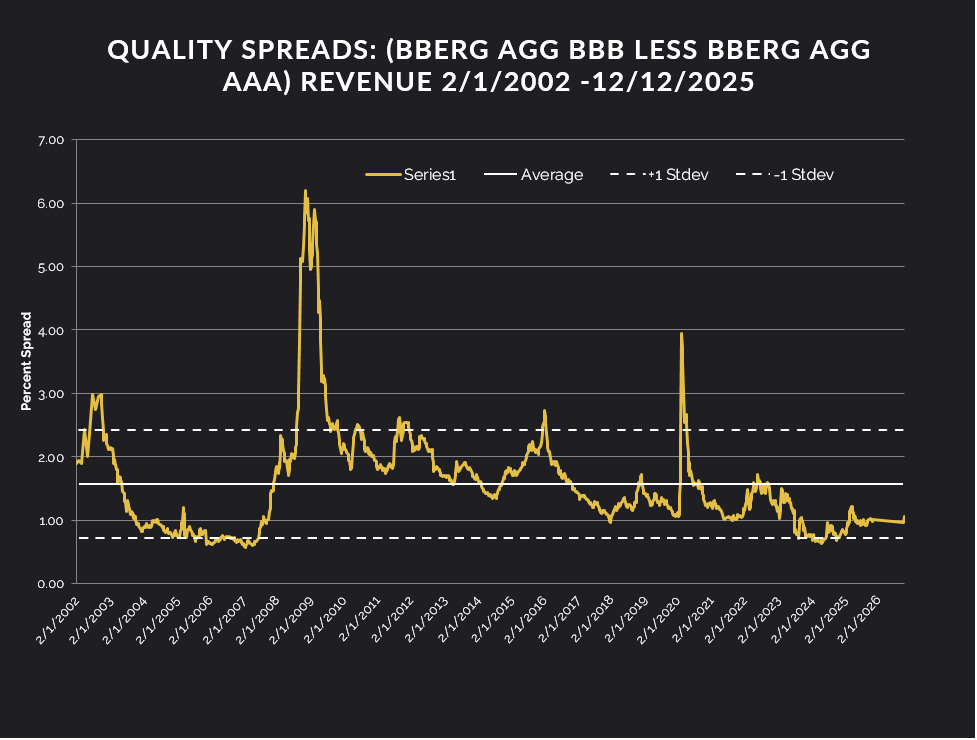

TAXABLE CREDIT

Investment-grade spreads widened a bit at 1.01%, 3 basis points higher than last week. The long-term average is 1.57%. The high-yield spread is higher at 2.63%, compared to a historical average of 4.56%.

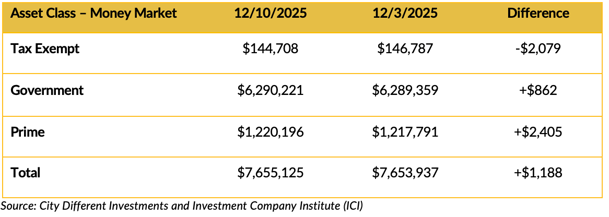

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market fund flows were lower in the tax-exempt category, however, higher in the government and prime categories.

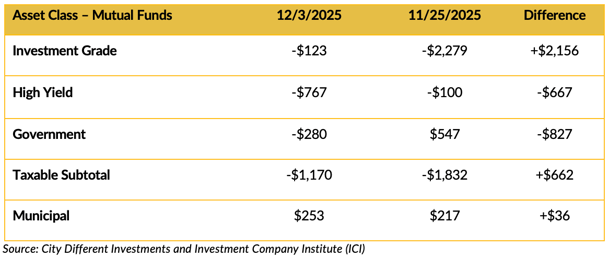

Mutual Fund Flows (millions of dollars)

Mutual fund flows in total were up week-over-week.

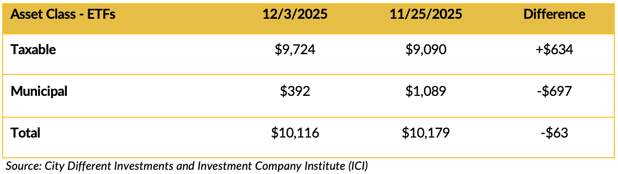

ETF Fund Flows (millions of dollars)

Net ETF flows were lower than the week before with taxable bonds being the only positive category.

SUPPLY OF NEW ISSUE BONDS

This week’s supply is projected to be $6 billion. This comes up against $9 billion of coupon reinvestment.

CONCLUSION

The past week marks a significant pivot in U.S. monetary policy, with the Federal Reserve ending its "insurance cut" cycle and signaling a new period of caution as the federal funds rate approaches the estimated neutral range. This shift is complicated by conflicting economic signals: robust Q3 GDP growth suggests strength, while indicators like the rising unemployment rate and downward trend in quits from the JOLTS report suggest an underlying softness in the labor market.

Looking ahead, the direction of U.S. policy and the Fed's next move hinge entirely on next week's crucial data releases, including the employment reports and the CPI inflation reading. Globally, this U.S. policy pause contrasts with divergent actions from other central banks (like expected hikes in Japan and cuts in the UK). Finally, domestic fiscal policy — specifically the large and persistent U.S. budget deficit — remains a growing concern that is projected to exert pressure on longer-term interest rates in the coming year, regardless of the Fed's near-term decisions.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein is available upon request.