.png)

The week of August 14, 2023, has been a tough one for most markets. Stocks are down, and bonds are up in yield. Many street analysts are changing their outlooks from “a recession is around the corner” to “a soft landing is being engineered.” Some are even saying that no landing is likely. The Federal Reserve’s minutes and commentary before the Jackson Hole conference have led some to believe the Fed is not done raising short-term interest rates because of the economy's resilience.

The Treasury yield curve is experiencing a “Bear Steepener.” Long yields are increasing at a higher rate than short yields. The spread between two-year and 10-year Treasury securities has become significantly less inverted (1.06% on June 30 versus 0.69% on August 18). Real gross domestic product (GDP) increased by an annual rate of 2.4% in the second quarter of 2023. Unemployment is low; July’s unemployment rate was 3.5%. This is all happening before the full impact of Bidenomics kicks in (money from the Inflation Reduction Act and the Chips Act).

Why is this happening? Many economists thought that with such a significant increase in short-term interest rates, the economy would slow, with a lag. We believe they have miscalculated the impact of COVID-era government measures. Those include QE and the government’s pandemic relief programs. These programs led to ultra-low interest rates that corporations and homeowners took advantage of to refinance and, in many cases, extend their debt. These steps increased the amount of money supply and decreased the economy's sensitivity to changes in short-term interest rates.

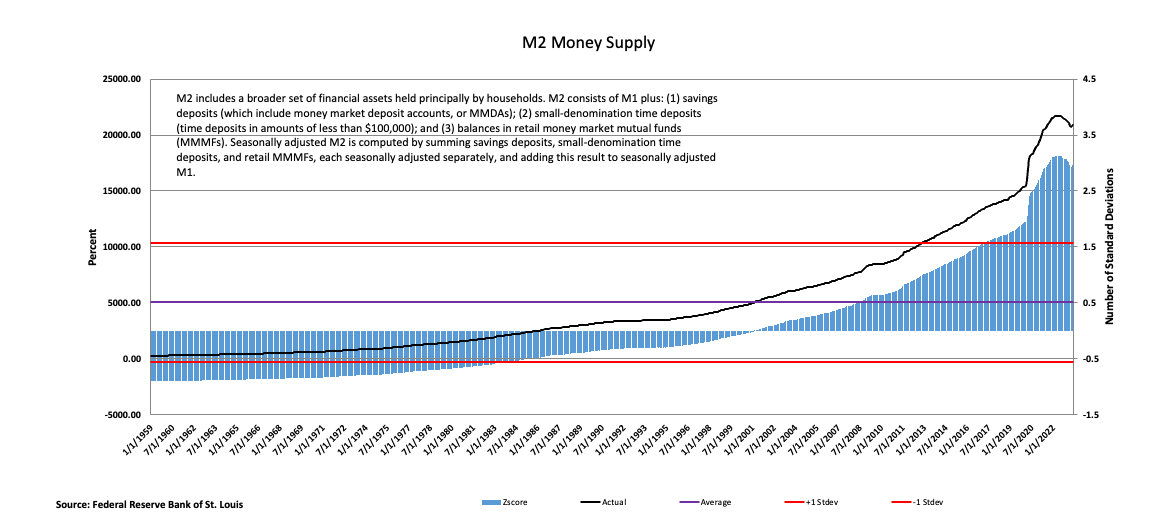

Money Supply

The latest figures from the St. Louis Fed show that M2 (a measure of the money supply) has rolled over but still has a lot of money in the system. The amount of money in the system is close to a three-standard deviation event, based on data from 1959.

Couple that with an increase in the velocity of M2 and you have a formula for future inflation (or at least stubbornly persistent inflation).

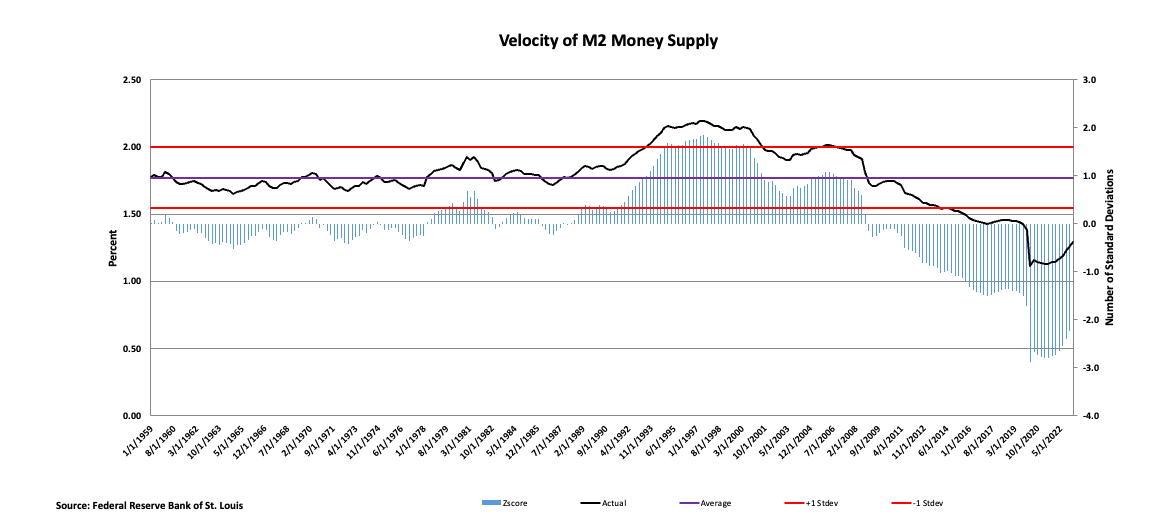

The velocity of M2 (degree of turnover) has been running low by historical standards, a negative 2.1 standard deviation event. The amount of money in circulation offset this low measure. Still, the latest number shows an increase in this measure. To paraphrase Milton Friedman, much money in the system turning over supports inflation.

The velocity of M2 (degree of turnover) has been running low by historical standards, a negative 2.1 standard deviation event. The amount of money in circulation offset this low measure. Still, the latest number shows an increase in this measure. To paraphrase Milton Friedman, much money in the system turning over supports inflation.

The Economy’s Sensitivity to Short-Term Interest Rates

The amount of refinancing and debt extension by both homeowners and corporations during the pandemic era has lessened the economy's sensitivity to short-term interest rates. Since the expense side of both groups is locked in, an increase in short-term interest rates may make their cash more productive.

Corporations

Corporations took advantage of the ultra-low pandemic-era interest rate environment to issue debt to lock in low rates and raise liquidity after their 2008 and 2009 financial crisis experiences. Below is an excerpt from a WSJ article titled U.S. Companies Are Thriving Despite the Pandemic - or Because of it

“Stung by the cash crunch that accompanied the financial crisis in 2008 and 2009, many companies rushed to borrow when the pandemic hit in 2020. Large companies were able to borrow large amounts, issuing a median $123.6 million in debt in the 12 months ending in late 2020. The year before, they only issued $6.4 million. In 2021, they started paying it down, cutting debt by $24 million on average, according to data from FactSet.”

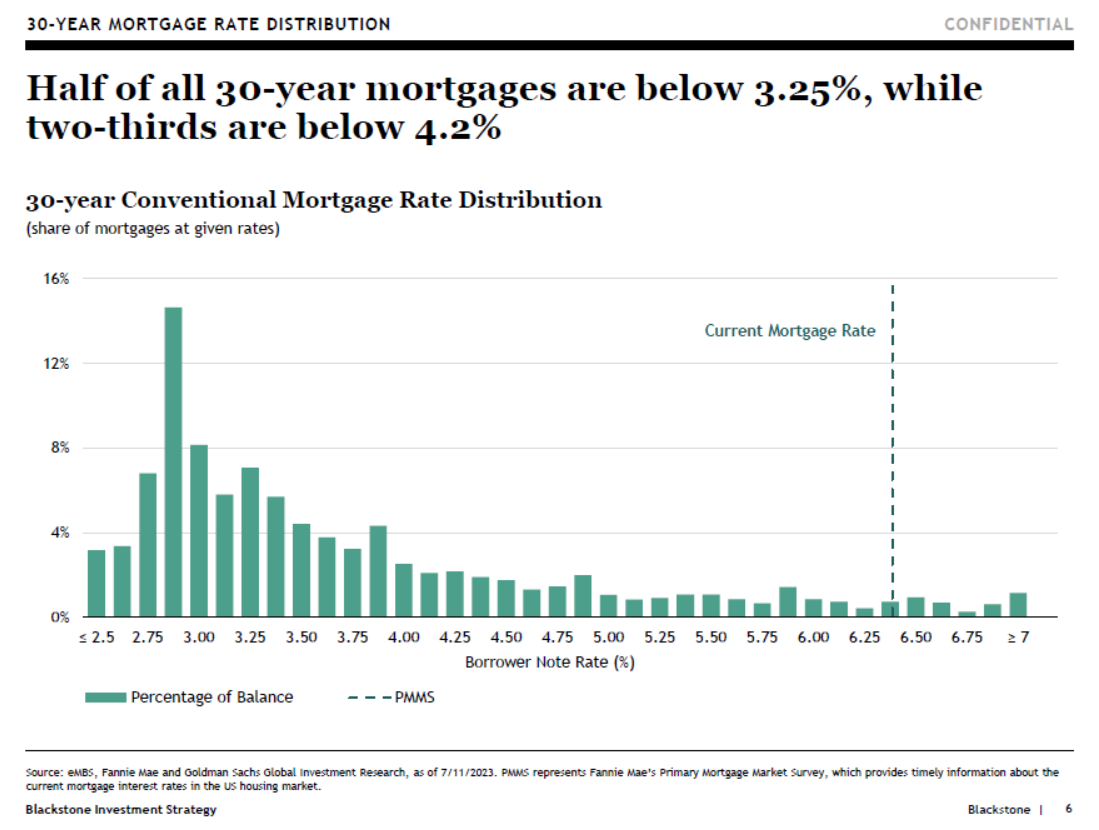

Homeowners

The following graph illustrates the coupon distribution of 30-year mortgages. Homeowners used the pandemic-era ultra-low interest rates to refinance their mortgages, if they could. These low-interest-bearing mortgages currently look like assets compared to current mortgage rates at around 7.00+%.

Conclusion

The post-pandemic error does not have any historically equivalent periods. This time, it truly was different.

IMPORTANT DISCLOSURES

The information and statistics contained in this communication have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or forecasts discussed herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, or any non-investment related content, made reference to directly or indirectly in this communication will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. No discussion or information contained herein serves as the provision of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability above to his/her individual situation of any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal, tax, or accounting advice.

Visitors to the City Different Investments web and social media sites are asked to read these terms.