WEEK ENDING 2/17/2023

Highlights of the week:

- Where is the recession?

- Federal Reserve is chasing neutral rate, and the market is catching up.

- Friday marks one year of the Russia-Ukraine war.

A CITY DIFFERENT TAKE

The recession of 2023 was (or is going to be) the most predicted recession in our history. We spent most of 2022 with talking heads, analysts, and CEOs all predicting a recession — first in the spring of 2023 and now in the fall of 2023. But the data pumped out in January still stands strong. Retail sales saw their highest jump in the last two months. Both the Consumer Price Index and the Producer Price Index came in stronger than expected. And the labor market remains robust with unemployment at a 53-year low.

None of this sounds like a hard landing, or a soft one for that matter. We have been navigating language surrounding both a hard landing and a soft landing for the economy. But we seem to be stuck in a loop between strong economic data and the Fed’s rate hikes.

So, where is the Fed’s neutral rate in the middle of the landing discussion. At the beginning of February, the futures market was predicting a Fed Fund rate of 4.88% in June. But with the hawkish data releases, the neutral rate has jumped up to 5.25% around August.

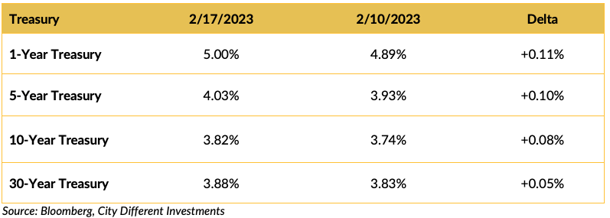

CHANGES IN RATES

A couple of hotter-than-expected inflation reports (CPI and PPI) add to this. Some bearish Fed official comments proved to be a volatile mix for the fixed-income markets. Treasury rates moved higher on the week across the yield curve. The largest increases were in the short portion of the Treasury market. The slope of the 1-to-10-year yield curve went a little more negative, moving to -1.18% vs. last week’s -1.15%.

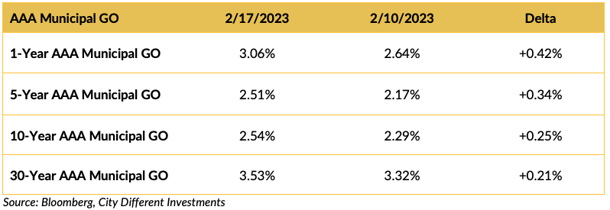

The municipal market reacted much worse to the inflation reports and Fed comments. Our own Sweta Singh was quoted in a Bloomberg article on Friday about municipal yields extending their climb against Treasuries:

“Muni yields rose higher than Treasuries because we just went through January effect where we organically have coupon money being put back in the market,” said Sweta Singh, a portfolio manager at City Different Investments. Plus, “we are now seeing some supply” in munis, and retail investors may be pulling out cash as performance weakens, she said.

The market giveth, and the market taketh away. It will be interesting to see how the municipal market reacts to the shortened holiday week.

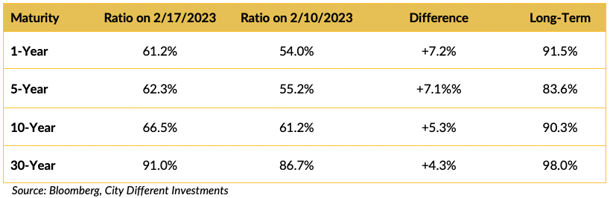

The ratios above and their weekly changes are another representation of how the two fixed-income markets recorded such different reactions.

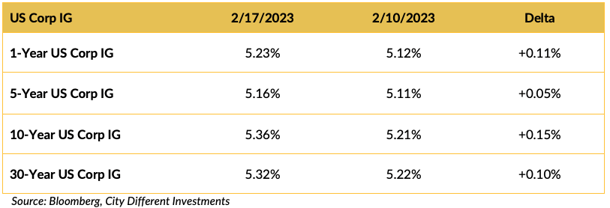

The week’s volatility was shared by the investment grade (IG) corporate market.

We have asked this question in the past, and we are sure we will ask it in the future. Of the three fixed-income markets highlighted above, which one does not belong?

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

The big news coming out of Washington this week was the surprise meeting between President Biden and President Zelensky days before the Russia-Ukraine war’s first anniversary. (It is hard to believe that the war has reached its one-year point.) President Biden pledged another $500 million in aid to Ukraine. This package will include artillery ammunition, anti-armor systems, and air surveillance radars.

In other noteworthy political news, the tone of the U.S. and China relationship continues to be rocky. From North Korea to the spy balloon, Secretary of State Antony Blinken and China’s state councilor Wang Yi did not back down from jabs and harsh rhetoric.

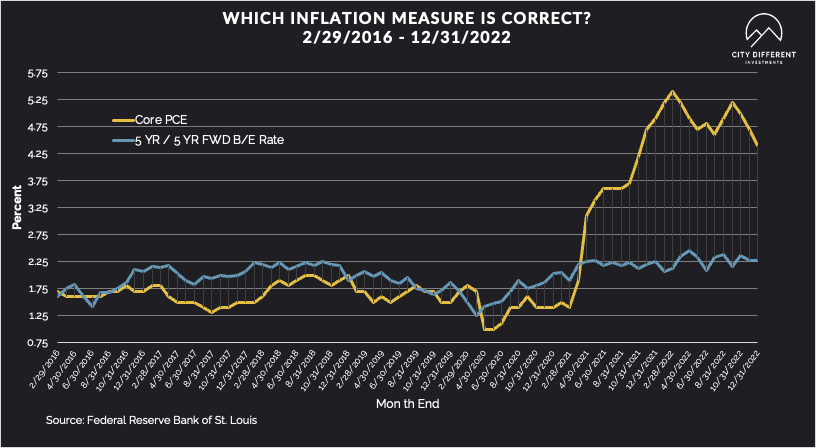

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended Friday at 2.22%, 3 basis points higher than closing at 2.19% on February 10. The 10-year Breakeven Inflation Rate ended the week at 2.36%, 3 basis points higher than last week’s observation of 2.33%. Given the stability of these measures, and in light of new information, we question their value as an inflation forecasting tool.

MUNICIPAL CREDIT

Municipal credit continues to be strong. However, the popular press is picking up stories about hiccups in Municipal high-yield funds. High-yield is normally the first sector to show weakness as the economy cools. According to an article published by Bloomberg last Friday:

“The biggest holding in the world’s biggest high-yield municipal bond fund isn’t a municipal bond. It’s a $1.5 billion stake in shares of Energy Harbor Corp., a thinly traded power company that’s not listed on any US stock exchange.”

This brings pause for investors. Do you really know what is in your mutual fund holdings?

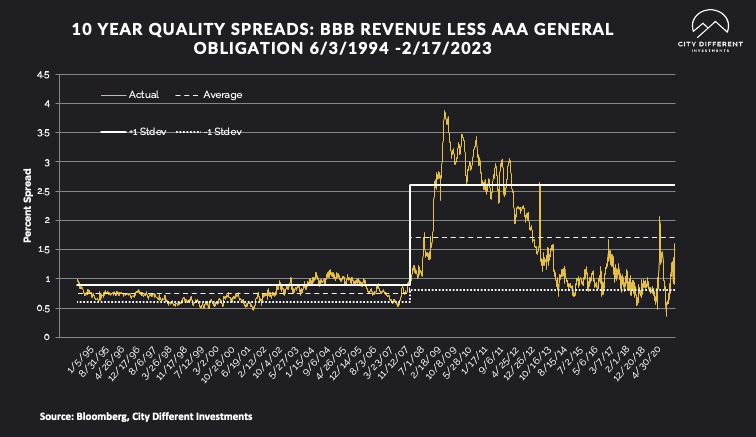

10-year quality spreads (AAA vs. BBB) were narrowed on the week from 1.32% to 1.22% (based on our calculations). The long-term average is 1.71%. Lower-quality securities are still not attractive by our way of thinking. Usually when the municipal market has significant shifts, lower-quality securities are the last to move. That is until someone tries to sell them.

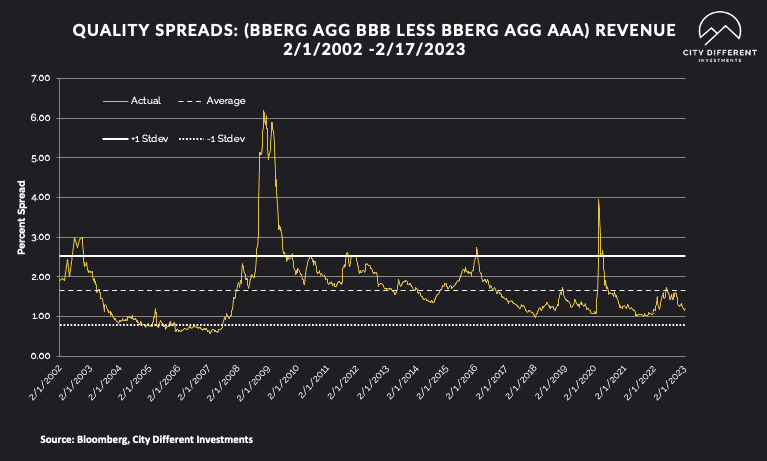

Quality spreads in the taxable market didn’t move much on the week, finishing at 1.20% vs. 1.18% last week.

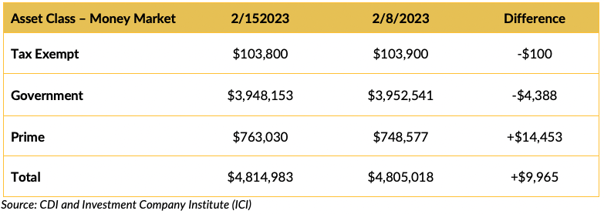

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Prime money market funds won the week, again!

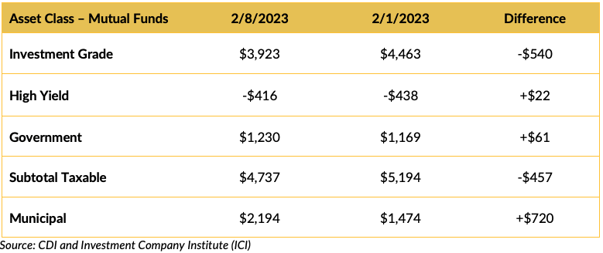

Mutual Fund Flows (millions of dollars)

Municipal bond funds won the week. But that is before last week’s revaluation. We shall see if these numbers hold up next week.

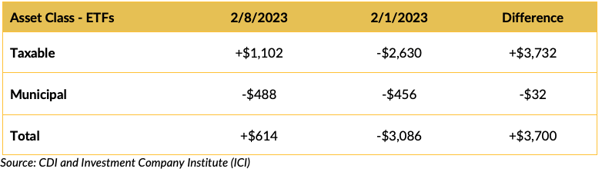

ETF Fund Flows (millions of dollars)

A quiet week for bond ETFs.

Other services that track mutual fund cash flows have reported negative flows for municipal bond mutual funds for the week ending February 15. This should be confirmed in next week’s ICI numbers.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

We estimate that next week’s new-issue supply will be low, around $4.3 billion in the shortened holiday week.

Total new issuance supply figures of $10 billion or more usually indicate weakness in new-issue supply pricing (higher yields).

CONCLUSION

The end of this week marks the one-year anniversary of Russia’s invasion of Ukraine. The U.S. seems committed in its support for Ukraine with President Biden visiting President Zelensky this week.

The data coming out of the economy continues to be strong. There are no signs of recession in sight yet. However, this strong data flows over into the Fed dilemma for the new neutral rate which jumped up to 5.25% in August of 2023.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.