WEEK ENDING 12/16/2022

Highlights of the week:

- The Fed raises its targeted short-term interest rate by 50 basis points.

- Many market participants interpret Chairman Powell’s conference as “dovish.” But we view it as a reiteration of his Jackson Hole comments.

- Another marginally lower inflation measure lands, but the Fed’s 2% target is still far away.

- This is our last Week in Review for 2022. We wish all our readers happy and healthy holidays. We’ll see you in the new year.

A CITY DIFFERENT TAKE

The Treasury market continued to rally in the last week. Many market participants think the Fed is winning its war on inflation and is well on its way to 2% inflation. Yes, some major inflation measures look to have rolled over, but we feel it will take several subsequent lower inflation readings to confirm that thesis. Unemployment is still low, despite headline-grabbing layoff reports. And there are still more than 10 million unfilled jobs. This should support higher wage growth.

We feel that the fixed income markets have gotten a little ahead of themselves. This could come from a much-needed relief after a very difficult year. It is good to remind investors that the last few years of pandemic-induced quantitative easing (QE) and free money were an anomaly, not the norm. What the fixed income and equity markets have undergone this year is a reversion to the mean. Yes, it has been painful for those investors who have stretched for returns in the last couple of years. Events like the failures of so many SPACs, NFTs, and especially FTX are nothing more than the normal withdrawal symptoms from the drug of “free money.”

CHANGES IN RATES

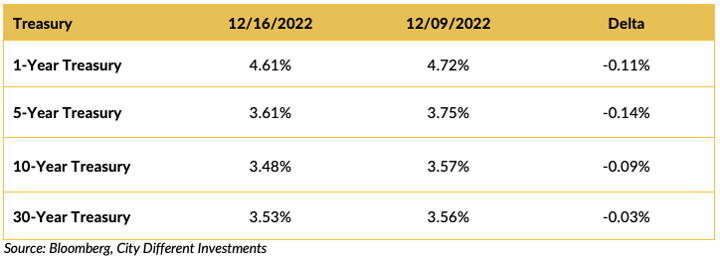

Treasury yields moved lower most of last week. Year-over-year CPI came in below expectations (7.1% vs. 7.3%) and last month’s reading of 7.7%. The core year-over-year reading followed the same trajectory: lower than expectations (6.0% vs. 6.1%) and below last month’s reading of 6.3%. As expected, the Federal Reserve increased its target short-term rate by 0.50%. Many market participants interpreted Chairman Powell’s comments at his press conference as dovish. We viewed them as a reiteration of his earlier Jackson Hole comments — a slower pace of increase to a higher-than-anticipated terminal rate in place for a longer duration.

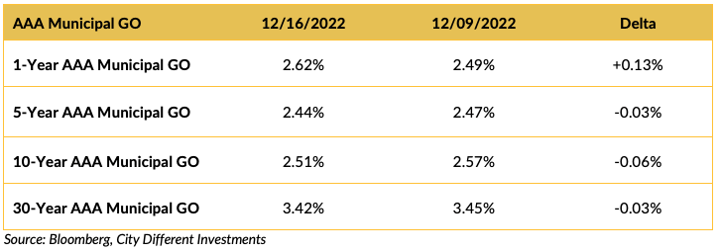

The municipal market mostly followed the direction set by the Treasury market.

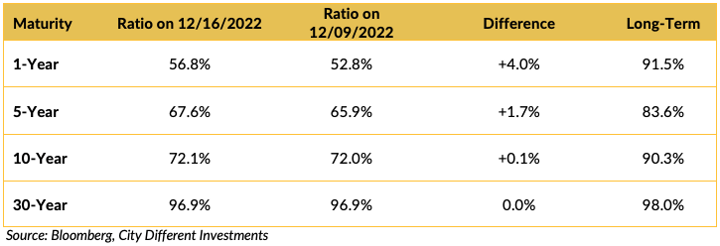

Most muni/Treasury ratios went mostly unchanged on the week. We continue to think market participants' enthusiasm for the potential of the January effect has gotten a little ahead of itself.

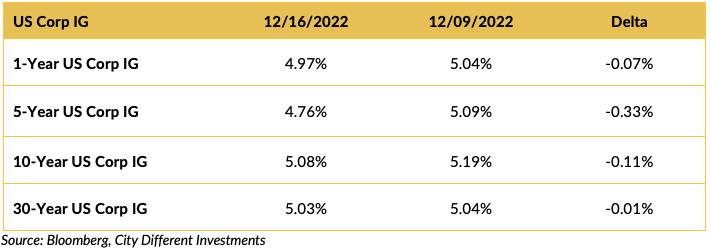

Five-year Investment-grade rates moved significantly lower on the week, outpacing all the other tenors listed above.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

It was a quiet week in Washington. Many are waiting for the January 6 committee’s final report. Anticipation is high as to what it includes or recommends.

The new Congress will be sworn in on January 3, and then the fun begins. If quotes like the following indicate what the new Congress has in store for the American public, then — oh boy!

In a video clip, Rep. Marjorie Taylor Greene was recorded as saying “I want to tell you something: If Steve Bannon and I had organized that, we would have won, not to mention, it would have been armed."

However, there is one bright spot—financial markets like gridlock in Washington. And with split control of the House and Senate, gridlock is almost certainly assured. Happy New Year!

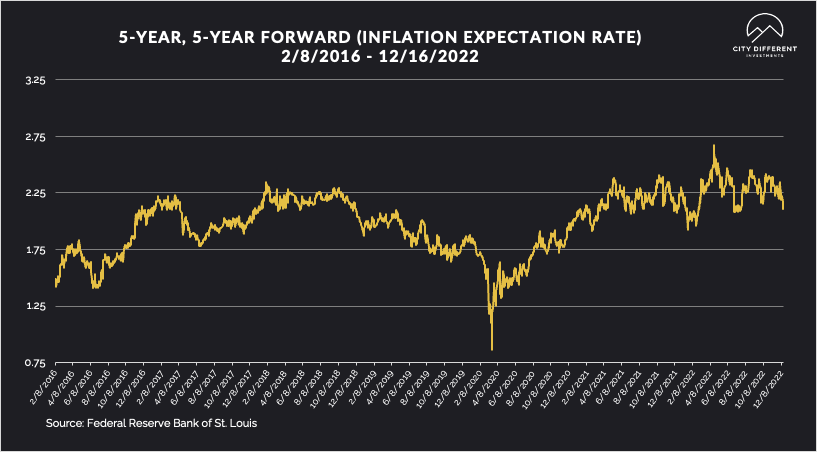

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended Friday at 2.12%, ten basis points lower than the December 9 closing of 2.22%. The 10-year Breakeven Inflation Rate ended the week at 2.13%, 13 basis points lower than the December 9 observation of 2.43%. Both of these readings seem low, given where inflation is today. These implied inflation measures have stayed consistently in the 2% neighborhood. These market participants must have greater faith in the Federal Reserve achieving its 2% inflation target than we do..

MUNICIPAL CREDIT

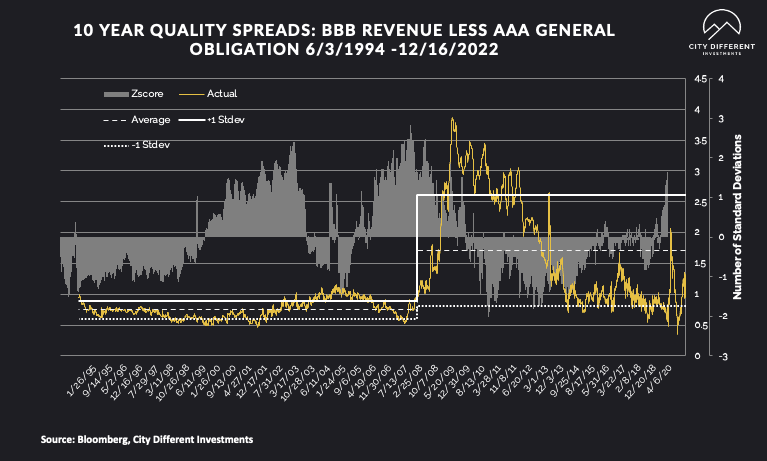

10-year quality spreads (AAA vs. BBB), as measured on December 16, were 1.26%. Higher than the December 9 reading of 0.94% and still below the long-term average of 1.72%. This reading is at the lower end of the fair territory (as we define it). We still do not think that investors are “getting paid” to take credit risk with forecasts of a recession on the horizon (even though we believe the likelihood of a significant recession is low). We would need quality spreads to move into the upper portion of fair territory before beginning a strategic position.

WHY IS THE MUNICIPAL MARKET BEHAVING THIS WAY?

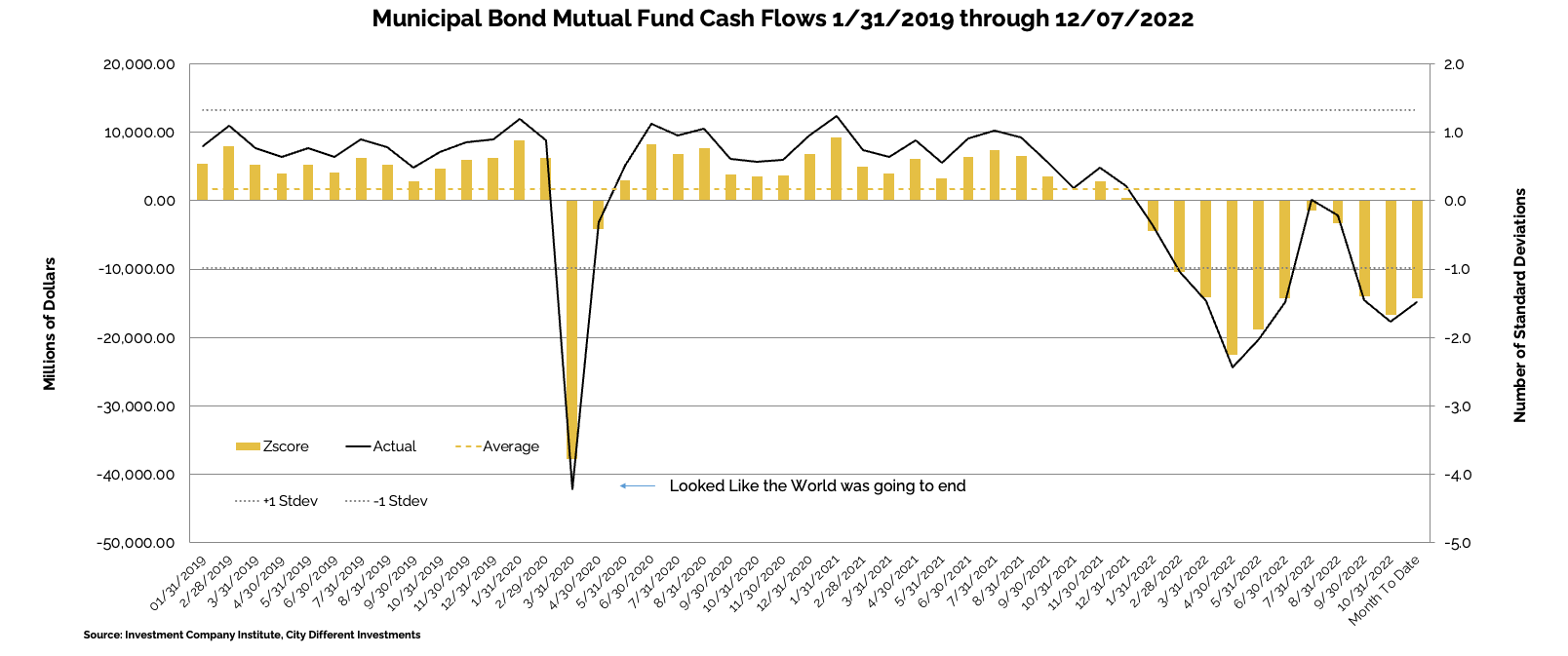

Various sources are used to report cash flows related to municipal bond mutual funds and ETFs, all reporting at different times. The source we have chosen to use is the Investment Company Institute (I.C.I.). The I.C.I. reported weekly cash flows from municipal bond mutual funds for the period ending December 7 was -$2.5 billion compared to -$2.6 billion from the week of November 30.

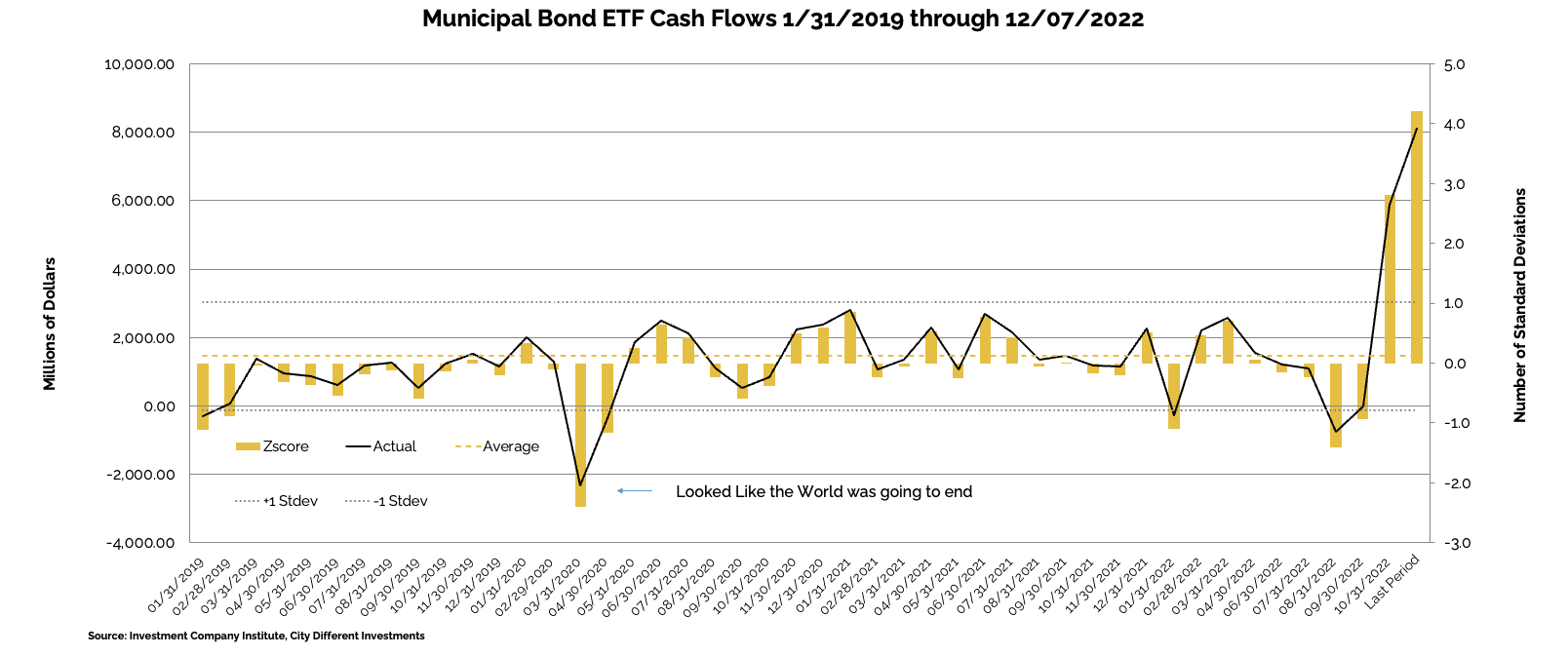

Municipal bond ETF cash flows for the same combined period were +$1.4 billion, roughly the same as the week of November 30.

Other cash flow sources:

In its Municipal Markets Weekly newsletter dated December 16, 2022, JP Morgan commented on cash flow data this week, stating that:

“Lipper reported combined weekly and monthly outflows of $1.2 billion for the period ending December 14, muni ETF inflows of $758 million, and open-end fund outflows of $2 billion. YTD outflows increased to a new record of $116.6 billion. HY funds recorded $128 million of outflows, Int. funds saw $525 million of outflows, and LT funds saw $524 million of outflows.”

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

In the same newsletter, JP Morgan reported:

“Next week, we expect total supply of just $269 million, or 9% of the 5-year holiday equivalent week average ($3 billion). We anticipate tax-exempt supply of $260 million (9% of average), and taxable/corp cusip supply of $11 million (4% of the average).”

CORPORATE INVESTMENT GRADE AND HIGH YIELD OVERVIEW

In its weekly "Credit Flows" report dated December 16, 2022, Wells Fargo commented:

“Who is buying US corporate bonds this year (IG+HY)? With much higher interest rates this year, not surprisingly net issuance of US corporate bonds declined to $353 billion from $876 billion last year. Given negative total return performance, bond funds and ETFs swung from net buying $394 billion US corporate bonds in 2021 to net selling -$20 billion in 2022.

Fundamentals update. IG gross leverage modestly improved in 3Q22, but net leverage was unchanged as companies deployed record outlays for share buybacks and dividends over the past year. In HY, leverage and interest coverage are healthy overall, but pockets of weakness have started to emerge beneath the surface.”

CONCLUSION

It has been a tough year for the fixed income markets (a brilliant observation, we know).

The curve is still very flat (if not inverted), and it appears to us that investors are not being paid to accept added duration risk. Many commodity-based inflation measures look to have turned over, but wages are still an issue. Yes, we have read the headlines about layoffs, but unemployment is still low, and more than 10 million jobs are currently unfilled.

On behalf of everyone at City Different Investments, we wish you all happy holidays and here’s to a better 2023. And remember, BARB — “Bonds Are Back.”

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.