In my last blog post, I talked about how “thinking like an endowment trustee” can provide a real advantage to both financial advisors as well as retail investors when thinking through your investing strategy. I serve on the endowment committee for a few nonprofits in the Santa Fe, NM area, and I’m constantly thinking about how to improve year-over-year, decade-over-decade returns for these organizations I support and love.

To that end, we recently conducted a thought experiment here at City Different Investments — how could we improve the investment performance above and beyond the endowment consultants' current recommendation? We wanted to deviate from the passive investment strategy recommended by the consultant in favor of a core-satellite investment approach (the core portfolio usually consists of low-cost, passive investments while the satellite portion typically consists of more active investment strategies).

To test our thought experiment, we’ve been tracking both the underlying performance and volatility of this core-satellite strategy against the consultant’s recommended model.

** spoiler alert — the results look great **

Let’s see that strategy in action, shall we?

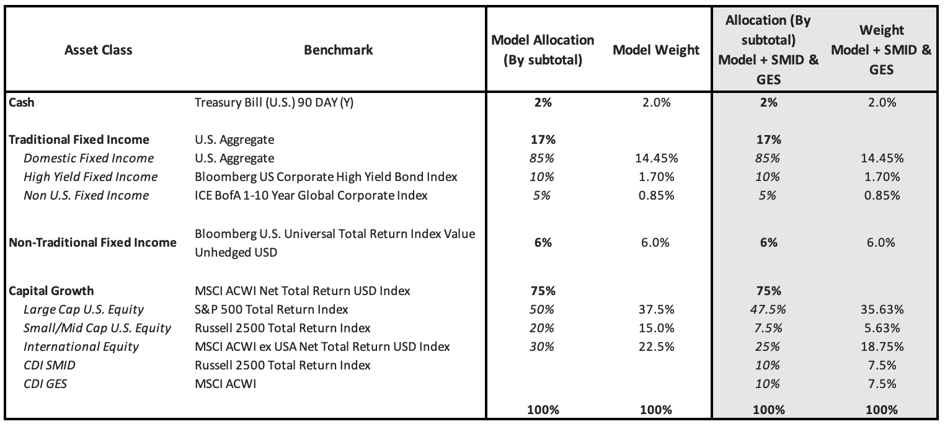

👆The first two columns are how the endowment consultant’s model allocates and weights its chosen investment vehicles.

Within our approach, we made some notable tweaks to the strategy:

We adopted a core-satellite approach as our main departure from the consultant’s model [e.g. we allocate ~ ½ of the relevant allocation to passive, and ½ to our SMID Cap Core (SMID) and Global Equity Strategies (GES)]. We took the 20% small/mid-cap allocation and put 10% into the CDI SMID strategy. We also took 10% of the Equity (Capital Growth) allocation and put it into the CDI GES strategy (this came via 2.5% from Large Cap US, 2.5% from Small/Mid Cap US, and 5% from International Equity).

So what did this do for us?

Over the trailing 1-year period, returns increased and volatility declined.

→ One of the interesting sub-points about the volatility decline is that the strategies we substituted actually contained more volatile securities than the parts of the consultant’s allocation that we replaced (the CDI securities have about 19% volatility in each strategy, vs. an average of 12.7% in the model component we’re replacing). BUT, overall volatility when including the CDI strategies declined.

So why does overall volatility decrease when we layer in two strategies with higher volatility? We think it’s because our covariance is so low vs. the part of the portfolio we’re replacing.

→ Modern Portfolio Theory has a lot to say about why this lower covariance results in more efficient returns, which we’ll cover in a couple of sections.

So what's the takeaway?

It’s about utilizing active management in your investment portfolio. If you’re paying active management fees, we believe you should be in focused, actively managed strategies — not benchmark-hugging investment portfolios with index-like returns.

To that end, if you’re going to use a core-satellite approach like the example above, then your satellite securities should look different than the rest of the portfolio (and whaddya know… that’s exactly what the CDI strategies above show 🤣 )

Chasing the efficient frontier

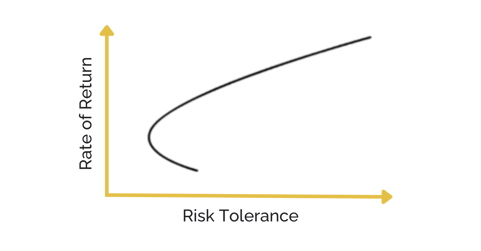

There’s an important theory of investing at work here — it’s called “the efficient frontier.” Basically, the efficient frontier is the set of optimal allocations within investment strategies that offer the highest expected return for a defined level of risk (or the lowest risk for a given level of expected return).

The efficient frontier, when turned into a graph, represents the optimal distribution of risk to returns:

The efficient frontier graphically represents portfolios that maximize returns for the risk assumed. The returns are obviously dependent on the investment combinations that make up a given portfolio. An individual strategy’s standard deviation is a proxy for risk. Ideally, an investor is trying to fill their portfolio with securities offering exceptional returns BUT, when combined, offer portfolio-level standard deviation that is lower than the standard deviations of the individual strategies (the exact thing that happened when we replaced the consultant’s allocations with higher-volatility individual strategies… we got a less volatile portfolio overall).

The efficient frontier theory holds that the less synchronized the securities (lower covariance), the lower the standard deviation (read: risk). So, there is a world in which you can move higher along the efficient frontier — increasing returns while lowering overall volatility — by leaning into more volatile individual instruments… just so long as you nail the diversification of those individual securities.

→ A key finding of the concept was the benefit of diversification (seen in the curvature of the efficient frontier). The curvature was integral in revealing how diversification improves the portfolio's risk/reward profile. It also showed that there is a diminishing marginal return to risk.

All that to say — you can potentially increase returns AND decrease risk using a core-satellite approach to investing (whether for endowments or investing more generally). When selecting active managers for the satellite exposure, make sure that exposure looks different than the rest of the portfolio (lower covariance). One easy way to ensure “different” is to look for focused managers. As we have demonstrated with our core-satellite example above, you can both improve returns as well as reduce volatility if you diversify your portfolio with the right active strategies.

IMPORTANT DISCLOSURES

The information and statistics contained in this communication have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or forecasts discussed herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. This information is to be used as the basis for discussion and is not to be considered projected performance. This analysis is not intended to convey any guarantees as to the future performance of the investment strategies, asset classes, or assets depicted. Any projections, market outlooks, or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results. Benchmark definitions are available upon request

The objective of the SMID Cap Core strategy is to generate strong risk-adjusted returns in a focused portfolio of small and mid-cap stocks invested across the business life cycle. Portfolios invest primarily in U.S. stocks with greater than $100 million in market cap. Portfolios typically hold between 20-35 positions, with no position representing more than 10% of the portfolio. Not less than 80% of portfolio assets will be invested in companies whose market cap is within the market cap range of the Russell 2500 Index. The strategy may take on international exposure up to 25% of portfolio assets. An investment in the strategy is subject to certain risks. The value of an investment may fall as well as rise and is not guaranteed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. The strategy could be more volatile than the performance of more diversified portfolios.

The objective of the Global Equity strategy is to generate strong risk-adjusted returns in a very focused portfolio of global equities. Portfolios invest primarily in stocks of companies with greater than $100 million in market cap selected on a worldwide basis. Portfolios typically hold between 20-30 positions, with no position representing more than 10% of the portfolio at time of purchase. An investment in the strategy is subject to certain risks. The value of an investment, and income generated (if any) may fall as well as rise and is not guaranteed. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. The strategy could be more volatile than the performance of more diversified portfolios.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, or any non-investment related content made reference to directly or indirectly in this communication will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. No discussion or information contained herein serves as the provision of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability above to his/her individual situation of any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal, tax, or accounting advice.