.png)

Among the things I’ve been lucky enough to do in my professional life in Santa Fe, NM, two stand out: I’ve enjoyed a successful career in finance and have been involved with several nonprofits throughout the city and state. Sometimes, those two stories collide wherein I find myself serving on a nonprofit’s endowment committee. And while I love the opportunity it gives me to mix two of my passions under one roof, it also carries a real gravity… You’re entrusted with the financial future of an organization whose mission you believe in deeply. It’s a responsibility and privilege I do not take lightly, but it also provides me with a valuable lens to view financial investing.

Let me explain…

Time horizons

Every financial advisor worth their weight will preach a diversified, long-term time horizon. But few investors truly operate on a multi-decade strategy year in, year out, decade after decade… yet that’s exactly what we’re tasked with on an endowment committee. The time horizon, by definition, is multi-decade, which allows us to make investment recommendations that fit that time horizon not only in theory but also in practice.

What this means for the moment

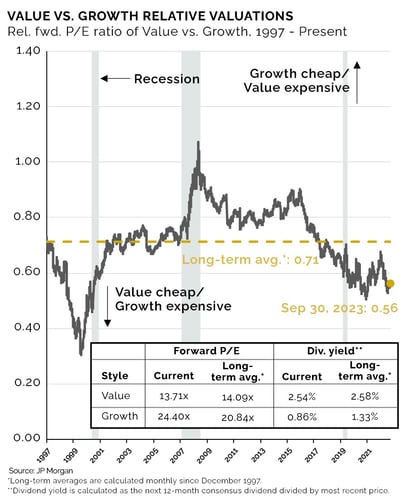

Right now, value is still relatively cheap, whereas growth is relatively expensive. That’s not always true, obviously — there will be periods when growth or value is cheap relative to long-term averages… but it’s incredibly difficult to tell how long the respective over- or under-valuation will last. For now, if we think value is still currently cheap compared to the long-term average, it might make sense to overweight value for a time (especially on such a long investment horizon).

Weighting strategy

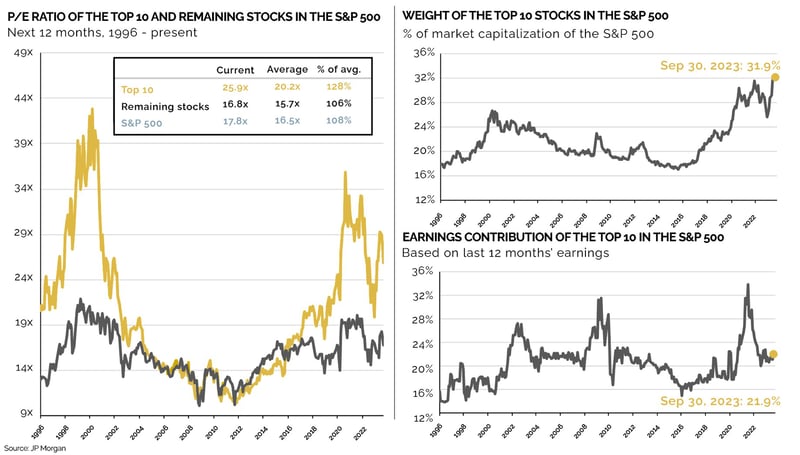

Another mistake we see some endowments making right now is plowing a huge percentage of their holdings into the S&P 500 or Russell 2000 as benchmark funds. Now, we’re not saying endowments should have no exposure to these indexes, but the underlying math is getting a bit topsy-turvy.

For instance, at the end of September, the top 10 stocks within the S&P 500 made up the largest weight of that index over the last 27 years… at a whopping 32% of the entire index. Beyond that, those 10 stocks are trading at almost 28x P/E as of September’s end. Now, that’s not an all-time high, but it’s almost 8 times more than the long-term average.

While the S&P 500 might sound like a diversified investment vehicle… you’re putting an awful lot of eggs in 10 baskets.

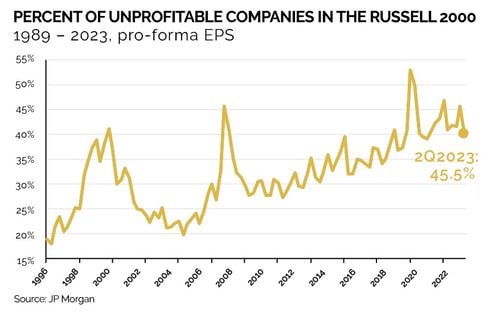

Likewise with the Russell 2000 — the percentage of unprofitable companies within the index is at an all-time high (excluding a blip during Covid when small companies had unusually depressed earnings).

Market-cap musings

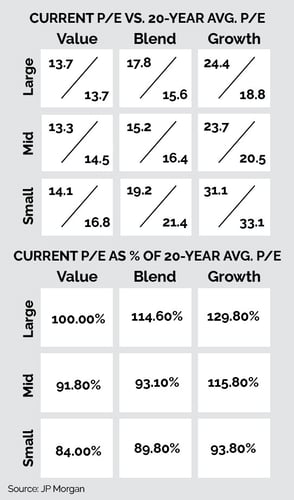

Currently, Large + Growth stocks are trading at higher P/E vs. their respective 20-year averages whereas Blend Small / Mid are trading at relatively attractive valuations vs. 20-year averages (and is more stable if we consider the over/under-valuation of value/growth over the long term). Value Small / Mid might seem cheap, but it’s hard to tell if it’ll stay cheap for much longer.

What does all this mean? A balanced + basket approach might make more sense at this stage (which we’ll outline in just a second).

Time for a vacation?

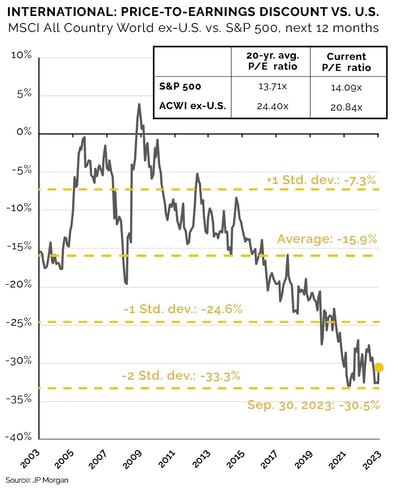

The final thing we’re looking at through the lens of endowment investing is the disparity between international and U.S. stocks.

U.S. stocks are well above their average valuation, but international stocks are lagging behind theirs. So much so that the valuation spread between them is at almost two standard deviations:

Of course there have been periods of U.S. equity outperformance before… but never for this long (almost 15 years!). While we’re bullish on U.S. equities generally — especially with AI and Machine Learning innovations being spearheaded here (plus the usual friendly business climate and relatively mobile workforce) — we’re also leaning into higher international exposures within the limits of policy benchmark allocations.

Baskets all the way down

As I teased a couple of sections ago, our primary investing strategy at CDI (and often what I preach to my endowment committees) rests in our “basket approach.”

Rather than limit our exposure in a focused portfolio (20-35 holdings) to the sector weights in an index, we take a differentiated approach to diversification.

More important than lining up sector exposures, we believe the best approach to diversification is to focus on types of businesses — what we call our baskets:

- Emerging Businesses (<25%): Companies in the process of establishing a leading position in a product, service, or market with the potential for above-average growth.

- Established Businesses (30-50%): Businesses that exhibit steady earnings growth or cash flow and above-average profitability. These often sell at above-average valuations.

- Mature Businesses (30-50%): Financially sound, economically sensitive businesses, usually selling at low valuations relative to net asset value or potential earnings power.

Within any of these basket types, we have room to flex given the prevailing economic conditions; but the strategy is built on achieving real, long-term diversification without an overreliance on a heavily weighted S&P or oft-unprofitable Russell 2000 holdings.

IMPORTANT DISCLOSURES

The information and statistics contained in this communication have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or forecasts discussed herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results. Benchmark definitions for the S&P 500 and Russell 2000 are available upon request.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, or any non-investment related content, made reference to directly or indirectly in this communication will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. No discussion or information contained herein serves as the provision of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability above to his/her individual situation of any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal, tax, or accounting advice.