WEEK ENDING 6/5/2026

- Iran conflict, oil prices, driven off front pages

- This is jobs week

- Fear vs. greed: which is winning?

- 82nd anniversary of D-Day

A CITY DIFFERENT TAKE

The war in Iran and rising oil prices were driven off the front page of the Wall Street Journal, replaced with reporting on the big jobs surprise and the proposed IPOs of SpaceX and Anthropic.

The Iran conflict is ongoing, and it is getting difficult to know who to trust for updates on current conditions. Futures prices of West Texas Intermediate (WTI) in New York finished the week at $90.54 per barrel, up from last week’s close of $87.36 per barrel.

But the big news this week was Friday’s jobs numbers release:

-

Change in nonfarm payrolls up 172,000 vs. expectations of +88,000. The revised two-month revision was +93,000 vs. the prior -16,000. The three-month revision was +79,000 vs. the prior +48,000.

-

The unemployment rate stayed steady at 4.3%.

-

Average hourly earnings Y/Y were 3.4%.

-

The last read on the Personal Consumption Expenditure (PCE) Index was 3.8%. The quick evaluation is that wages are not keeping up with inflation (we disregarded core PCE because, unlike economists and the FED, the public drives and eats).

Other employment related measures:

- JOLTS survey, which measures the number of job openings, are above their long-term averages (7,618 vs. 5,736)

- JOLTSQUIS, which tracks voluntary job separations, were a little below its long-term average (1.9 vs. 2.0)

- JOLTLAYS, which tracks involuntary job separations, are below its long-term average (1.1 vs. 1.34)

The employment picture looks OK, but not robust. The fact that wages are not keeping up with inflation (Average Hourly Wages Y/Y delta 3.4% vs. PCE Y/Y delta 3.8%) could explain why the last read of the University of Michigan Consumer Sentiment Index was at more than a 20-year low of 44.8.

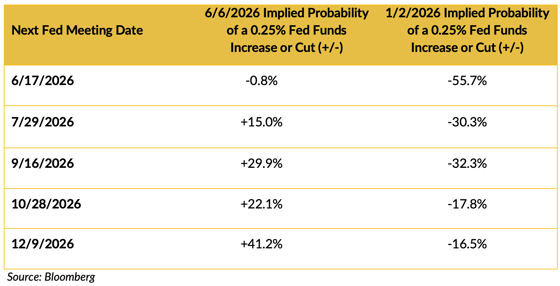

What does all this mean? The market’s implied probability of a Fed funds rate cut this year is quite different from the beginning of the year, even with a new Fed chair. The following table shows how the market’s odds for a Fed rate cut has changed this year:

Much has changed in the last six months. What does it all mean in English? The fear of rising inflation has overtaken the fear of an employment-led recession.

Speaking of fear, Warren Buffet popularized his investing philosophy with this statement:

“Be fearful when others are greedy and greedy when others are fearful.”

SpaceX’s long anticipated IPO of $75 billion, and Anthropic’s proposed IPO:

“Anthropic submitted confidential paperwork for an initial public offering on Monday, the first step in what could be a blockbuster debut for the $965 billion company. The filing with US regulators is another entry in what looks to be a historic year for IPOs as artificial intelligence labs vie to fund their expensive research. Another Big IPO

Bringing Buffet’s philosophy into focus, it looks like the owners of these two businesses are cashing out. Or, as Ray Dalio put it in a recent Bloomberg article, “Dalio Sees AI Bubble Bursting as Wealth Is Converted Into Money”

“‘Bubbles pop when it comes time to capitalize on investments,’ Dalio said, noting concerns about the profitability of AI companies. ‘The pricking is the converting of wealth into money,’ he said. Today’s AI-driven market is ‘following that kind of path, even though it is a wonderful technology.’” Fear or Greed?

Should we be fearful or greedy? That’s the question facing all investors. At CDI, we choose to be a little fearful. Good luck!

CHANGES IN RATES

TreasuryMarket

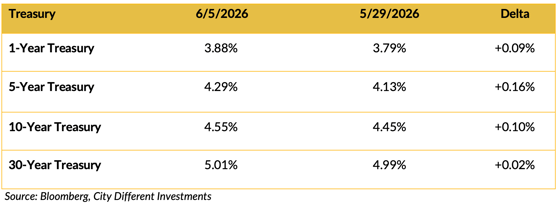

Treasury yields moved higher last week because of some positive employment data. The 2/10 spread flattened to 38 basis points. The Treasury market has moved from anticipating a Fed cut of short-term interest rates to anticipating an increase in short-term interest rates.

Municipal Market

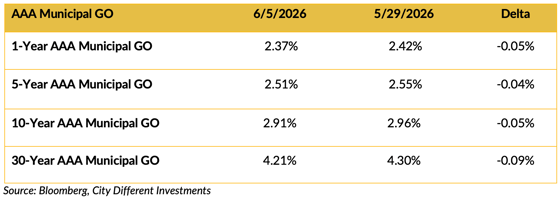

AAA general obligation municipal bond yields were also lower over the week. Municipal bonds have gotten very expensive when compared to their Treasury equivalents. The 2/10 spread was marginally unchanged at 0.5%.

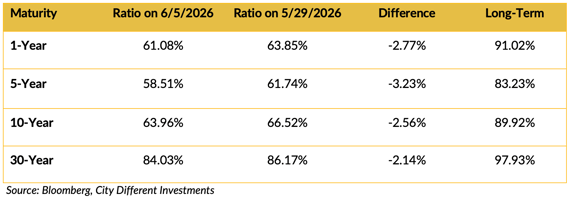

Selected Municipal AAA General Obligation Bond / Selected Treasury Bonds Yield Ratio

The muni/Treasury ratios got richer last week. AAA general obligation municipal bond is now priced well through their breakeven taxable equivalent at the 37% federal income tax rate. Municipal money market funds are even richer. The seven-day SEC yield ration is now sub 50%.

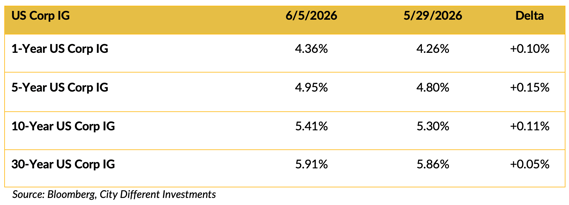

Investment Grade Corporates

Investment grade corporate yield adjustments were more in line with the Treasury market yield adjustment. Corporate quality spreads did not move. The 2/10 spread is 87 basis points.

THIS WEEK IN WASHINGTON

The Senate passed the $70 billion border enforcement bill:

“Lawmakers of both parties objected to the Trump fund over concerns that taxpayer money would be used to compensate the president’s allies and could reward people who had assaulted police officers who defended the Capitol on Jan. 6, 2021 as it was overrun by a mob of Trump supporters. Republicans were particularly incensed because the fund and an agreement to end audits of Trump’s taxes were announced just as the president helped to end the Senate careers of two GOP lawmakers he saw as insufficiently loyal — Sens. Bill Cassidy of Louisiana and John Cornyn of Texas. Incensed

The definition of “incensed” does not call for action (good for the Senate):

“Incensed is an adjective that means to be extremely angry, enraged, or infuriated. It describes a state of deep outrage, often triggered by something perceived as unfair, unjust, or deeply disrespectful.” Definition

Incensed is the right word because nowhere in the definition does it say the individual or body is angered enough to take corrective action. No more tax audits — only in this America!

The president had a call with Prime Minister Benjamin Netanyahu on Monday over Isreal’s escalation in Lebanon, which got petty heated.

“President Trump lashed out at Israeli Prime Minister Benjamin Netanyahu over Israel's escalation in Lebanon in an expletive-laden call on Monday, two U.S. officials and a third source briefed on the call told Axios.” F Bombs Dropped

WHAT, ME WORRY ABOUT INFLATION?

The graph above contrasts a 5-year Breakeven Inflation Rate (this is the market-implied inflation rate) tracked weekly with the core PCE inflation rate. The 5-year Breakeven Inflation Rate finished the week of June 5 at 2.48%. The 10-year Breakeven Inflation Rate finished the period at 2.36%.

MUNICIPAL CREDIT

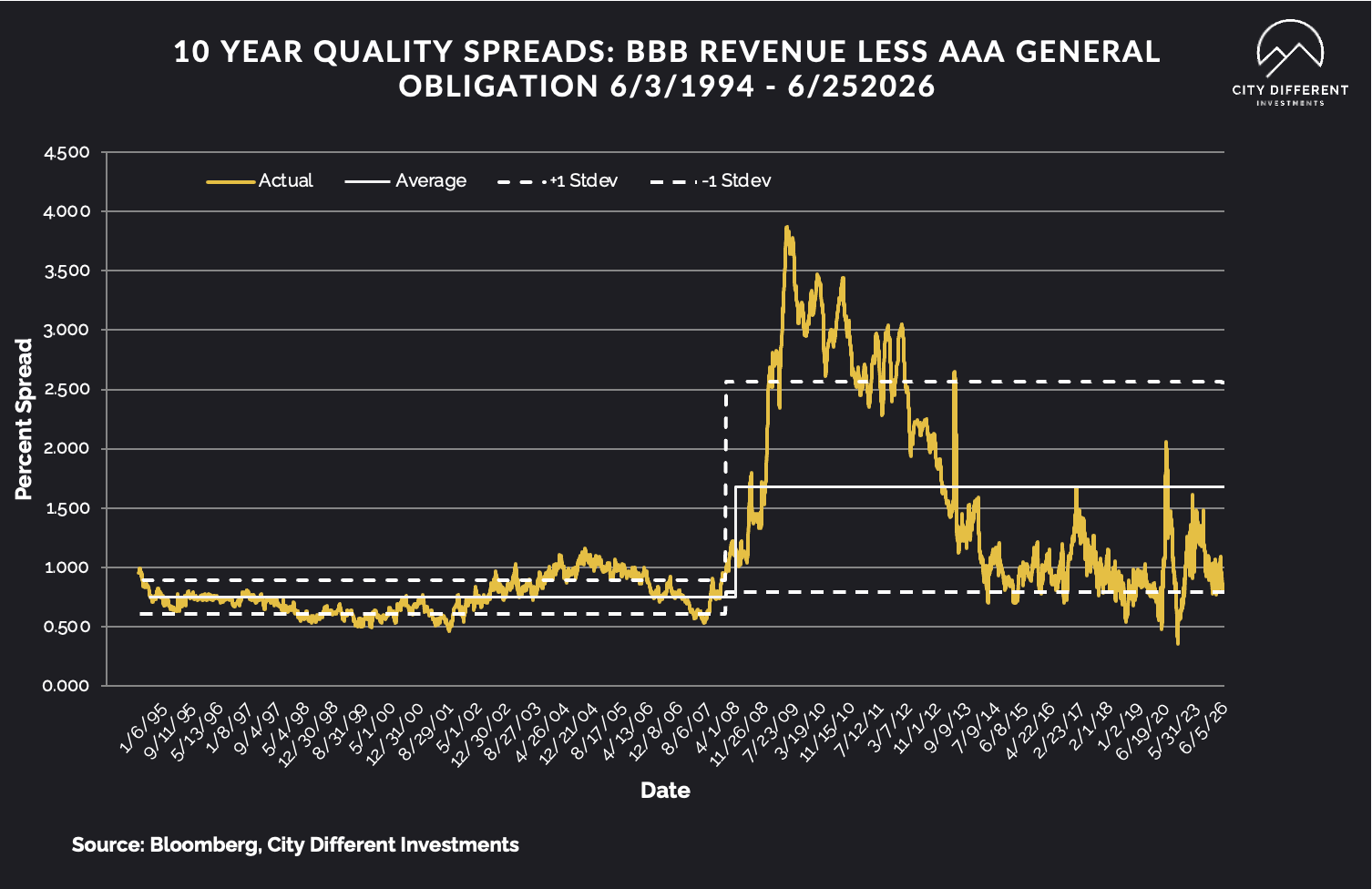

Last week's 10-year quality credit spread between BBB revenue bonds and AAA general obligation bonds was 0.86%, virtually unchanged week over week. The historical average credit spread is 1.67%.

TAXABLE CREDIT

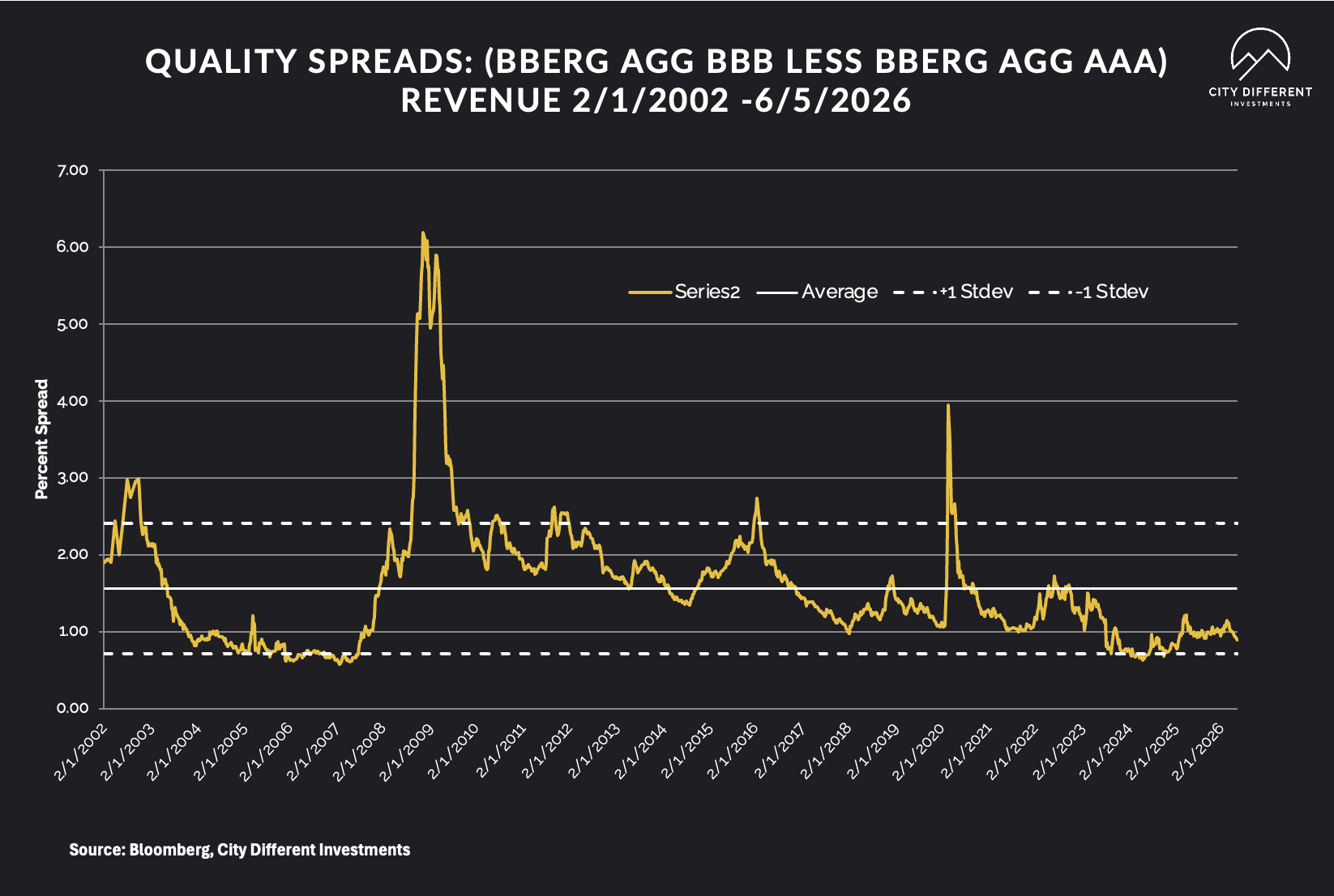

Investment-grade spreads for the past week were at 89 basis points. The long-term average for investment grade is 1.56%. High-yield credit spreads are 2.64%.

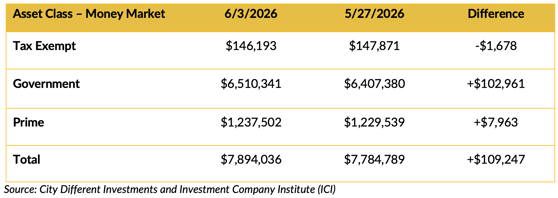

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market fund flows were positive overall but nuanced underneath that. Tax-exempt money market was negative last week.

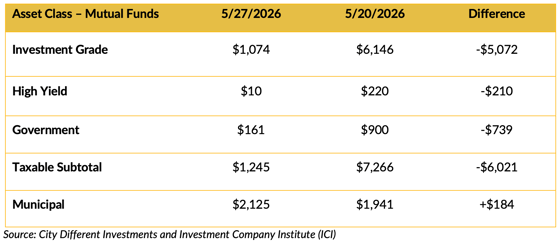

Mutual Fund Flows (millions of dollars)

Mutual fund flows were mostly negative. However, municipal high funds saw positive flows.

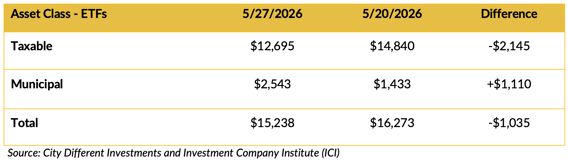

ETF Fund Flows (millions of dollars)

Net ETF flows were mixed week over week.

SUPPLY OF NEW ISSUE BONDS

Supply continues to dominate the muni market. This week’s calendar is extremely robust at $13 billion. June is a strong supply month for munis, but it has been met with strong demand.

CONCLUSION

Given the jobs reports this week, it is easy to predict that inflation is the Fed’s main fear. The market agrees given the changes in implied probabilities over the last six months. As we head into the summer, the municipal market looks very expensive relative to its taxable equivalents, and municipal national money market funds look even more expensive than bonds. This is not an out-of-the-ordinary event. We expect the money market ratios to fall back in line as municipal issuers come to market with their annual note issuance. The question is how long the reevaluation will take.

Saturday, June 6, was the 82nd anniversary of the D-Day invasion of Europe, the beginning of the ultimate defeat of the Axis powers. There are very few members of the Greatest Generation still with us, so it is up to us (their descendants) to not forget their sacrifice.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein is available upon request.