WEEK ENDING 3/22/2024

- We will not be publishing a Weekly Commentary next week. We wish you all a happy holiday!

- The Capitol Hill Greatest Hits: “Another One Bites the Dust” & “Burning Down the House”

- The market takes Chair Powell’s comments to be dovish.

- Last-minute vote on spending bill avoids government shutdown.

- The municipal bond market begins the cheapening process.

A CITY DIFFERENT TAKE

The Federal Reserve had a two-day meeting last week and announced short-term rates will go unchanged. The fixed income markets seemed to take Fed Chair Powell’s comments on possible rate cuts quite constructively. But we heard a different message.

Our interpretation is that the economy seems to be doing just fine, even with a restrictive fed funds policy. And with the presidential election looming, there is no need to cut short-term rates. Changing economic data could push the Fed in an even more dovish direction.

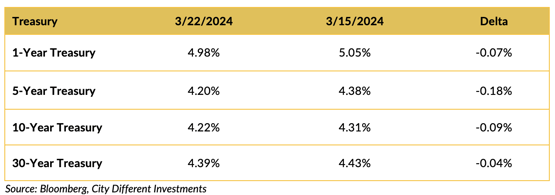

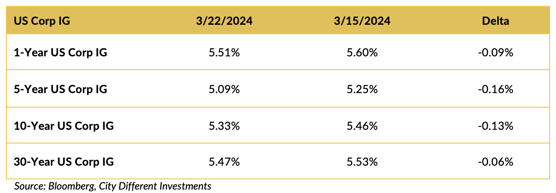

CHANGES IN RATES

Treasury rates moved lower on the week. The market took Powell’s press conference as somewhat bullish for rates. Of course, this is the same market that took the three possible rate cuts discussed at December’s news conference and turned those into six rate cuts in the spring. We can’t remember — how many spring cuts have we seen? Markets do tend to overreact. We heard a steady-as-she-goes message based on incoming data. The economy seems to be doing just fine, even with a restrictive federal funds rate.

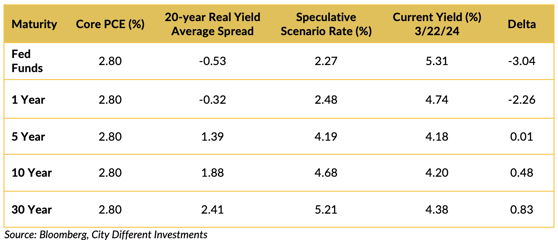

Here is a little bit of speculation. What if the Fed accepted core PCE inflation at 2.8% and the 20-year average real yield spreads were reestablished? What would that mean for the yield curve?

The following table illustrates that speculation:

Conclusion: Short-term rates decrease a lot and long-term rates increase. When these rate changes are magnified by the securities duration, the returns are eye-popping.

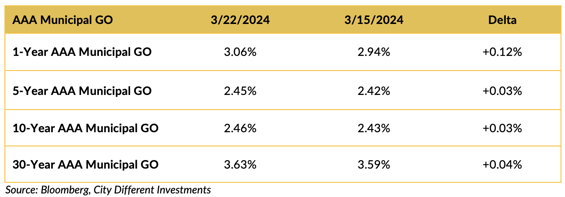

The municipal market’s yields moved higher on the week. The market is seeing an increase in supply which acts to revalue an already rich (relative to taxable securities) municipal market.

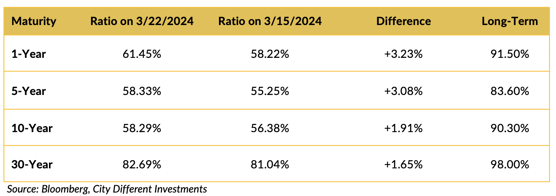

The municipal/Treasury ratios increased last week as the municipal market was hit with a seasonal increase in new issue supply. This could be signaling an end to the January effect.

This market segment followed the Treasury markets and saw lower rates last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

It seems like we avoided another partial government shutdown. Thank goodness for a late-night Senate vote. Now let’s check out the Weekly Top 40:

“Another one Bites the Dust” (1980, Queen — for those born after 2000)

Wisconsin Republican Rep. Mike Gallagher announced he will resign from Congress effective April 19, joining fellow Republican Rep. Ken Buck of Colorado (who is leaving after this week) — thus, shrinking the Republican majority in the House.

“Burning Down the House” (1983, Talking Heads — also for those born after 2000.)

Hard-right Rep. Marjorie Taylor Greene filed a motion to oust House Speaker Mike Johnson.

“Ah, watch out/You might get what you’re after.

Cool babies/Strange but not a stranger.”

We don’t know how far Greene’s motion will get, but who would want that Speaker job after this?

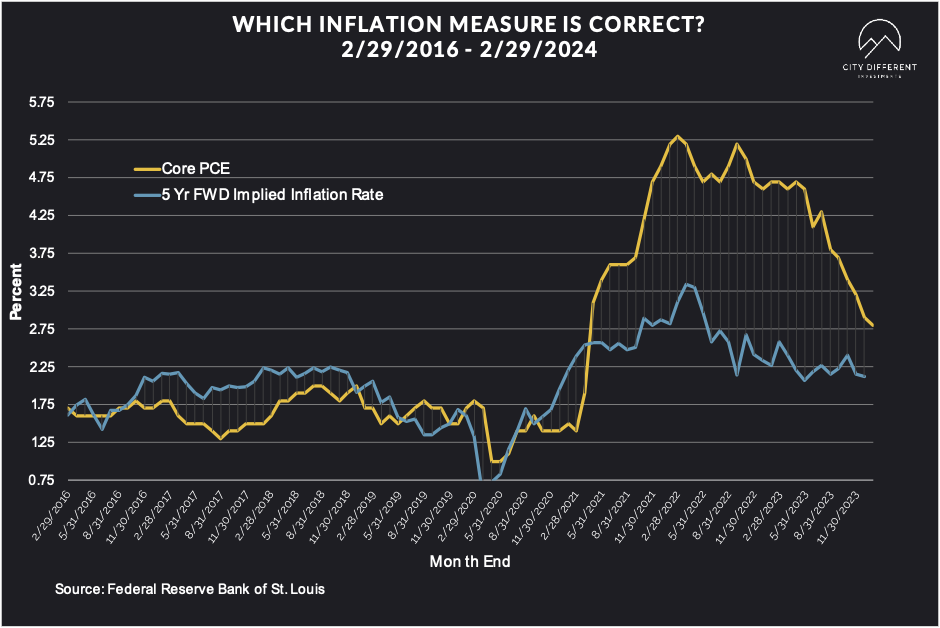

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week of March 22 at 2.41%, 16 basis points higher than the March 15 close of 2.25%. The 10-year Breakeven Inflation Rate finished the week at 2.35%, three basis points higher than the close of March 15.

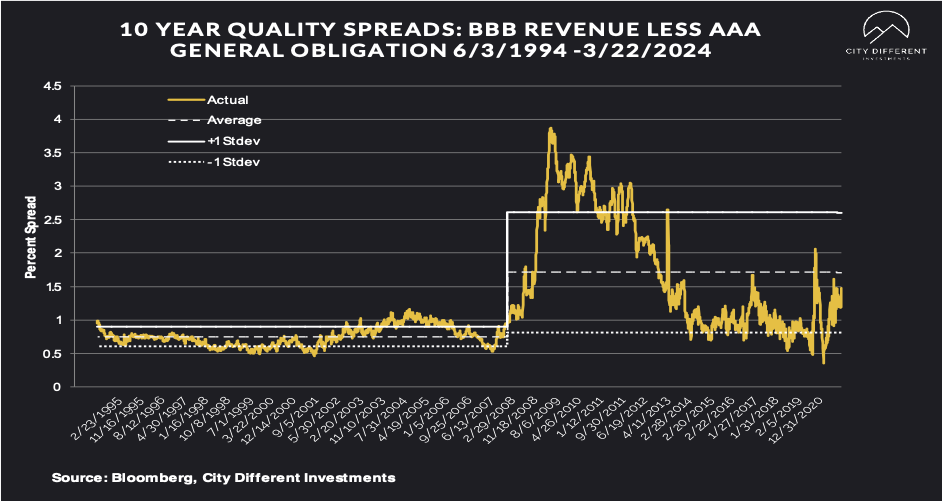

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of March 22 were 1.22%, two basis points higher than the March 15 reading of 1.20% (based on our calculations). The long-term average is 1.71%.

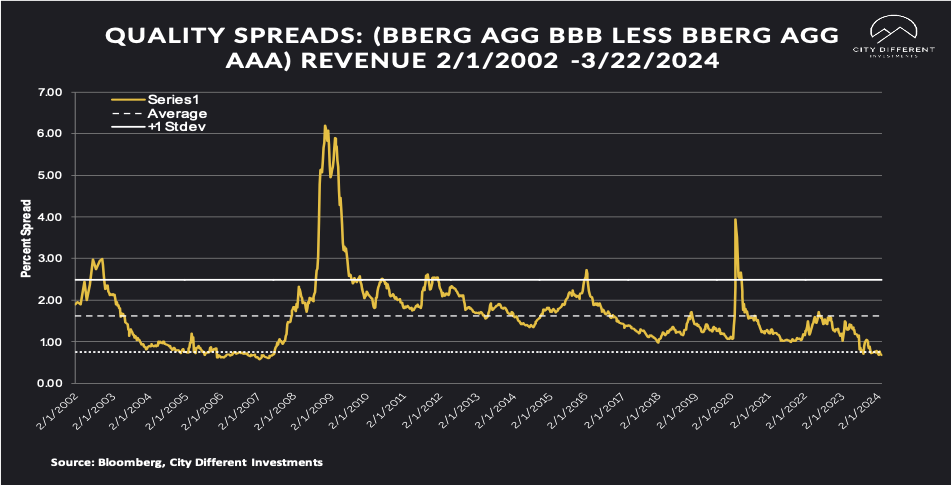

Quality spreads in the taxable market are not attractive but were slightly lower, ending the week at 0.68%, two basis points lower than last week. High-yield quality spreads were 2.64% on March 15.

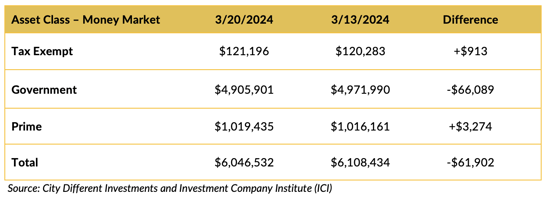

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds still see positive cash flows. Their yields are hard to beat, even if the duration is in question.

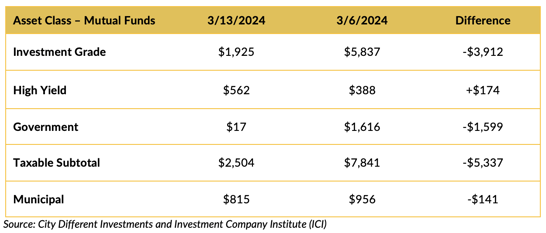

Mutual Fund Flows (millions of dollars)

Bond funds saw a reduction in cash flows.

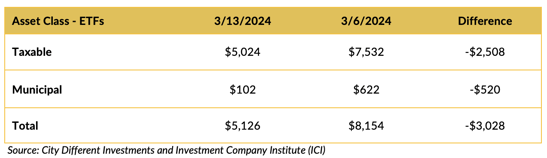

ETF Fund Flows (millions of dollars)

ETF Funds saw reduced inflows compared to the week prior.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Supply for the municipal tax-exempt calendar will likely hit $9.2 billion in the holiday- shortened week.

CONCLUSION

The market viewed Chair Powell’s press conference as dovish. This is the same market that took December’s indication of three rate cuts this spring and turned that into six rate cuts. Granted the first day of spring was last week — but how many rate cuts have we seen? So, we may be a little aggressive in our critique. The yield curve is still inverted, and some investors think it is time to extend duration to capture higher yields. We feel that better risk-adjusted total returns may be found in the shorter maturities where we get paid to wait for a steeper yield curve.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.