WEEK ENDING 3/15/2024

• Higher than expected core CPI and PPI.• FOMC should leave rates unchanged on Wednesday.

• What’s a better buy? A 3-year T-bill or a money market fund?

A CITY DIFFERENT TAKE

Core inflation in February turned out to be higher than expected. Headline CPI surprised to the upside by 0.4% with core index (not including food and energy) also rising 0.4%. The “supercore” CPI measure (core services excluding tenants’ rent and owners’ equivalent rent), came down to 0.5% in February from 0.8% a month ago. These numbers show that inflation is anything but linear. Core CPI is at 3.8% year-over year.

Headline PPI also trended to the upside. Headline PPI doubled expectations, rising by 0.6% in February. The jump came from higher gas prices. Year-over-year headline PPI is just under 2%, but core is at 2.75%.

Fixed income markets responded to higher inflation numbers with a jump in yield of 15 to 20 basis points across the curve.

Both the CPI and the PPI reports are very meaningful numbers for the Federal Reserve, which meets this week. And this will not be a boring meeting. Sticky inflation and strong economic growth will make things interesting. Plus, back-to-back increases in inflation this year (for the months of January and February) will strengthen the Federal Reserve’s conviction of a higher-for-longer pause before a rate cut. (Every Fed participant has hinted at leaving rates unchanged for now.)

We will also get a refreshed dot plot out of this meeting, as well as an update on quantitative tapering. We’ll also be watching the Fed for their summary of economic projections — the Fed’s take on the economy. This includes GDP growth forecasts, unemployment estimates, and PCE and core inflation forecasts.

Currently, the market is predicting an 85-basis-point rate cut for 2024, starting in June. The Fed dot plot suggests three 25-basis-point cuts with equal distribution for this year. The Fed’s dot plot and market expectations are coming closer to alignment than they were in December of 2023.

CHANGES IN RATES

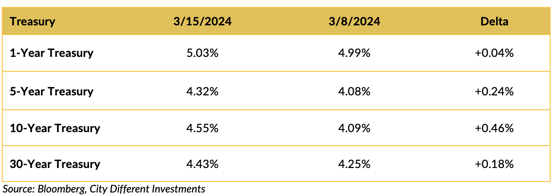

Treasury rates moved up significantly across all tenors and continue to build upon rates that have risen from last week.

At CDI, we ran some mathematical scenarios of solely yield basis calculating. So, what’s a better buy — a three-year Treasury bill or a money market fund?

Assuming T 4.25 3/15/2027 yielding 4.36% on a three-year Treasury bond and 3 Month Tbill as a Proxy for money market yielding 5.25% here are our conclusions:

- Our math indicates that if it takes two years for real rates to come back to the historical average, then you break even. It doesn’t make a difference which one you own.

- However, if rates break even in less than two years, then you win by holding a three-year Treasury bill over a money market fund.

- Conversely, if rates do not break even in less than two years, then the money market fund wins over the three-year Treasury bill.

Rates rose on the shorter part of the curve.

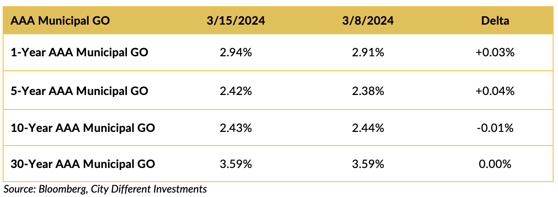

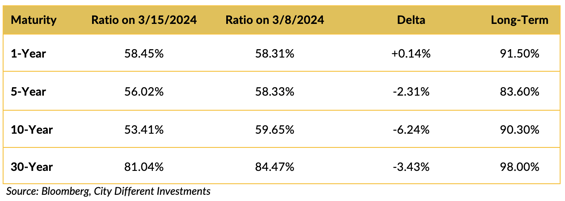

The municipal/Treasury ratio got more expensive in the 1–10-year part of the curve. Ratios are rich relative to Treasury and also to U.S. corporates.

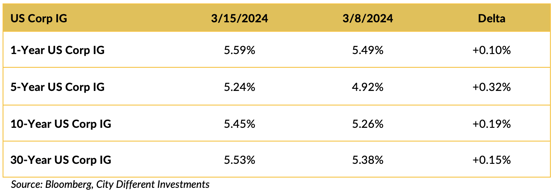

Rates in the corporate market segment followed the Treasury market and rose significantly.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Russia’s election results showed Putin winning 87% of the votes, extending his term as president by another six years. This also makes Putin the longest-serving president in the country’s history. While the outcome of the election is not surprising, it is worth acknowledging the inevitable extension of Putin’s war in Ukraine.

Last week, we talked about the bipartisan support for TikTok legislation, essentially banning it across the country. This will be an interesting and long road with several litigation leading to decisions between national security and free speech.

Former President Donald Trump made some notable threats and suggestions on the campaign trail. Trump threatened 100% tariffs on cars made in Mexico by Chinese companies. He later suggested he would replace the Federal Reserve chair if elected president.

Meanwhile, President Biden’s reelection campaign is well underway with a massive war chest. According to the media, Biden sits on $155 million — the highest campaign fund total of any Democratic candidate in history.

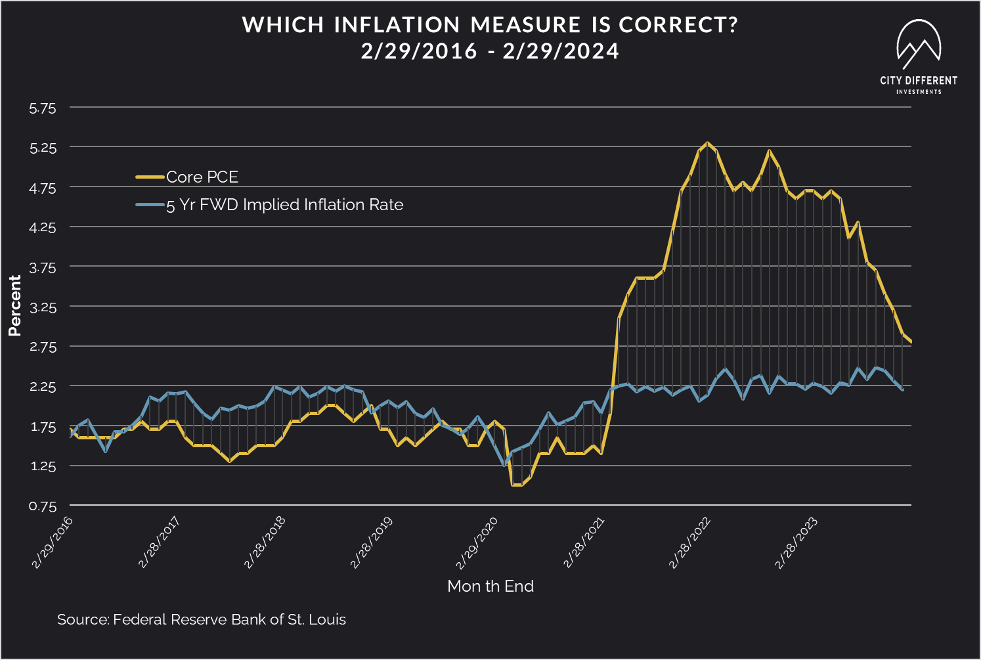

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week of March 15 at 2.25%, nine basis points lower than the March 8 close of 2.34%. The 10-year rate finished the week at 2.32%, four basis points higher than the close of March 8 at 2.28%.

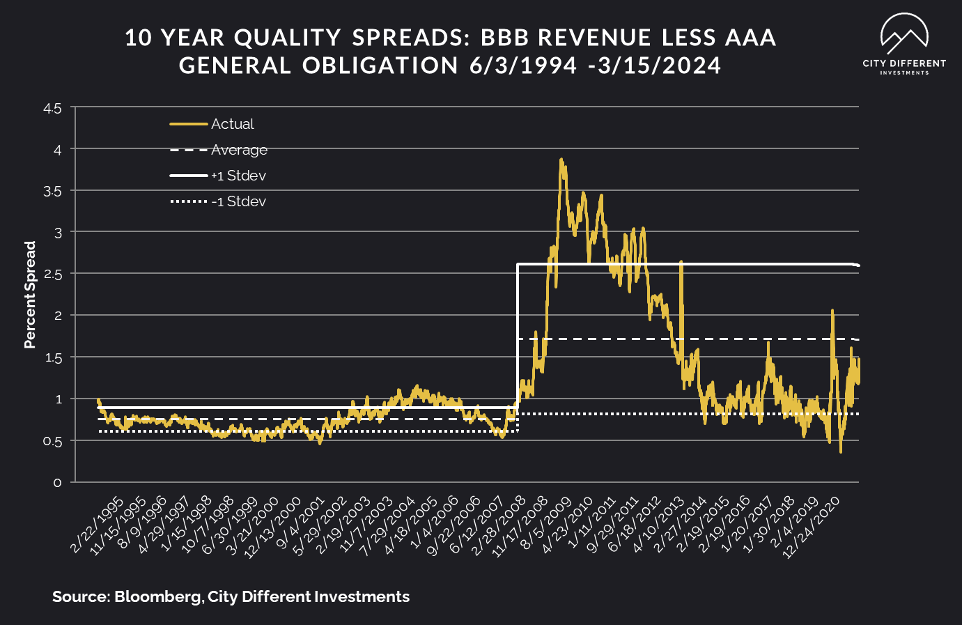

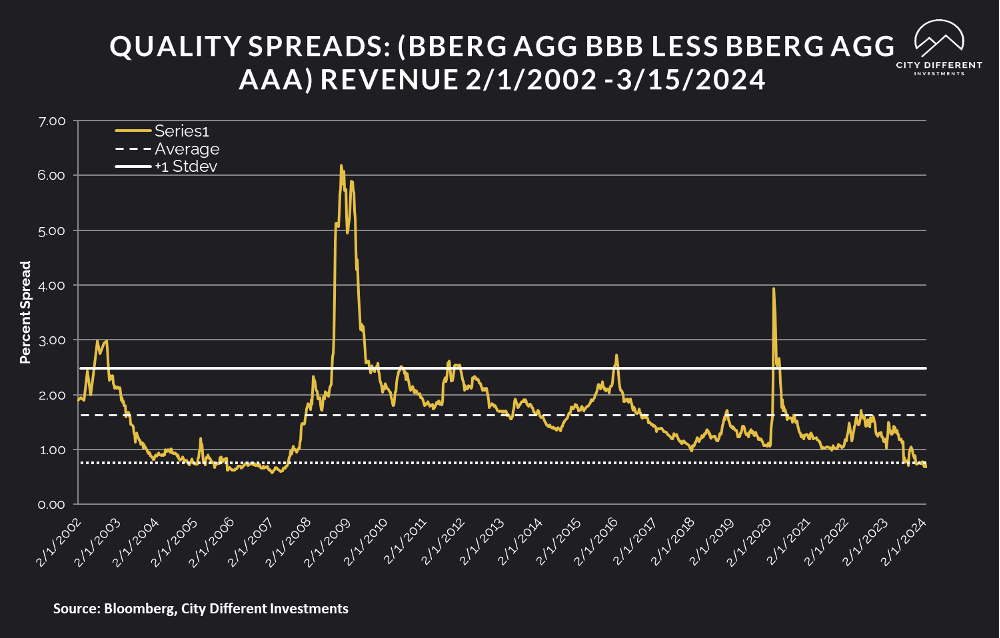

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of March 15 were 1.20%, one basis point wider than the March 8 reading of 1.19% (based on our calculations). The long-term average is 1.71%.

At 0.69%, quality spreads in the taxable market last week were one basis points tighter than the week before. High-yield quality spreads on March 15 were at 2.64% versus 2.93% last week.

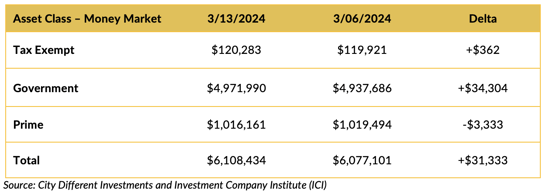

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds saw higher flows in both tax-exempt and government categories, while prime saw a slight drop.

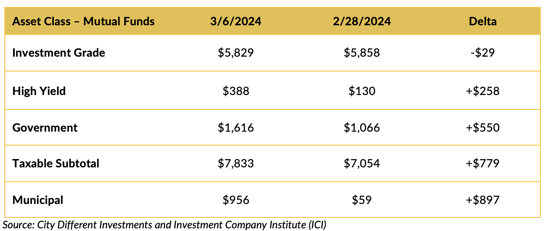

Mutual Fund Flows (millions of dollars)

The municipal market received a big inflow last week.

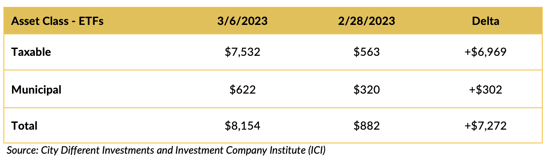

ETF Fund Flows (millions of dollars)

ETFs saw a big uptick in weekly issuance across all categories.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Year-to-date municipal supply has been robust. But so has demand, with close to $21 billion worth of coupon reinvestment coming up in March/April. This week’s municipal tax-exempt supply is projected to be close to $6.3 billion.

CONCLUSION

This is an important week. The Fed is not expected to raise rates. They are, however, expected to provide guidance for its dot plot and quantitative tightening after last week’s hotter-than-expected inflation prints for both CPI and PPI data.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.