.png)

WEEK ENDING 7/7/2023

Highlights of the week:

- We celebrated the 4th of July last week, but the real fireworks were on the 6th.

- Money funds are seeing all the love.

- Members in the House are fighting again and using very bad language. Is it time for a soap sandwich?

A CITY DIFFERENT TAKE

It started out as a quiet two weeks, with Treasury yields drifting upward. Core PCE came in lower than expected on June 30 at 4.6% (versus 4.7%). A higher ADP employment report on July 6 sent yields in the bond market higher and stock prices lower (S&P 500 down about 1%, and the ten-year Treasury crested 4%). The real jobs report was released Friday (July 7) and showed a 209,000 gain in nonfarm payrolls (lower than the expected 230,000).

Year-over-year average hourly earnings were reported at 4.4%, and the prior month’s number was revised from 4.3% to 4.4%. None of this led to a rollback of Thursday’s action.

Labor negotiations are getting more heated. There is a writer's strike in Los Angeles while the Screen Actors Guild looks to strike this week. The Teamsters Union is threatening to walk out of UPS. Finally, contract negotiations with auto workers will begin soon. We are sure the high summer temperatures will only help bring a sense of calm to these tense discussions.

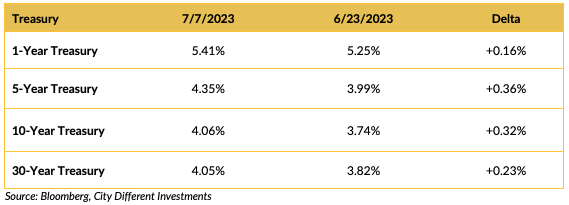

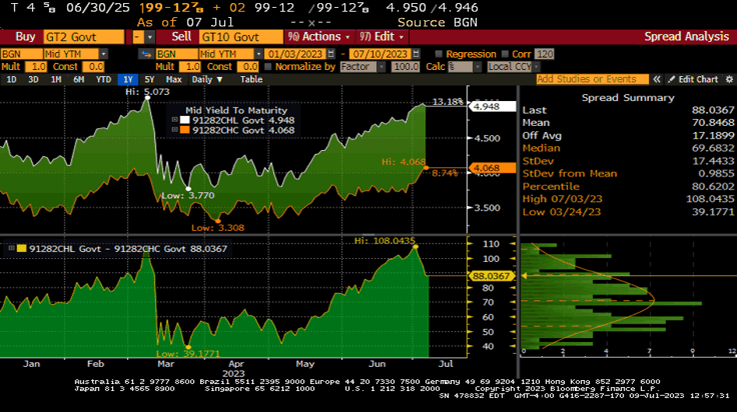

CHANGES IN RATES

Rates moved higher across the yield curve over the last two weeks. The inversion of the Treasury yield curve decreased dramatically over the same period. This analysis of the two-year Treasury note versus the ten-year Treasury bond highlights this move.

Source: Bloomberg

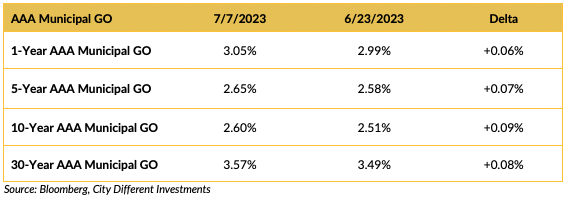

Yields moved higher across the municipal market over the last two weeks but at a much lower level than the Treasury market.

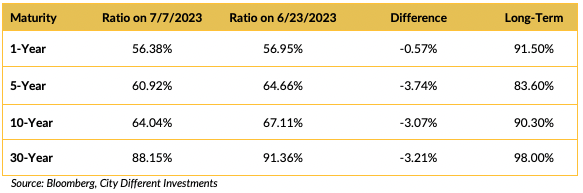

Muni/Treasury ratios are lower across the curve. Municipals continue to richen relative to Treasuries.

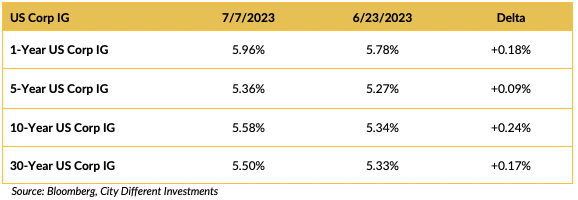

Yield in the investment grade (IG) corporate market increased over the last two weeks.

Yield in the investment grade (IG) corporate market increased over the last two weeks.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

It appears there is continued turmoil in the ranks of the House Freedom Caucus. Fox 5 reported, “Marjorie Taylor Greene voted out of Freedom Caucus after clash with Lauren Boebert.” Now this is a cage match we would pay to see.

“The vote took place just days after Greene clashed with fellow Republican and Freedom Caucus member Lauren Boebert on the House floor. During that argument, Greene reportedly called Boebert a "little b----."

More recent reports indicate that cracks have emerged and that the Freedom Caucus “is grappling with what they stand for and how best to wield their potential power” or whether it should even support Trump for a 2024 presidential run. It will be interesting to see whether Republicans will be able to unify or whether a splintered party will result in more gridlock or additional power for Democrats. Time will tell.

Treasury Secretary Janet Yellen is in China, trying to find common ground. President Biden is off to a NATO summit where he will have to explain why the U.S. is sending cluster ordinance to Ukraine. (Answer: we and our allies don’t have anything left.)

The Supreme Court is on summer recess. We wonder where Justices Thomas and Alito will be vacationing.

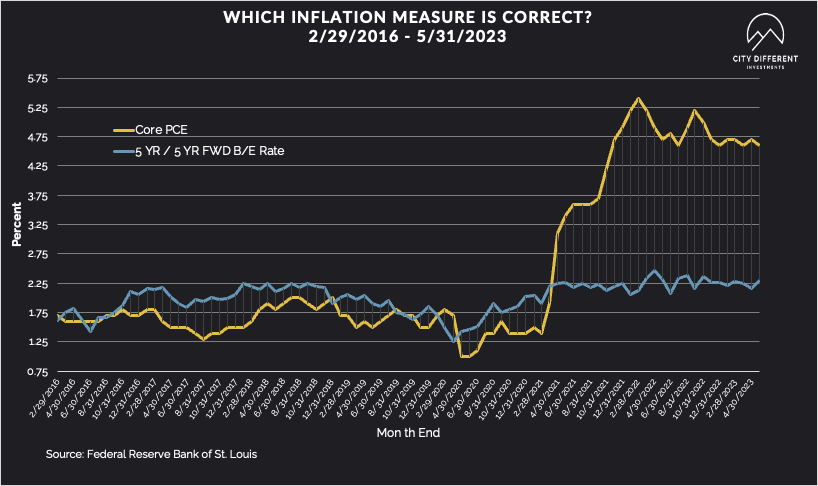

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.32%, a six-basis-point increase over the June 23 close of 2.26%. The 10-year Breakeven Inflation Rate finished the week at 2.27%, a six-basis-point increase over the June 23 close of 2.21%.

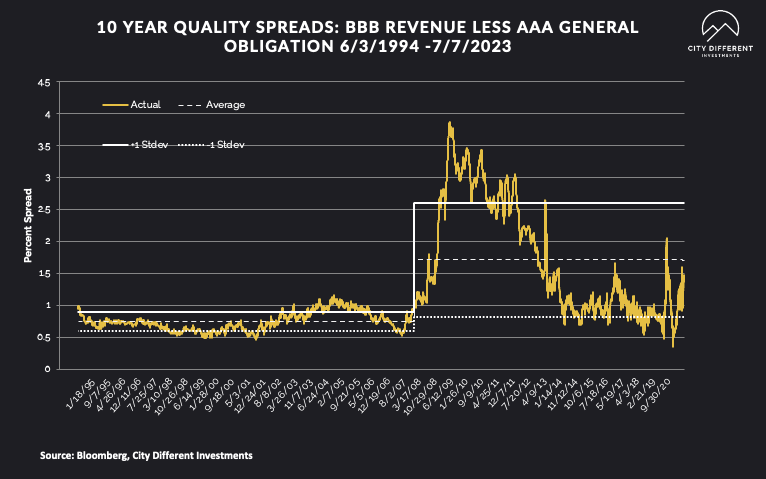

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of July 7 was 1.39% (based on our calculations), 0.02% higher than the June 23 close of 1.37%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

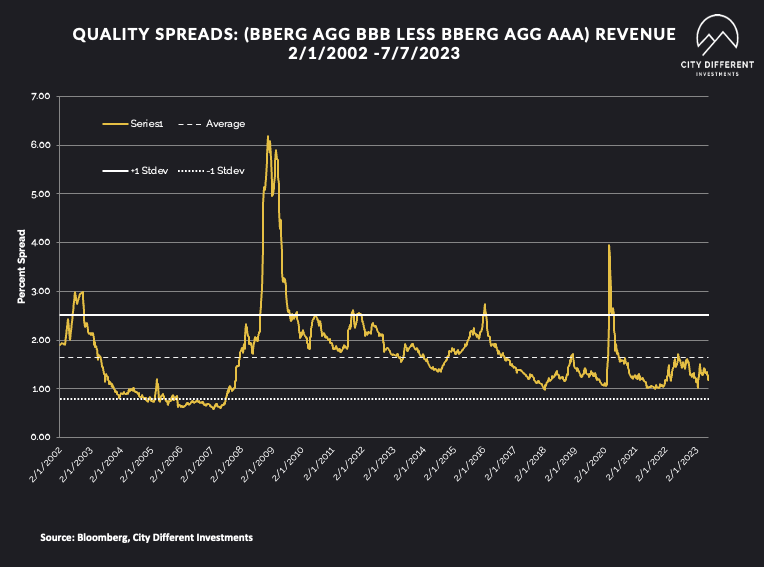

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 1.18%.

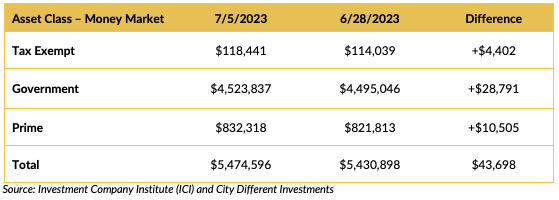

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds saw positive cash flows. Disintermediation continues; high money market yields are pulling cash out of bank deposits. Is this the correct strategy for long-term investors? Read our upcoming blog, “Avoiding the Cash Trap” and decide for yourself.

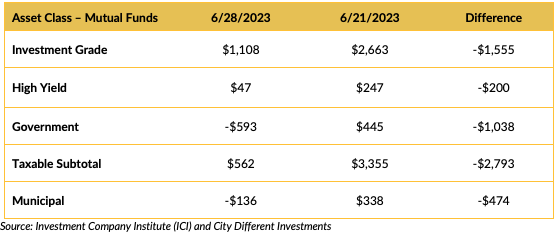

Mutual Fund Flows (millions of dollars)

Flows into bond funds are weak.

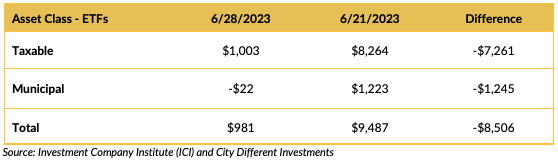

ETF Fund Flows (millions of dollars)

Bond ETFs also saw weak cash flows.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply is starting to build, with reports slated somewhere around $9.8 billion.

CONCLUSION

The bond market has adjusted to levels not seen since March’s Silicon Valley Bank collapse. The Fed seems poised to increase rates at their July meeting by 25 basis points. The reported market probability of such a rise is 89%. The yields on money market funds are attractive, but how long will that last? Overall, we feel this is a good time for long-term investors to think about bonds.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.