.png)

WEEK ENDING 6/2/2023

Highlights of the week:

- We hope everyone had a great Memorial Day weekend.

- Yay! The United States did not default on its debt. But we had to endure an ugly kabuki dance to get there.

- A heck of a lot more jobs were created in May than the market expected.

- The Fed’s next decision just got harder.

A CITY DIFFERENT TAKE

What a week it was. The sausage-making in Washington is something to behold.

On Thursday night, the Senate passed the debt limit bill after voting on ten amendments that never stood a chance of passage. We don’t remember this type of action being covered in Schoolhouse Rock’s “I’m Just a Bill.” (If this is before your time, look it up.)

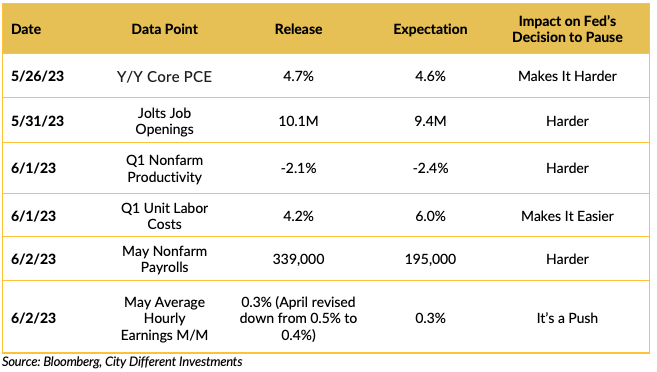

Now the markets can look to analyzing the economic data and speculating on what the Fed will do at their next meeting: hike or pause. The recent economic data has made that decision more difficult.

We think that speculating on the Fed’s next move is an interesting parlor game, but no way to manage money. Better to focus on relative value fundamentals.

We think that speculating on the Fed’s next move is an interesting parlor game, but no way to manage money. Better to focus on relative value fundamentals.

CHANGES IN RATES

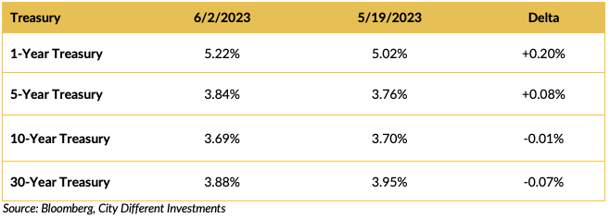

Yields in the Treasury market were mixed over the last two weeks. Short rates increased, and long rates were flat to a little lower.

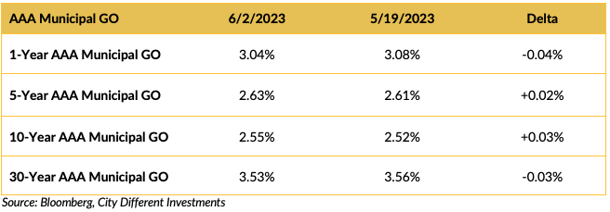

Yields in the municipal market were, for all intents and purposes, unchanged on the week.

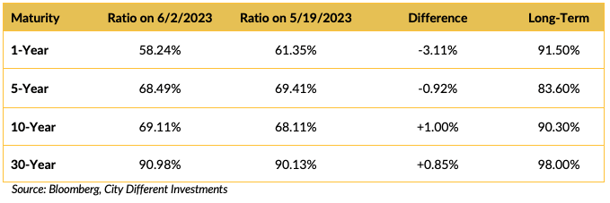

The Muni/Treasury ratios moved marginally lower on the week. AAA general obligation municipal bonds in maturities greater than 5 years make sense for anyone in the 33% marginal tax bracket or higher.

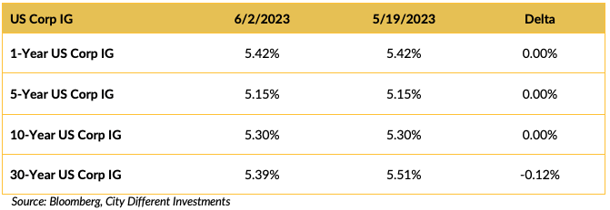

Yield in the investment grade (IG) corporate market short maturities were essentially unchanged over the past two weeks. Long-term IG yields moved lower.

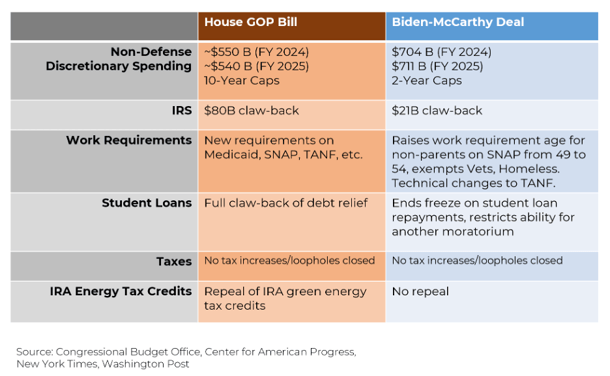

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

A PBS report states 62% of Americans say that the question of Joe Biden’s mental fitness is a real concern.

Well, now that the debt deal is behind us, it’s safe to say we would not want to play poker with the man behind the aviator sunglasses. We would rather play against Maverick. (James Garner’s or Mel Gibson’s “Bret Maverick.” Not Tom Cruise.) A well-worn saying in poker circles is that if you don’t know who the pigeon at the table is, it’s you. We wonder if Kevin McCarthy has realized who the pigeon at his table was.

Economic analyst Steven Rattner provided a good analysis of the debt deal:

The compromise passed the House by a vote of 314 to 117. It must be a good deal because the extremes of each party are upset. The Senate passed the debt legislation 63 to 36. (What were those 36 senators thinking about? Certainly not the good of the country.) Now the markets can go about the business of worrying about the Fed, employment, GDP growth, and inflation. The debt ceiling imbroglio should be forgotten for about two years.

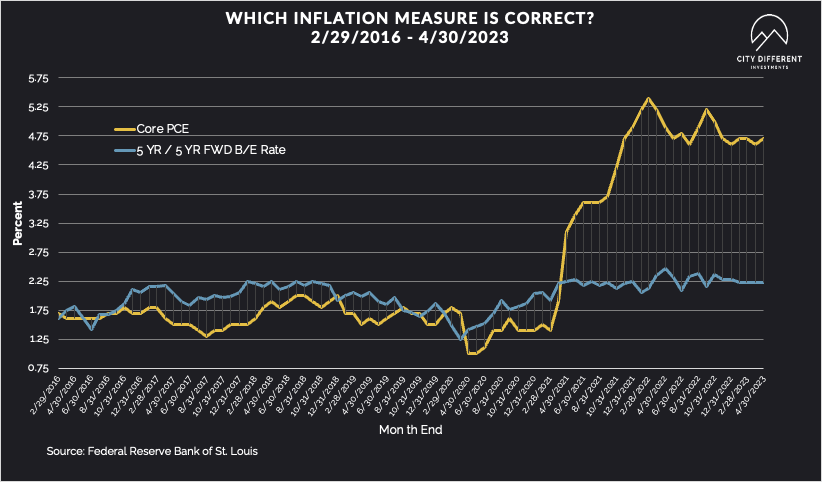

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate was 2.29% on May 19 and ended last week at 2.23%. The 10-year Breakeven Inflation Rate on May 19 was 2.24% and ended last week at 2.18%.

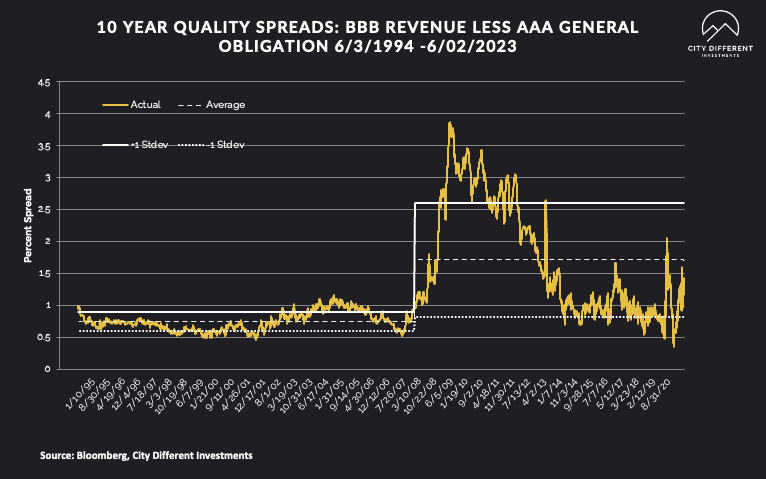

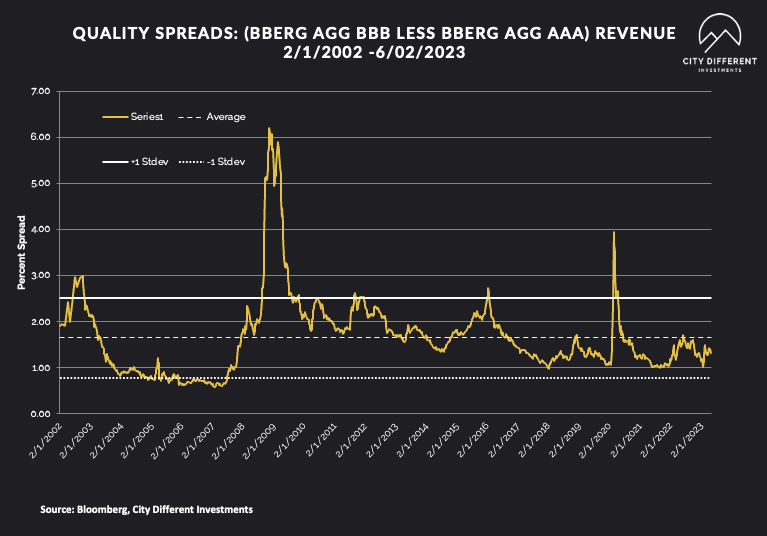

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of June 2 at 1.44% (based on our calculations), 0.28% higher than the week of May 19’s reading of 1.16%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

Quality spreads in the taxable market are not attractive but were stable last week, ending at 1.32%.

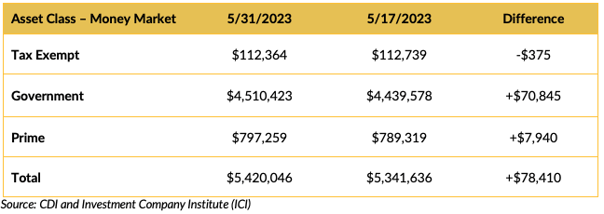

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds saw positive cash flows. Disintermediation continues; high money market yields are pulling cash out of bank deposits.

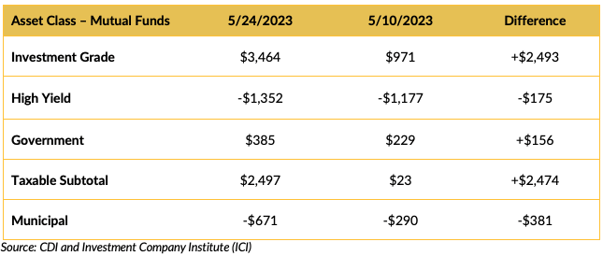

Mutual Fund Flows (millions of dollars)

Flows into bond funds are weak. Investment grade bond funds were the weekly winner. Municipal bond funds continue to see withdrawals.

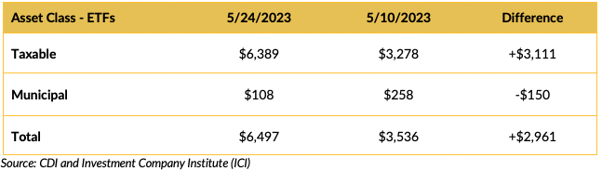

ETF Fund Flows (millions of dollars)

ETFs saw positive cash flows.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply is starting to build, slated somewhere around $9.2 billion.

CONCLUSION

The United States did not default on its debt, but the road to get there was rough. Seems like the debt deal angered the extreme segments of each political party. In the final analysis, that must mean it’s a good deal (such is the nature of compromise). Maybe there is hope for our democracy after all. Well, let's not get ahead of ourselves.

The economy certainly seems resilient, at least for this week. Inflation looks sticky. The Fed’s job has gotten harder. Let's hope they do a better job than Congress.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.