Vanguard just dropped the hammer on ETF fees again, slashing its average expense ratio to a jaw-dropping 0.07%. That’s a big deal in an industry segment where “fees are one of the most important differentiating factors,” as TMX VettaFi’s Roxanna Islam put it.

On the surface, this looks like a win for investors — according to Vanguard’s estimates, investors stand to save ~$350 million this year alone. But if you look past the headline, the reality is more complicated.

Sure, cheap is good… but only if it doesn’t come with trade-offs. And in this case, those trade-offs could cost investors far more than a few basis points in fees.

The Passive Investing Subsidy

Vanguard gets to play by a different set of rules. Since its fund investors effectively own the company, it can afford to funnel extra revenue into lower fees. That’s great for marketing, but it forces competitors into a no-win scenario. As Bloomberg put it: “Follow suit and lose potentially hundreds of millions in revenue — or hold the line and risk losing badly needed market share.”

But here’s the thing — Wall Street isn’t in the business of simply accepting lower revenues. That money has to come from somewhere. And where it’s likely to come from is everything except passive investing.

We’re already seeing it happen. Asset managers are shifting their focus to “higher-margin areas” like active strategies, alternatives, and niche ETFs. In fact, Bloomberg went on to say that the average fee on newly launched ETFs in 2024 has actually ticked up — probably as a result of firms moving toward more expensive products to make up for lost revenue.

As CFRA’s Aniket Ullal put it, firms like JPMorgan probably won’t even try to compete with Vanguard on low-cost, index-based funds. Instead, they’re putting their efforts into “higher margin areas” like active investing and alternatives.

Translation: If you want exposure to anything other than a vanilla index fund, you should probably expect to pay more.

The Hidden Cost of “Cheap”

If you’re a retail investor only interested in passive investing, this does count as a win… potentially.

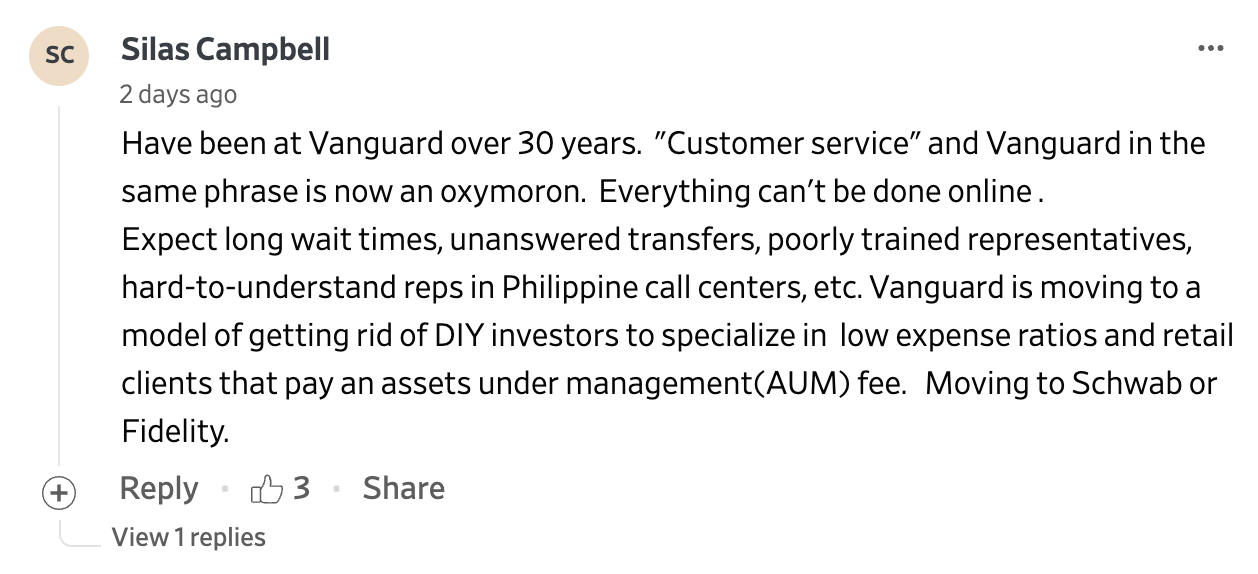

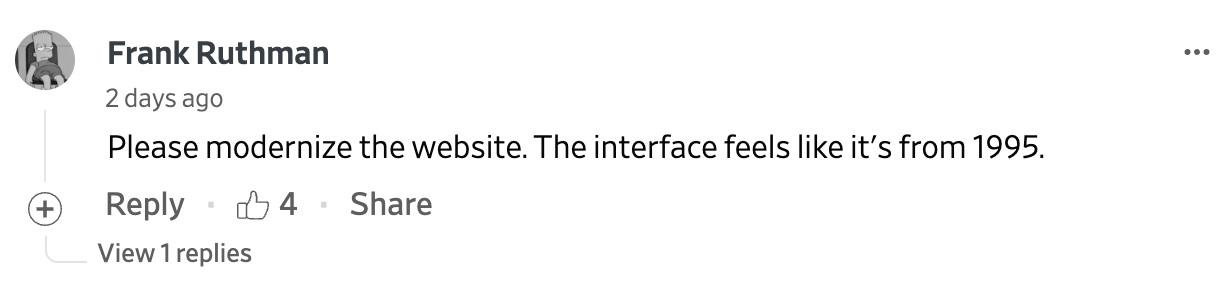

One look at the comments section on the Wall Street Journal’s article paints a different picture for Vanguard clients:

Their now-legendary challenges with customer service got the A1 treatment from the WSJ in a separate article, too:

If you’re a set-it-and-forget-it passive investor, maybe you don’t care about this. But if you place any value on customer service, personal relationships, helpful guidance, or just, ya know, the ability to talk to someone about a question or concern you may have… this announcement doesn’t exactly spell good news.

If Vanguard is knowingly and willingly deflating its bottom line by $350MM… what makes us think they’re going to invest real money into customer service or modernizing their digital platforms?

What This Means for Investors

If all you care about is rock-bottom fees, then yes, Vanguard’s move is a win. But don’t mistake cheaper for better.

Passive investing has risks — especially when markets are as concentrated as they are today.

Passive index strategies typically can’t proactively protect you against macro-market downturns (like we saw with the Deep Seek announcement last week… when markets are concentrated and volatility hits the big boys… a lot of indexes dip).

And as we’ve pointed out before, there’s substantial (and in our opinion, compelling) research showing the less actively a fund is managed, the lower its average returns.

Cutting fees on passive ETFs won’t change those realities.

Meanwhile, if you’re looking for real diversification — or just an investment strategy that doesn’t blindly track the same indexed companies — you should likely expect to pay a premium. Because when Vanguard pushes ETF fees to zero, the cost of everything else likely has to go up.

IMPORTANT DISCLOSURES

The information contained in this communication has been designed for general informational, illustrative, and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any security. Moreover, the information provided is not intended to provide any investment advice whatsoever. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, or any non-investment related content, made reference to directly or indirectly in this communication will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. No discussion or information contained herein serves as the provision of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability above to his/her individual situation of any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal, tax, or accounting advice.

The presented information and statistics have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or forecasts discussed herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice. Please keep in mind that past performance may not be indicative of future results.