Bond investors have grown more sophisticated over the years, and the tools we use to evaluate bonds have evolved alongside us.

For decades, yield was the primary measure investors focused on. Yield tells you the income a bond generates relative to its price. It remains one of the most important metrics in fixed income, but yield only tells part of the story.

.png?width=793&height=248&name=bonds%20yardstick%20(2).png)

In 1973, Martin Leibowitz and Sidney Homer published Inside the Yield Book, helping bring duration into the mainstream. If yield tells investors what a bond pays, duration tells them how a bond's price is likely to react when interest rates change. It gave investors a second dimension for understanding risk.

As the bond market became more complex, duration alone was no longer enough. Callable bonds introduced a new challenge. If an issuer can redeem a bond early when rates fall, the bond's future cash flows change. Option-adjusted duration emerged to account for those embedded options and provide a more accurate measure of interest-rate sensitivity.

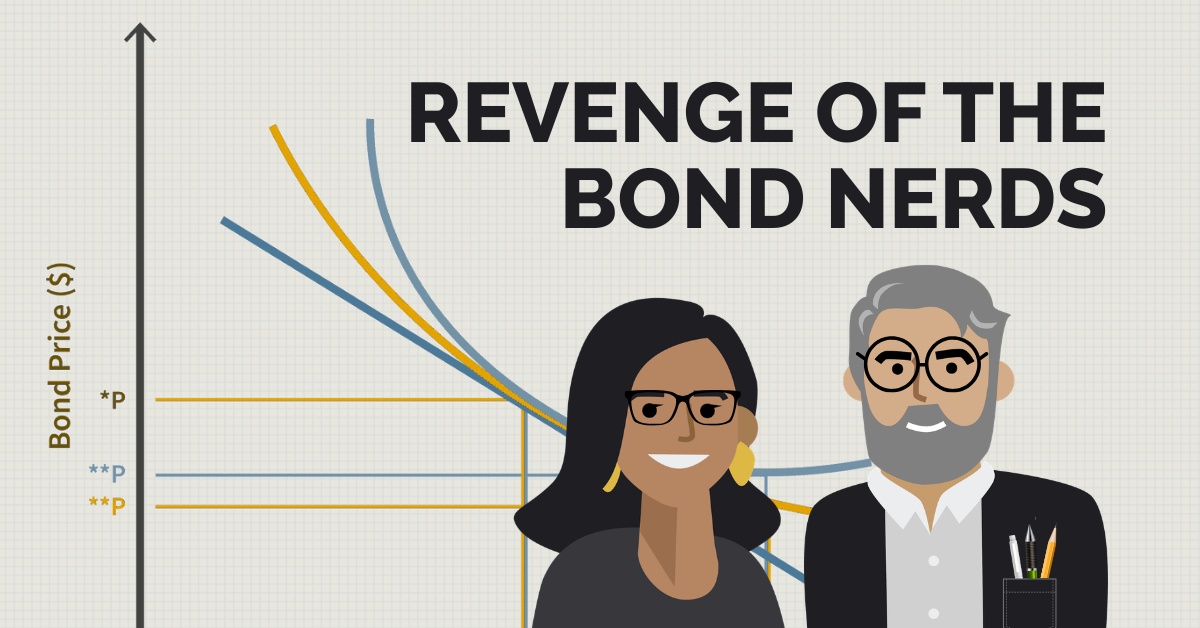

That brings us to convexity.

Convexity measures how a bond's duration changes as interest rates move. While duration assumes a relatively straight-line relationship between bond prices and interest rates, convexity recognizes that the relationship is actually curved.

Positive convexity is generally beneficial for investors in a volatile interest rate environment. As interest rates rise the duration of a postively convex security decreases. The opposite also holds true as interest rates decline the duration of the positively convex security increases.

Negative convexity does the opposite, and it is commonly found in callable structures. When rates fall, the duration of a negatively convex security decreases. The upside will be limited because the issuer may call the bond and refinance at a lower rate. When rates rise, the bond's duration can extend, increasing interest-rate risk at exactly the wrong time.

At City Different Investments, convexity is an important part of our fixed income analysis because we strive to provide clients with stable income streams while minimizing unexpected price dislocations. Convexity helps us understand not just how a portfolio may perform today, but how it may behave when market conditions change.

Which is why this Bloomberg headline caught my eye: "Muni Convexity Deepens as Defensive Structures Favor Stability."

The article notes that the investment-grade municipal bond index is near a multi-year low in option-adjusted convexity, driven by a growing concentration of premium, high-coupon callable bonds. Those structures can provide attractive income and price stability, but they may also limit participation if rates fall and create duration extension risk if rates rise.

In other words, the headline highlights exactly why convexity matters.

A portfolio heavily concentrated in premium callable bonds may appear attractive because of its yield profile. But if the embedded call options are already in the money for the issuer, investors face a challenging tradeoff. If rates fall, the bonds may be called away. If rates rise, the bonds may extend in duration and become more sensitive to further rate increases.

Both outcomes work against the investor, so why do these securities continue to show up in portfolios? Probably because they often look cheap.

Much like a value trap in the equity market, negatively convex bonds can appear attractive based on traditional valuation measures. The yield may look compelling relative to comparable alternatives. But the higher yield often exists because investors are being compensated for risks that may not become apparent until volatility returns.

These securities generally perform best in stable, low-volatility environments. When volatility increases, the embedded options that benefit the issuer can become increasingly costly for the investor.

That is the part of the story the quote screen doesn't tell.

Yield matters. Duration matters. But understanding convexity may tell you far more about how a bond portfolio is likely to behave when markets become unpredictable.

So, I'll leave you with a question, as I go change my pocket protector:

Do you know your bond portfolio's convexity?

IMPORTANT DISCLOSURES

The information contained in this communication has been designed for general informational, illustrative, and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any security. Moreover, the information provided is not intended to provide any investment advice whatsoever. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, or any non-investment related content, made reference to directly or indirectly in this communication will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. No discussion or information contained herein serves as the provision of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability above to his/her individual situation of any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal, tax, or accounting advice.

The presented information and statistics have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or forecasts discussed herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice. Please keep in mind that past performance may not be indicative of future results.