.png)

“We can and we must reduce Russian LNG exports to phase them out completely.”

-- EU Energy Commissioner Kadri Simson

[Golar’s Hilli Episeyo]

Overview

Golar LNG (Nasdaq: GLNG $23/share) is a Norwegian energy infrastructure group whose main assets are two Floating Liquefied Natural Gas (FLNG) facilities, called Hilli (in service since 2017) and Gimi (recently constructed). We introduced Golar LNG here back in March 2022 (when GLNG was priced at $18), and the company is now entering an interesting phase of developments which could enhance its valuation. Most immediately, Golar’s Gimi vessel should depart its Singapore shipyard this month to begin a 20-year service contract for the UK’s BP.

Why LNG

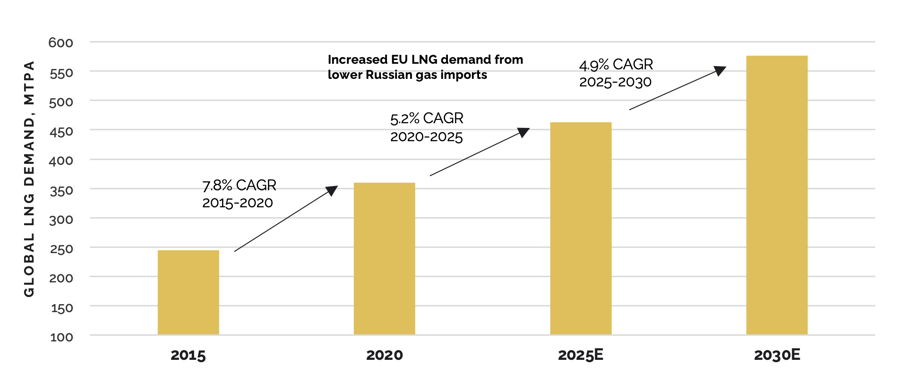

According to the latest estimates from Bernstein, global LNG demand should grow 5% per annum between now and 2030. This is driven by demand from Asia and Europe, which is eager to reduce its dependence on piped Russian gas because of the Ukraine war.

Interestingly, Europe imported 40% more LNG from Russia from January to July this year versus the same period in 2021, before the war began. But as the EU Energy Commissioner said last month: "We can and we must reduce Russian LNG exports to phase them out completely."1 This would raise demand for gas from other sources, including the offshore LNG in which Golar specializes. Golar’s FLNG vessels facilitate the offshore production, liquefaction, and storage of natural gas for transport to customers worldwide. LNG is a relatively clean energy source, and FLNG vessels produce zero hydrocarbon gas flaring. In other words, Golar’s vessels enable Europe to reduce its Russian reliance and transition towards a lower-carbon footprint while allowing energy producers to access remote gas reserves.

A Sea of Opportunities

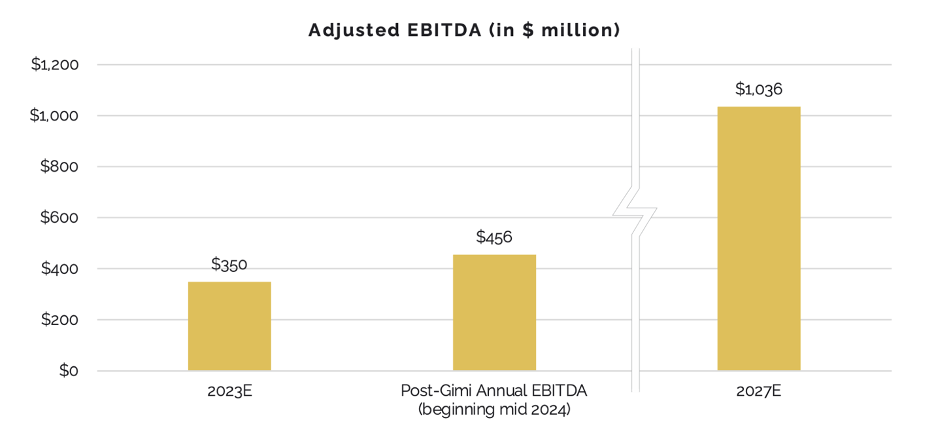

Golar’s 2023 profitability of about $350M of EBITDA looks like a pebble next to its $1 billion potential, according to the CEO’s recent outlook statement:

Tariffs in line with the current competitive U.S. export market suggest earnings of about $1 billion from this available capacity. However, our FLNG technology enables monetization of stranded gas reserves that would otherwise remain undeveloped. Hence, we believe significantly higher liquefaction margins should be obtainable. (Source: Q2 2023 earnings transcript)

So how could Golar, with a market capitalization today of about $2.5bn, achieve profits of $1bn or more? There are several steps that the company is taking to grow profits in the near term:

- Delivering the Gimi vessel to its customer this month, beginning a 20-year service period with contractually fixed revenues and profits. Gimi has a nameplate capacity of 2.7 mtpa (million tons per annum).

- Refinancing of Gimi once the vessel is in service. This should unlock capital and afford the asset a lower cost of debt.

- Recontracting of Hilli, which is currently only 58% utilized versus its nameplate capacity of 2.4mtpa. Management believes higher utilization and perhaps a higher tariff is achievable.

- Similarly to Gimi, Hilli can be refinanced once a new long-term contract is in place.

- An additional “Mark II” 3.5mtpa FLNG vessel. Management is in advanced deployment discussions, and Mark II could be ordered by the end of 2023 for delivery by late 2026. This would represent a substantial addition to Golar’s total liquefaction capacity.

[Golar’s Gimi, ready for departure from the Singapore shipyard]

[Golar’s Gimi, ready for departure from the Singapore shipyard]

Quantifying the Outlook

Based on the latest estimates, Golar could generate approximately $350M in EBITDA in 2023. Then Gimi could contribute $151M in EBITDA for Golar beginning mid-year of 2024. Recontracting Hilli at 90% capacity vs. 58% today could add approximately $168M in EBITDA. Lastly, Mark II could produce $412M in EBITDA based on currently planned capacity. Adding all these components, we estimate Golar could generate ~$1bn in EBITDA by 2027 or so, or 200% more than this year’s projected EBITDA.

Valuation

Golar shares have risen only modestly this year and have trailed the overall market. Golar’s recent share price of $23 equates to a dividend yield of 4.3% and an enterprise value (EV) of ~$2.7B (market cap of $2.5B plus net debt of $0.2B (including marketable securities). As discussed above, based on current market conditions, Golar should generate an annual adjusted EBITDA of ~$456m when Gimi’s EBITDA kicks in around mid-20242. Hence, Golar is priced at ~5.9x EV/EBITDA when Gimi starts running at a steady state. Other LNG infrastructure companies are valued more highly: Cheniere LNG trades at 10x 2024E EV/EBITDA, and we recall Teekay LNG being purchased by private equity in late 2021 for 11x EBITDA3.

Risks and Conclusion

There are always things to worry about. In the case of Golar, there are geopolitical risks, energy price fluctuations, and unforeseen project delays to consider. However, the delivery of the Gimi vessel represents meaningful progress, and Golar appears to be charting a promising course.

2. While Gimi is expected to generate cash flow beginning in early 2024, this will initially bypass the income statement per GAAP accounting. Then Gimi should produce $151M in EBITDA p.a. for Golar for 20 years beginning mid-2024.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice. Forecasts are based on current conditions, subject to change, and may not come to pass.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. Do not assume any securities identified were or will be profitable. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities and should not be relied on as financial advice. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.