.png)

WEEK ENDING 10/31/2025

- Fed eases short-term rates by 0.25%

- Chair Powell threatens “last call”

- Dissension on the FMOC

- Next Fed chair: and then there were five

- Government shutdown continues

A CITY DIFFERENT TAKE

Last Wednesday, the Federal Reserve board lowered short-term interest rates by 0.25%. The market’s implied probabilities for such a move were very high. The following table highlights those probabilities for the Friday before the Fed meeting and the Friday after the Fed meeting.

In terms of fresh data, the Fed is flying blind.

“But the central bank's new policy statement included several references to the lack of official data during a federal government shutdown, and Powell told reporters later that policymakers are likely to become more cautious if it deprives them of further job and inflation reports.” Flying Blind

This meeting seemed to be more contentious than others.

“Powell said there were ‘strongly differing views’ among his Fed colleagues about the appropriate path for monetary policy moving forward, with ‘a growing chorus now ... feeling like maybe this is where we should at least wait a cycle’ before cutting rates again. The latest rate cut drew dissents from two policymakers, with Fed Governor Stephen Miran again calling for a deeper reduction in borrowing costs and Kansas City Fed President Jeffrey Schmid favoring no cut at all given ongoing inflation.” Flying Blind.

Chair Powell threw some cold water on the idea of a December rate cut,

“‘In the committee’s discussions at this meeting, there were strongly differing views about how to proceed in December,’ Powell said. ‘A further reduction in the policy rate at the December meeting is not a foregone conclusion. Far from it.’” Here comes the cold water

The change in implied probabilities shows the effect of the chair’s comments on market expectations. Recent company layoff announcements are also concerning to the Fed.

“‘You see a significant number of companies either announcing that they are not going to be doing much hiring or actually doing layoffs, and much of the time they’re talking about AI and what it can do,’ Powell said. ‘We’re watching that very carefully.’

“Earlier this week, Amazon announced it would slash 14,000 jobs across its business, while media giant Paramount on Wednesday laid off at least 1,000 workers across its various divisions, including CBS News. UPS also revealed Tuesday that it would terminate 48,000 employees this year. Last week, Target said it would eliminate 1,800 corporate jobs, its first major layoffs in a decade.” More cold water

A chorus of descension?

“Dallas Fed President Lorie Logan and her Cleveland counterpart, Beth Hammack, said Friday they would have preferred to hold rates steady. Both were speaking at a conference in Dallas, following a statement earlier in the day from Kansas City Fed President Jeff Schmid outlining the reasons for his dissent against Wednesday’s rate cut.” The debate heats up

More support for further rate cuts in December:

“Federal Reserve Governor Christopher Waller stated Friday that the central bank should cut interest rates again in December, citing weakness in the labor markets despite the lack of official economic data during the ongoing government shutdown.” This is what makes markets

And then there were five, but in the end, there can be only one!

“Treasury Secretary Scott Bessent on Monday confirmed that the list of candidates to replace Federal Reserve Chair Jerome Powell has been winnowed down to five, and President Donald Trump said the replacement is likely to be named by the end of the year.

“Speaking to reporters on Air Force One, Bessent said the finalists are current Fed Governors Christopher Waller and Michelle Bowman, National Economic Council Director Kevin Hassett, former Fed Governor Kevin Warsh, and BlackRock executive Rick Rieder, according to several media outlets.”

A client question on time periods:

One of our clients asked us why we use such long time periods in our analysis, and why we do not use a shorter period. The answer is that a long-term time series tends to even out short-term disruptions or anomalies.

Take our slope of the yield curve analysis, for example. Our analysis goes back to 1994. If we used a shorter time period, distortions like an inverted yield curve would distort the analysis. This lesson was a result of painful experience.

Let’s highlight the inverted yield curve example. First, our core belief is that a positively sloped Treasury curve is the normal state. So given that belief, an inverted yield curve is the anomaly. If we examine the slope of the curve under various time frames, we find that the inverted yield curve has a significant impact on the analysis.

The following table highlights the answers to a question we posed to Google’s AI assistant: “What percentage of time was the Treasury curve inverted since (fill in the time segment)?”

By increasing the time period, the impact of an inverted yield curve is lessened, and that leads to less trade volatility based on short-term anomalies. These results are close to the analysis we conducted on weekly data.

But how does this long-term focus change when a systematic environment change happens? All you have to do is look at our municipal credit graph for the answers. In that graph, you see two time series: one before the financial crisis, when insured municipal bonds were rated AA and were about 60% of the new issue municipal market; and the other time after the financial crisis, when insured municipal bonds all but disappeared, and most lost their AAA credit ratings. The short answer is we start anew.

CHANGES IN RATES

Treasury Market

Treasury rates moved higher on the week. Nobody likes it when the punchbowl is removed. The 2/10-year slope ended the week at 51 basis points.

Municipal Market

Yields in the municipal market moved higher last week, albeit moderately. 2/10 spreads increased by 25 basis points for the week ending Oct. 31. A dramatic shift from the +1.00% slope of Aug. 22.

Selected Municipal AAA General Obligation Bond / Selected Treasury Bonds Yield Ratio

Treasury-muni ratios were richer across the yield curve.

Investment Grade Corporates

Investment grade corporate bond yields moved higher week over week.

THIS WEEK IN WASHINGTON

Election week is upon us. New Jersey and Virginia will be electing governors, and New York City will be electing a mayor. The NYC choice is interesting. On one hand, you have an older politician with a lot of baggage. On the other hand, a young politician with new ideas that, by our way of thinking, have a low probability of success.

Let’s not forget California’s Proposition 50 special election (the effort to counter Texas’s redistricting).

These elections seem to be run-of-the-mill, unless you are a Republican worried about next year’s midterm elections. To make these special elections interesting, the president has decided to monitor:

“Late last week, Trump's Department of Justice announced it was sending election monitors to observe voting in one county in New Jersey, which features a race for governor that Trump has become deeply invested in, and to five counties in California, where Democratic Gov. Gavin Newsom is pushing a ballot measure to counter the president's own effort to rejigger the congressional map to elect more Republicans.” This Summer I hear the drumming

The government is still shut down. The House is on an extra-long vacation thanks to the speaker, and “Johnson sets record refusing to swear in Arizona Democrat, Adelita Grijalva for 36 days after she won election.” (Why) The “why” may have something to do with :

“Rep. Eric Swalwell (D-CA) claimed that multiple House Republican colleagues informed him that they’re planning a ‘jail break’ revolt of over 100 lawmakers against President Donald Trump if there’s a discharge petition to force a vote on the Jeffrey Epstein files release.” Jail Break

Thin Lizzy may have said it best:

“Tonight there's gonna be a jailbreak

Somewhere in this town

See, me and the boys, we don't like it

So we're gettin' up and goin' down.” Thin Lizzy

So rather than “goin’ down,” Speaker Johnson sent everyone home — but for how long?

Another interesting point: given the government shutdown and federal workers and military going without pay, should the House continue to be paid?

Add to this the demolition of the East Wing:

“Amid the rubble and rancor memorializing where the East Wing of the White House once stood, President Donald Trump and his team are trying to dig out. Public outrage has been piling up over the sudden demolition to make way for the sprawling, golden ballroom he has long craved. Trump says the new construction will be a monument to the country’s greatness, even as his team insists there is nothing unusual in how he is going about it.” Good bye East Wing hello Golden Ballroom

All of it sounds politically tone deaf. (Good thing Thin Lizzy still holds up.) But if you’re not worried about re-election, what the heck?

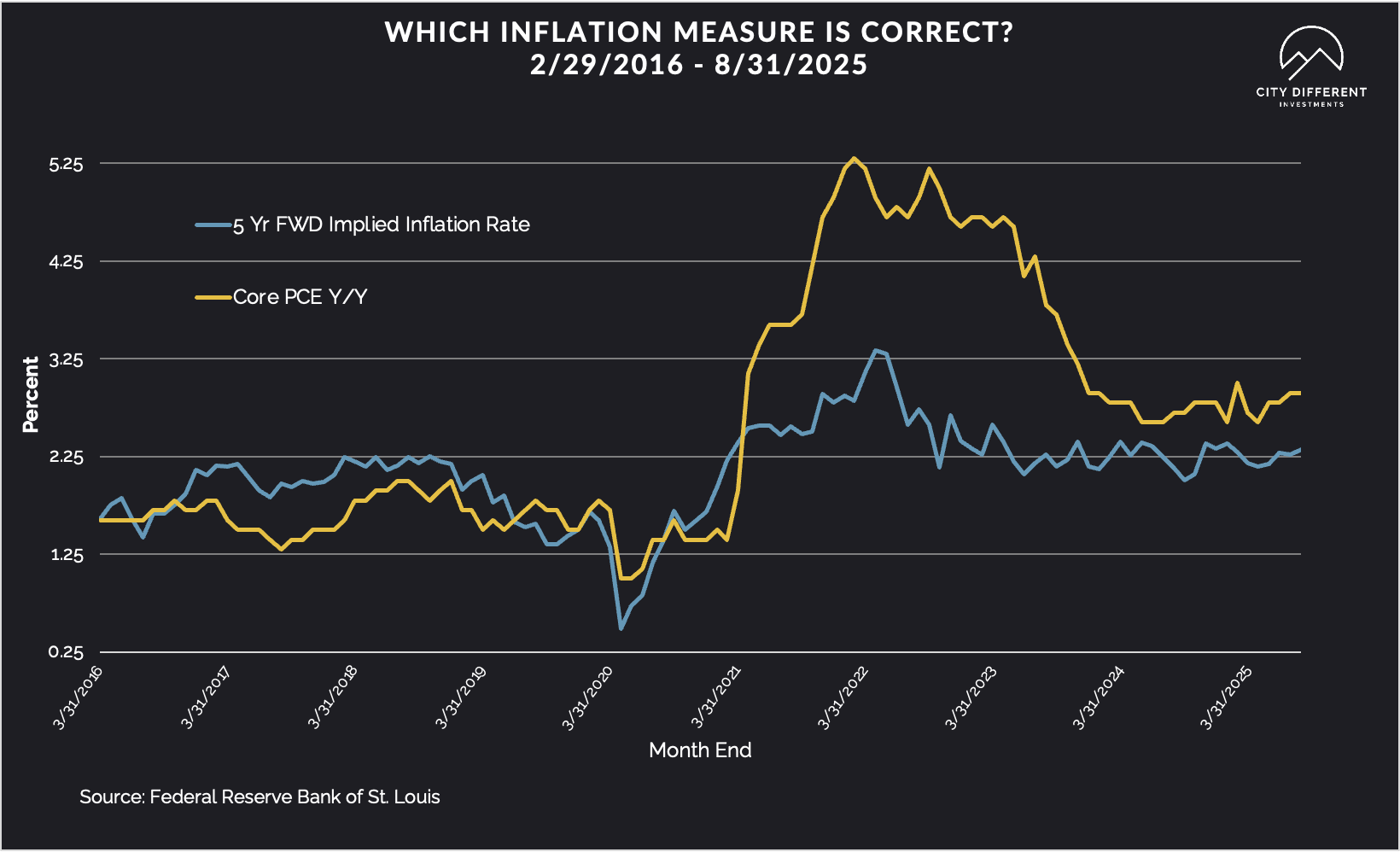

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week of Oct. 31 at 2.40%, the same as the previous week. The 10-year Breakeven Inflation Rate finished the period at 2.30%, 1 basis point higher than last week's observation. The government shutdown prevents us from updating the above graph.

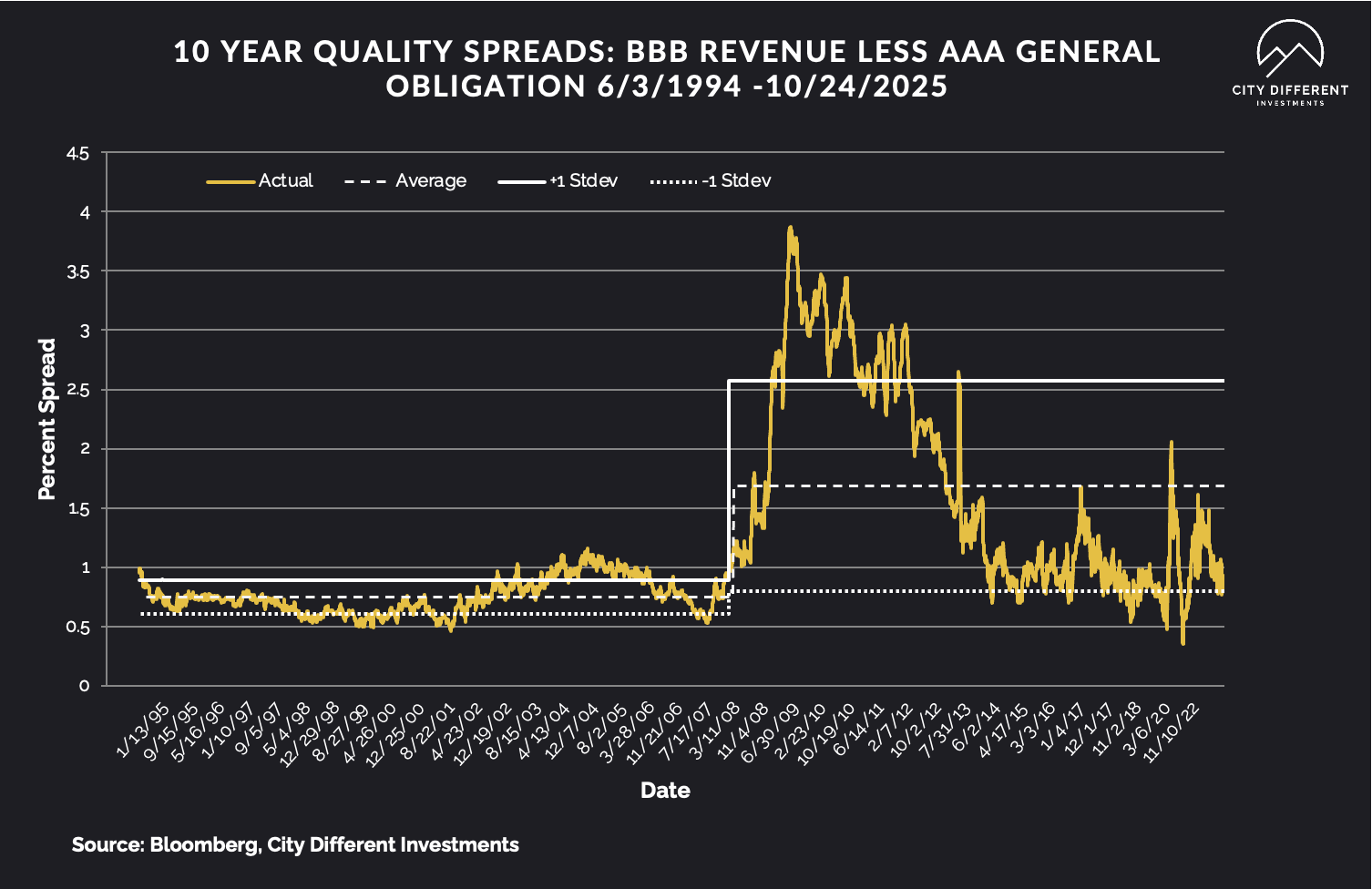

MUNICIPAL CREDIT

Last week's 10-year quality credit spread between BBB revenue and AAA general obligation bonds was at 0.92% versus a historical average of 1.68%, demonstrating very healthy and tight spread metrics.

TAXABLE CREDIT

Investment grade spreads are tight at 0.95%, 1 basis point higher than last week. This is still very tight compared to a historical average of 1.57%. The high-yield spread is lower at 2.71%, compared to a historical average of 4.57%. We believe that both these markets are overpriced on a spread basis. The latest credit tumult has not been represented in the current credit spreads.

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market fund flows were up in total last week, led by the government category.

Mutual Fund Flows (millions of dollars)

Mutual fund flows were positive from the prior week.

ETF Fund Flows (millions of dollars)

ETF flows were mixed over the week.

SUPPLY OF NEW ISSUE BONDS

Last week was a big supply week, with $13 billion issued. There are still a lot of new issuances to get through.

CONCLUSION

There’s dissension on the Fed board, and future rate cuts are not guaranteed. (Well, at least not from a market-implied probability standpoint.) Still no government data. The House is still on vacation (and getting paid). Flight delays are on the rise, just in time for the Thanksgiving holiday. (Now, there’s some pressure for the government.) Since this is Halloween weekend, it looks like the Fed gave out raisins, not chocolate bars (who can afford them?) and Chair Powell looks to be previewing this idea of “coal for Christmas.”

Have a nice week and be careful out there.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein is available upon request.