.png)

WEEK ENDING 2/16/2024

- Inflation does not move in a straight line.

- There is still a lot of cash sloshing around the system.

- Congress takes two-week vacation with foreign aid on their desks and potential shutdown on the horizon.

A CITY DIFFERENT TAKE

Valentine’s Day was this week, but many market participants had their hearts broken on Tuesday with the release of the January CPI report.

The report came in hotter on almost all vectors, showing investors that hopes for early rate cuts by the Fed were misplaced. M/M Core CPI was reported at 0.4% while expectations were for a 0.3% reading. Y/Y Core CPI was 3.9% versus expectations of 3.7%.

Thursday’s retail sales report gave the markets some hope with a lower than expected -0.8% reading (expectations were for -0.2%).

Friday’s PPI report seemed to confirm for investors that inflation does not move in a straight line. Y/Y Core PPI came in at 2.0% versus expectations of 1.6%.

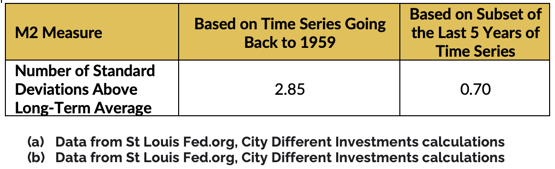

We have long wondered why the U.S. economy is so resilient. The great refinancing cycle that took place through the pandemic era of low interest rates is one driver. Another is that the Fed engineered an increase in money supply in the system (measured by M2), adding to the resiliency. The following table shows a couple of measures of money supply in the system:

This table illustrates that there is a lot of money in the system. In a normal time series, 67% of the observations are typically within +/- 1 standard deviation of the long-term average. Based on the time series going back to 1959, a 2.85 standard deviation event is quite rare. So, let’s shorten the time series to the last five years. The table shows that the M2 reading on December 1 is 0.70 standard deviation higher than the five-year average. It’s not as rare an event, but it still illustrates that there is a lot of cash in the system.

Here are a couple of more fun facts. M2 monthly growth has been negative since November 2022, on average about -2.8%. That monthly decline has been diminishing at lower rates since a peak -4.43% in April 2023 to -1.68% in December 2023. Velocity, the degree that this money is used, has been increasing since a low of 1.128 in April 2020. (The last available reading from October was 1.344.) Both an increase in M2 and velocity of M2 are needed for increased inflation.

Our summary of the week’s events are as follows:

- One month does not a trend make.

- The combination of higher inflation and a slowing economy is not a good one. Some pundits are beginning to use the term “stagflation.” We discount that because as we all know fear sells in the race for eyeballs and clicks.

- The U.S. economy does not seem to be as sensitive to higher short-term interest rates as it has been in the past — a pandemic hangover perhaps.

CHANGES IN RATES

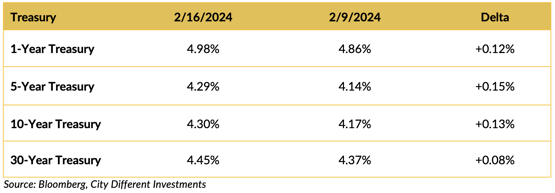

Rates moved higher in the Treasury market after some disappointing inflation news.

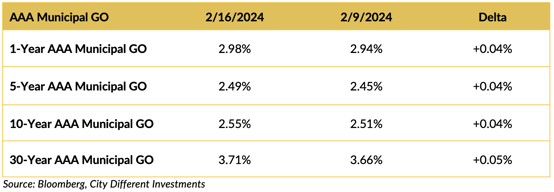

Municipal market yields moved higher, but not to the same extent as the move in the Treasury market. The President’s Day holiday shortened week ahead with limited supply is a factor driving this outperformance.

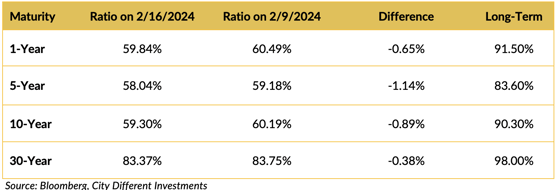

The municipal/Treasury ratios decreased marginally during the week. They are still past breakeven rates compared to their Treasury equivalents.

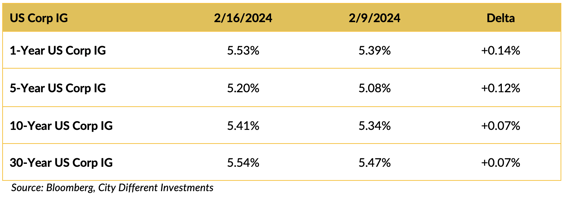

Rates in the corporate market segment were higher on the week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

What a week. Over the weekend, the death of Russian dissident Alexei Navalny was announced, drawing condemnation from many world leaders. President Biden strongly laid the fault at the feet of Putin. The presumptive Republican candidate has been strangely silent. Guess you might not want to insult any potential lenders when you may have to finance $500+ million in court verdicts.

The 113th Congress has been reported to be the next-to-least productive in modern history, second only to the 112th Congress.

On January 18, Congress had six weeks to act to approve funding for the 2023–2024 fiscal year. By our calendar, that now puts their deadline somewhere at the beginning of March. Pair that with a rather significant foreign aid bill sitting on the desks of the House, and what a time to take a two-week vacation. Nice work if you can get it!

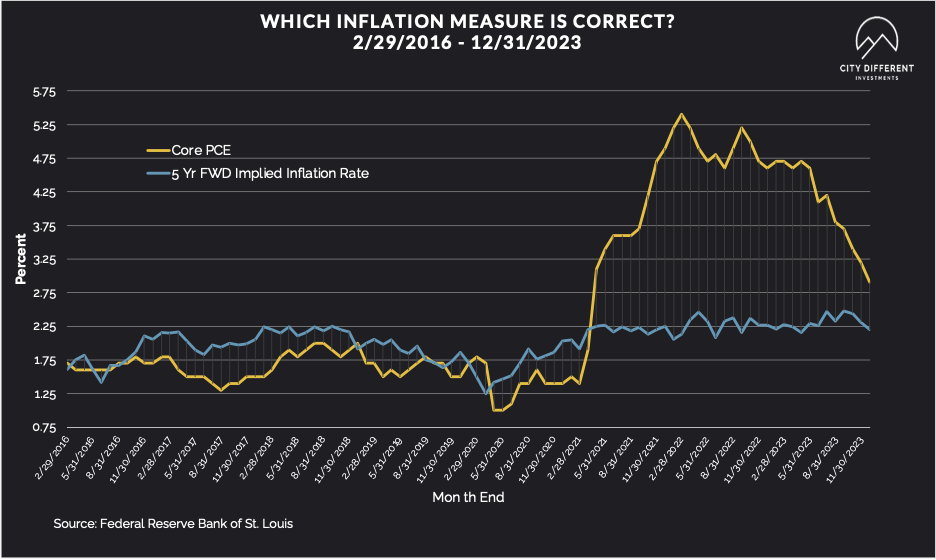

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week of February 16 at 2.38%, ten basis points higher than the February 9 close of 2.28%. The 10-year Breakeven Inflation Rate finished the week at 2.33%, eight basis points higher than the close of February 9.

MUNICIPAL CREDIT

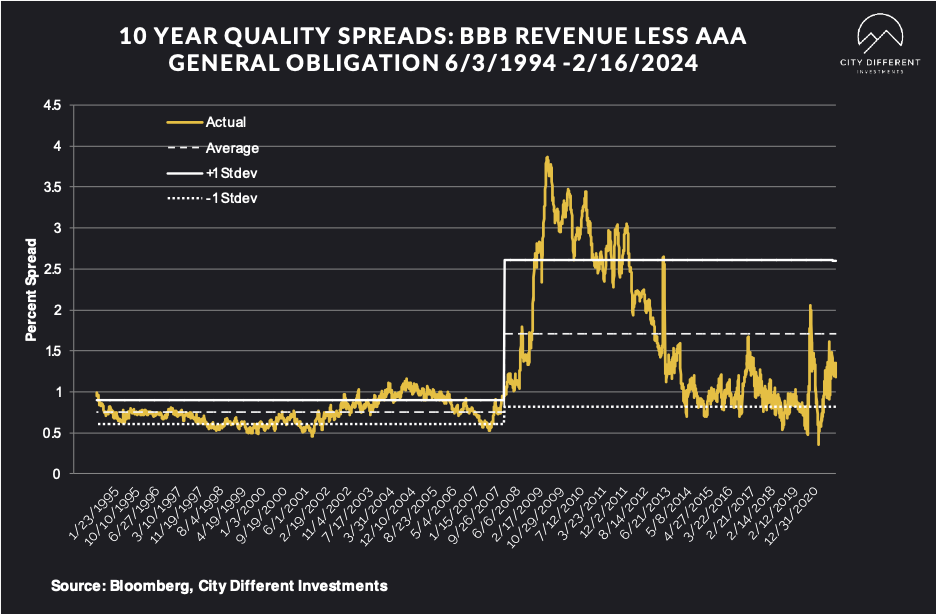

10-year quality spreads (AAA vs. BBB) as of February 16 were 1.60%, five basis points higher than the February 9 reading of 1.55% (based on our calculations). The long-term average is 1.71%.

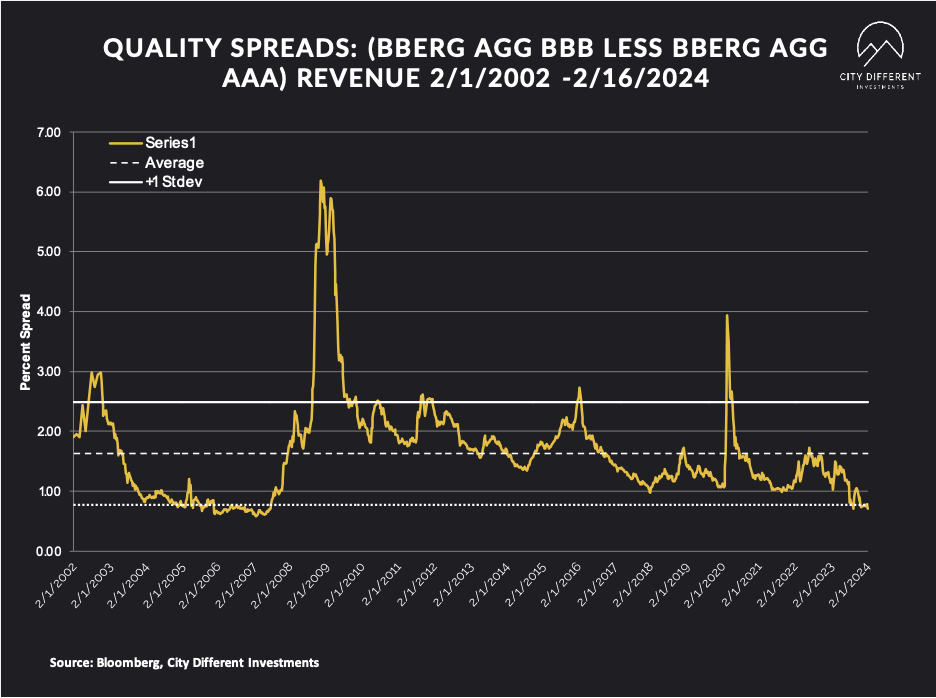

Quality spreads in the taxable market are not attractive but were slightly lower, ending the week at 0.71%, five basis points lower than last week. High-yield quality spreads were 2.95% on February 16.

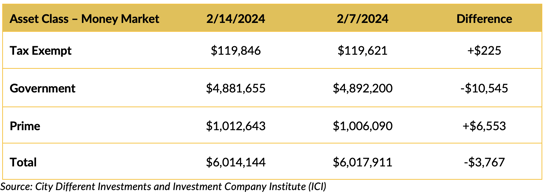

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds, except for government funds, won the week.

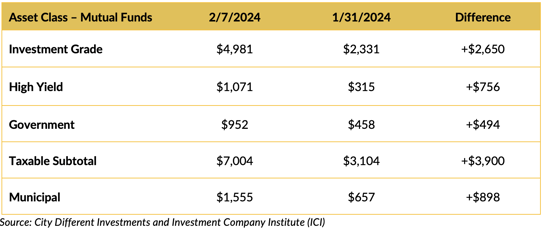

Mutual Fund Flows (millions of dollars)

Bond funds saw an increase in flows across the board.

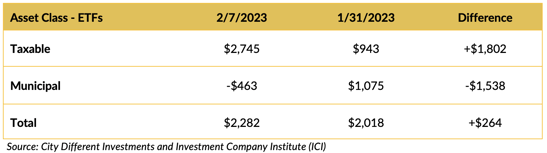

ETF Fund Flows (millions of dollars)

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Supply for the municipal tax-exempt calendar will likely remain uneven for the next few weeks to start the year. This week’s municipal tax-exempt calendar estimates are $4.7 billion in new issuance.

CONCLUSION

Both the Treasury and municipal yield curves remain inverted. We believe the best positioning in both markets to maximize income per unit of duration risk and protect one from the “cash trap” is in the short end of both markets. The belief that inflation is under control looks to be a bit premature.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.