WEEK ENDING 12/01/2023

- Chair Powell tries to calm fixed-income markets.

- 60% probability of a Q1 rate cut.

- Hostages released during last week's Israeli-Hamas cease-fire.

A CITY DIFFERENT TAKE

As we enter the holiday season, the fixed income markets are behaving as if they received their presents early — low inflation and a gentle slowdown in the economy. Chair Powell tried to do his best Scrooge impression, but the markets were not buying it.

The market's expectation of 2024 rate cuts, as measured by Bloomberg’s WIRP function, reached 60%, targeting a March timeframe. Markets do tend to get ahead of themselves. The November inflation reports have come in under expectations and show that no matter which series you look at, inflation numbers seem to have rolled over but are still considerably above the Fed’s 2% target.

Maybe with each additional friendly report, an “inflation angel” gets their wings?

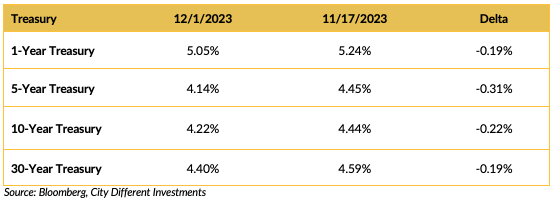

CHANGES IN RATES

The rally in Treasury yields continued this week. There was a little respite on Thursday after the PCE numbers were released. Year-over-year core PCE came in at 3.5%, lower than last month’s 3.7%, but matching expectations. This number is still well above the Fed’s 2% target. The fixed-income markets are pricing in Fed rate cuts at the end of Q1 2024 with a probability of 56.2%.

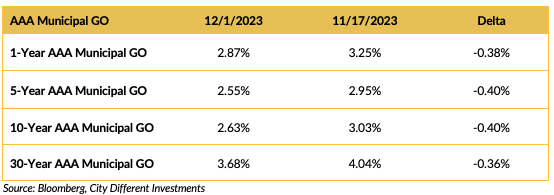

The municipal market has rallied much more than the Treasury market since Thanksgiving, aided by low levels of new issuance supply and market participants suffering from a bad case of a certain kind of FOMO — fear of not being fully invested and missing the much-expected January rally.

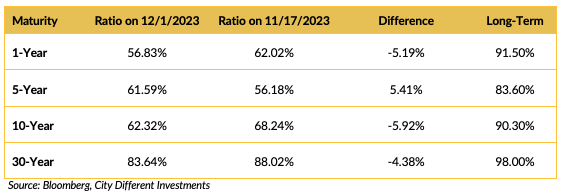

The municipal/Treasury ratios are lower (except for the 5-year maturity). Municipal bonds have outperformed the Treasury market over the last two weeks. The municipal/ Treasury ratios indicate that Treasury securities provide a better after-tax yield than AAA general obligation municipal bonds. We will see how long this lasts.

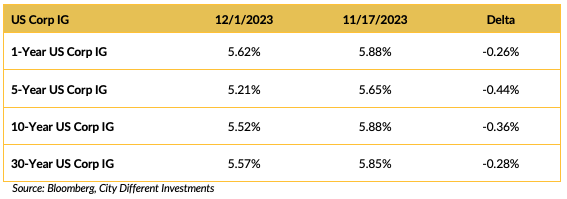

Corporate yields moved mostly lower last week; corporates joined the party.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Congress has one less Republican representative from New York. George Santos was expelled from the House last week for ethics violations. Because he was not convicted of anything, he retains certain privileges as a now-former member of Congress, including access to the House floor, dining room, gym, and cloakroom — but not security. Ain’t life grand? (At least in D.C.)

After a brief cessation of violence last week (allowing for the release of a handful of hostages), Israel’s war on Hamas has resumed.

It has been widely reported that Hunter Biden is willing to testify publicly on Capitol Hill, but House Republicans want testimony to be held in a private, closed session. Is that because they are concerned about what photos Rep. Marjorie Taylor Greene will bring?

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.32%, one basis point higher than the November 17 close of 2.31%. The 10-year Breakeven Inflation Rate finished the week at 2.22%, no change from the November 17 close.

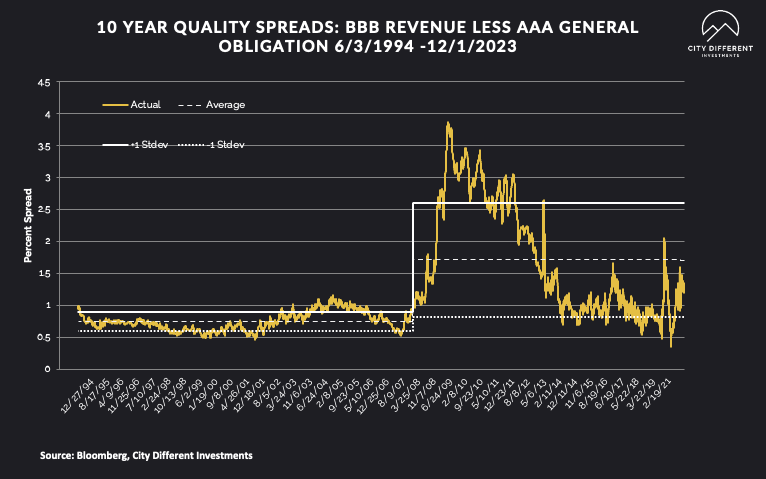

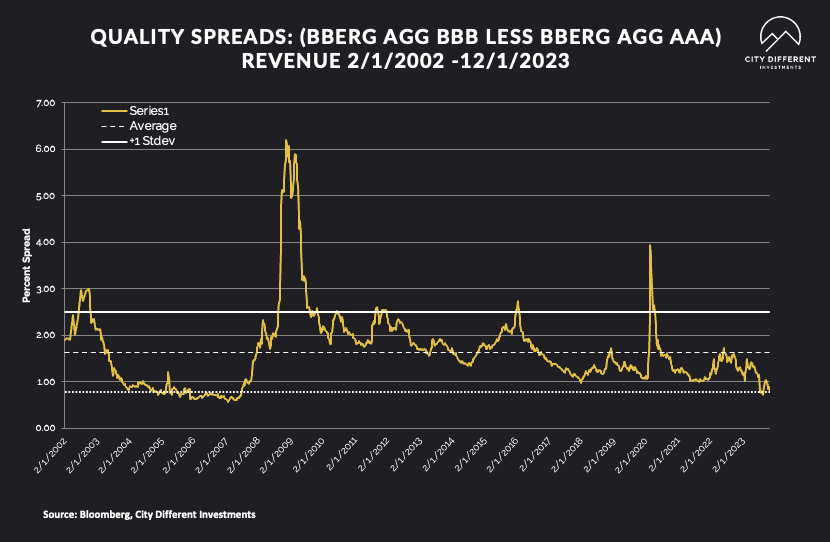

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of December 1 were 1.28%, seven basis points lower from the November 17 reading of 1.35% (based on our calculations). The long-term average is 1.71%.

Quality spreads in the taxable market are not attractive but were narrower last week, ending the week at 0.78%. High-yield quality spreads moved from 3.47% on November 17 to 3.40% on December 1.

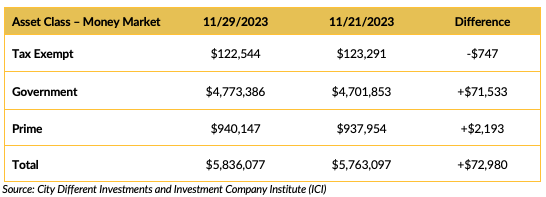

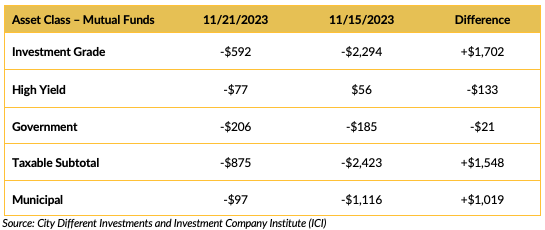

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Mutual Fund Flows (millions of dollars)

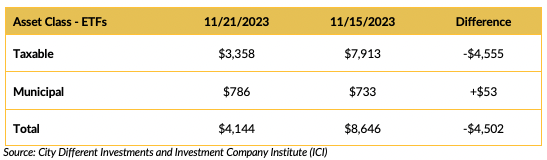

ETF Fund Flows (millions of dollars)

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $11.0 billion (there may be a lump of coal in this package).

CONCLUSION

Fixed income markets are moving, and it looks like there will likely be a Santa Claus rally. However, markets do tend to get ahead of themselves. Inflation, while rolling over, is still above the Fed’s 2% target. Chair Powell tried to do his best Scrooge impression (or was that Greenspan?) and calm this exuberance but to no avail. To paraphrase the Grateful Dead, “We may be going to hell in a bucket, babe. But at least we are enjoying the ride.”

Or maybe Francis Pharcellus Church was correct. “Yes, Virginia, there is a Santa Claus.”

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.