WEEK ENDING 12/08/2023

- Will Chairman Powell bring coal to the holiday party?

- The market has made the Fed’s job tougher!

- This week’s Fed meeting and inflation reports may add volatility to the holiday market.

- “Hold on to your butts.”

A CITY DIFFERENT TAKE

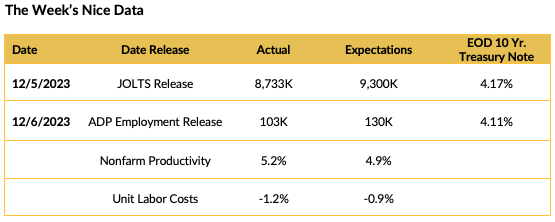

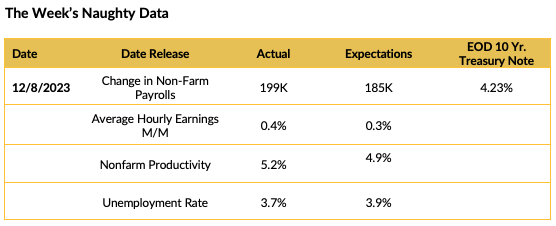

The fixed income markets continued to rally (higher prices / lower yields) through most of the week. Friday’s jobs report resulted in a moment of pause, except for the municipal bond market. In keeping with the holiday spirit, we have classified the week’s data releases as either naughty (strong economy, bad for bonds) or nice (weakening economy, good for bonds):

The employment report caused the market to reevaluate the probabilities it assigned to a first-quarter easing by the Fed. Last Friday (12/1), the implied probability, as measured by Bloomberg’s WIRP function, of a significant easing by the Fed in Q1 was 60%, whereas, at the close of business on 12/8, the implied probability was 44.5%.

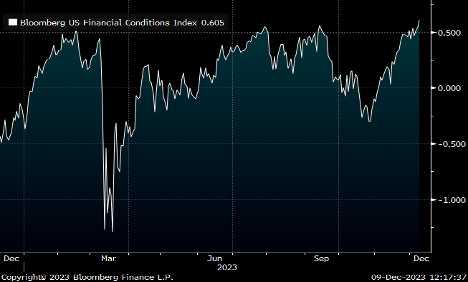

One of the impacts of the recent decline in interest rates is that financial conditions, as measured by the Bloomberg US Financial Conditions Index, are getting less restrictive (a positive value indicates accommodative financial conditions and a negative value indicates tighter financial conditions). The following graph shows the index’s values for all of 2023. The negative reading on 10/25/2023 was -0.281, which corresponded with the yield on the 10-Year Treasury note of 4.96%. The current reading of +0.61 (the highest reading for 2023 YTD) corresponds to a 4.23% yield on the 10-Year Treasury note.

What does this mean in simple English? Higher interest rates helped the Fed in its mission to slow the economy and reduce inflation to its 2% target. Lower interest rates did the opposite.

All this is setting the stage for an upcoming Federal Reserve meeting and the release of inflation data. Given recent volatility in the fixed income markets, these events could make for an interesting week. To borrow a line from Samuel L. Jackson’s character in Jurassic Park, “Hold on to your butts.”

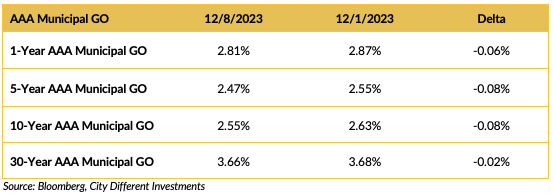

CHANGES IN RATES

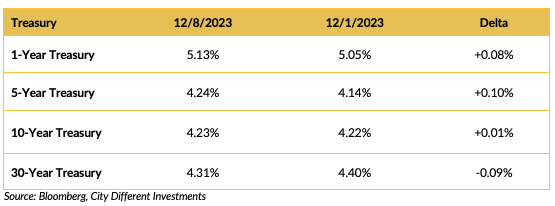

The rally in Treasury yields took a pause at the end of the week as the employment report lent a little doubt to the market’s belief that the Fed would be cutting the federal funds rate in the first quarter of 2024. It is times like these that I often think of the Ben Franklin admonition to, “doubt a little of his own infallibility”.

The municipal market continued to rally as the Treasury market took a breather. We believe that the municipal market is suffering a little bit from FOMO. Market participants are taking these last, typically big new issue weeks to set up for an anticipated January rally (January effect). This is despite municipal bond mutual funds continued suffering from withdrawals.

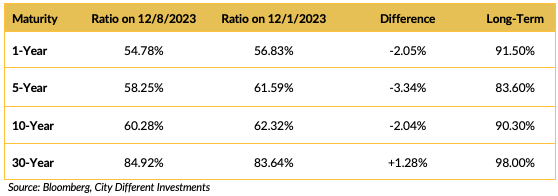

The municipal/Treasury ratios are lower (except for the 30-year maturity). Municipal bonds have outperformed the Treasury market over the past week, and the municipal/ Treasury ratios indicate that Treasury securities provide a better after-tax yield than AAA general obligation municipal bonds. We will see how long this lasts.

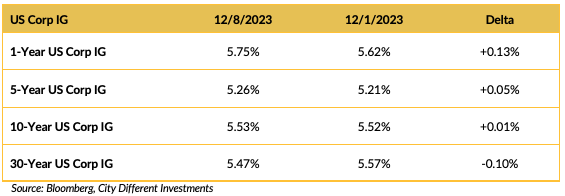

Corporate yields moved mostly higher last week; corporates mostly paused along with Treasuries.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Three presidents of prestigious universities testified before Congress about antisemitism on their respective campuses. All three did not do well, and one has since resigned from her position.

Israel and Ukraine aid funding has been tied up in the Senate by Republicans over border disputes.

“The vote was 49 in favor to 51 against, leaving the $110.5 billion measure short of the 60 votes needed in the 100-member Senate to pave the way to start debate, threatening President Joe Biden's push to provide new aid before the end of 2023.”

It seems to us that these funding bills should not be conflated with border security. All are important but very different, and the impacts on the US are wide-ranging on the world stage. This must be Washington DC calculus at work.

Kevin McCarthy announced that he is leaving the House of Representatives at the end of 2023. This follows George Santos’s expulsion and the announcement of several other Republican House members that they will not seek reelection in 2024. Rep. Michael Burgess of Texas, Rep. Debbie Lesko of Arizona, and Rep. Kay Granger of Texas are not seeking reelection in 2024. Rep. Bill Johnson of Ohio is also leaving Congress in March of 2024.

A government shutdown will be averted this year, but in 2024, the key date to worry about is January 19, for funding agencies like Agriculture, Transportation, Housing and Urban Development, and Veteran Affairs. Other agencies have a February 2nd deadline. Happy New Year!!

Liz Cheney has begun her book tour; enough said.

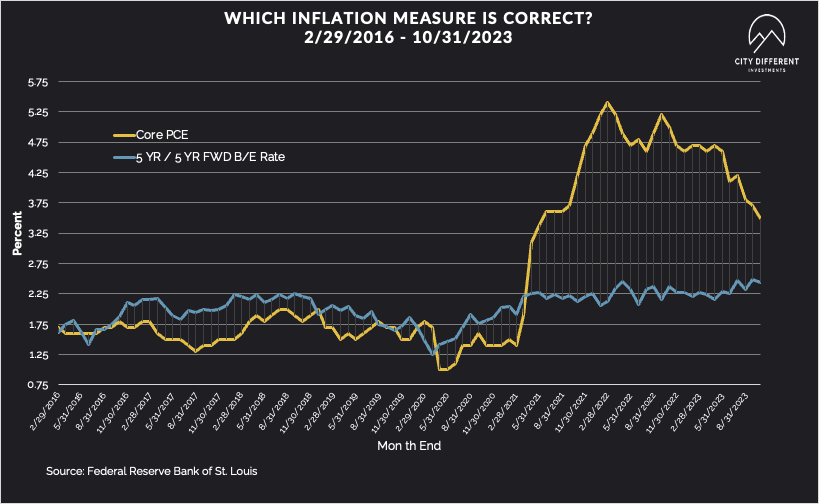

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.31%, one basis point lower than the December 1 close of 2.32%. The 10-year Breakeven Inflation Rate finished the week at 2.21%, one basis point lower from the December 1 close.

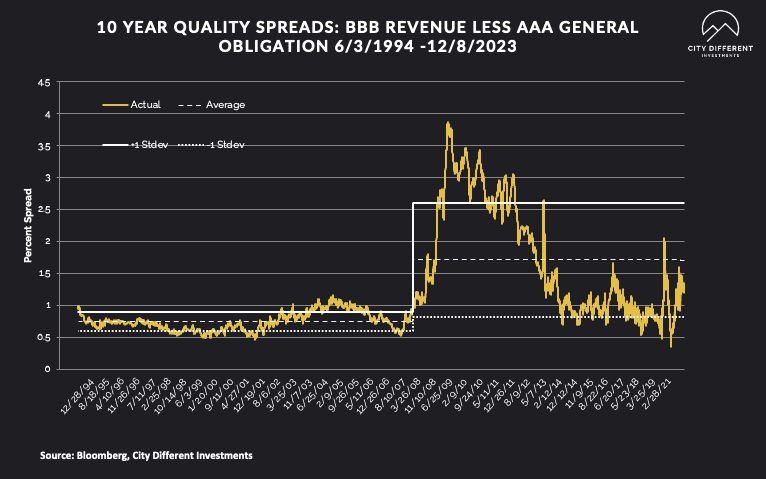

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of December 8 were 1.35%, seven basis points higher from the December 1 reading of 1.28% (based on our calculations). The long-term average is 1.71%.

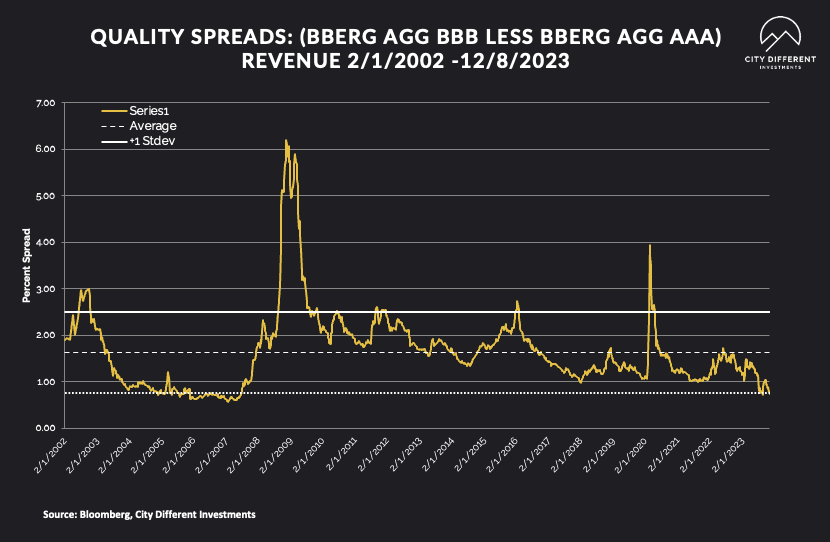

Quality spreads in the taxable market are not attractive but were narrower last week, ending the week at 0.73%. High-yield quality spreads moved from 3.44% on December 1 to 3.26% on December 8.

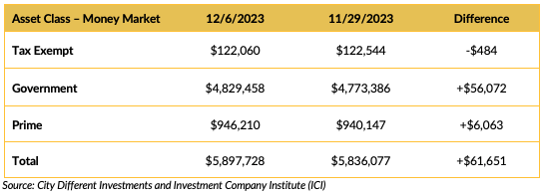

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

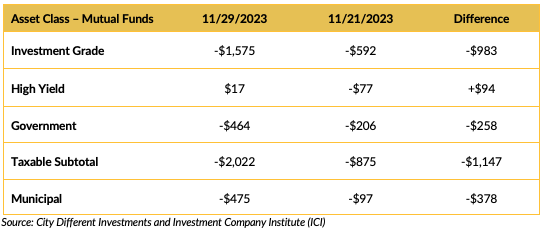

Mutual Fund Flows (millions of dollars)

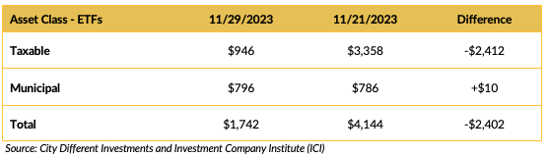

ETF Fund Flows (millions of dollars)

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $4.7 billion (there may be a lump of coal in this package).

CONCLUSION

This week should be interesting. We have the Fed meeting mid-week and the latest inflation readings on Tuesday. The rally in rates has made the Fed’s job harder, no doubt. What will the market find in its collective stocking, a bit of coal, perhaps? We think you all are getting as tired as we are with these not-so-veiled holiday references. We promise to stop soon!

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.