WEEK ENDING 11/17/2023

- Fed’s dovish tone and positive inflation data knock yields off their peak.

- Government debt sales continue to climb.

- Happy Thanksgiving! “Thankfully,” we’re taking a pause from writing next week.

A CITY DIFFERENT TAKE

October's CPI showed meaningful progress toward lower inflation. Our favorite summation of the Federal Reserve's current policy comes from a tweet by Nick Timiraos of The Wall Street Journal: "The first rule of mission accomplished is that you never say mission accomplished." While there are tones of cooling inflation and a pause from the Fed, Chair Powell recently insisted that the Fed had not yet made up its mind about whether to continue to pause at the December meeting. But market participants refuse to believe the Chair. The CME FedWatch Tool puts the probability of rates remaining the same at 99.8% with a 0.2% probability of an ease.

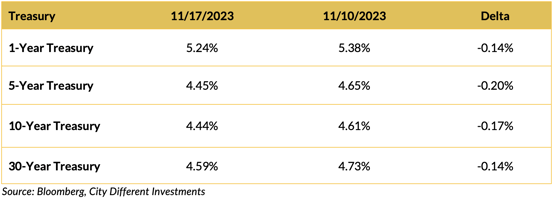

As we line up all the data, it does support a pause. Ten-year treasury yields have stopped pushing higher and remain between 4.4% and 5%.

A closer examination of the data shows the following.

- A big slide in October ISM numbers, suggesting the goods side of the economy is cooling. Services trended downward as well but remained robust.

- Employment slowdown also offers support for the pause. Nonfarm payrolls only increased by 150,000. The unemployment rate rose a smidge from 3.8% to 3.9%. (Keep in mind 48,000 members of the United Auto Workers union went on strike.)

- CPI changes were also respectable, trending in the right direction.

While these three data points make a case for a pause, remember we are not yet at 2% inflation. There is a concern that the economy and labor market are both strong, which is why the FOMC participants have not committed to a long pause. We think the markets are premature in their optimism that the Fed is done raising rates.

The markets are pricing a $16 billion sale of 20-year Treasuries and are having indigestion absorbing supply in a shortened holiday weekend. The 20-year auction could be at risk as last week’s 30-year auction was tepid.

CHANGES IN RATES

Treasury yields moved significantly lower last week, driven by what the market perceived as an inflation-friendly CPI report. Y/Y core CPI came in at 4%, ten basis points below expectations. The market may have perceived this as a friendly report, but markets tend to overreact. Core CPI is still well above the Fed’s 2% target.

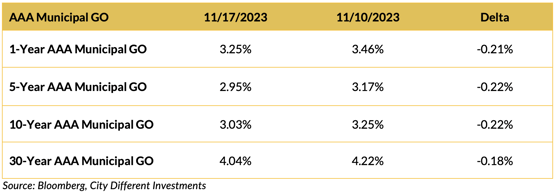

The overreaction to the CPI report was not limited to the Treasury market. Couple that with the seasonal reduction in the supply of new issue municipal bonds ahead of January, and you have a volatile combination.

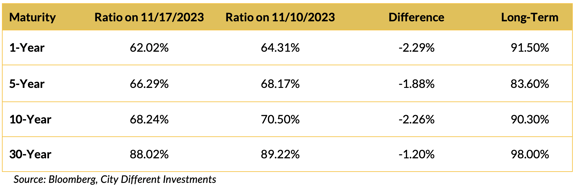

The municipal/Treasury ratios are lower and, in some cases, have broken through breakeven levels.

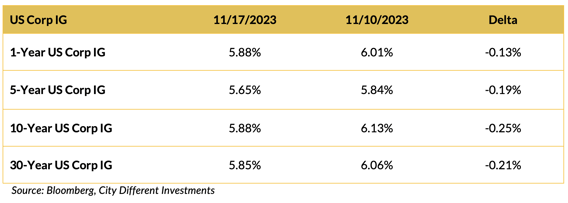

Corporate yields moved mostly lower last week; corporates joined the party.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Reuters earlier this week published a story titled “Forever war: Israel risks a long, bloody insurgency in Gaza.” Unfortunately, the situation in the Middle East seems to be inching toward that direction. And as Kyiv endured a second successive night of drone attacks, it’s clear the Russia-Ukraine war also does not have an end in sight.

The Senate passed and the President signed a stop gap funding bill that keeps the government running through early next year. Despite this success in the two chambers, President Biden's rating is at an all-time low, driven by the perception of his handling of foreign relations. Both wars weigh heavy on his reelection campaign.

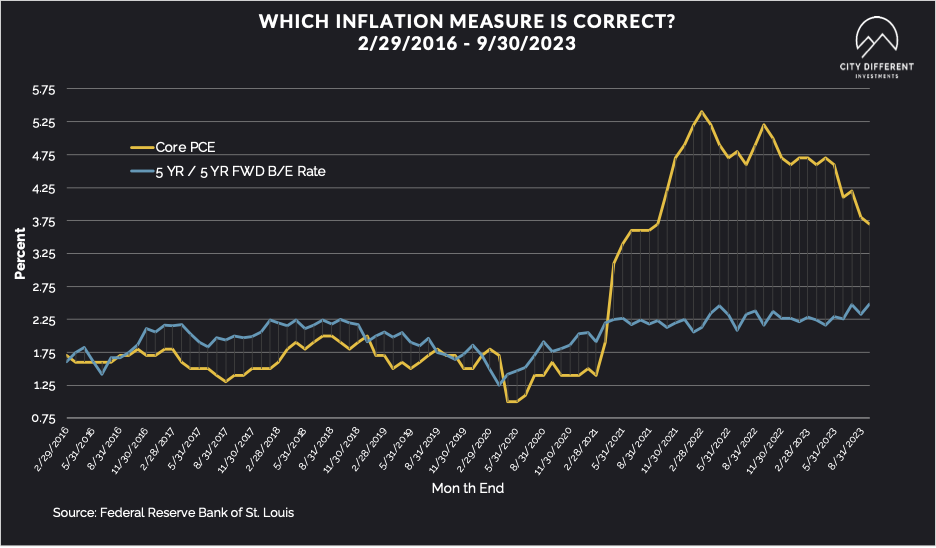

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.33%, three basis points lower than the November 10 close of 2.36%. The 10-year Breakeven Inflation Rate finished the week at 2.28%, matching the November 10 close.

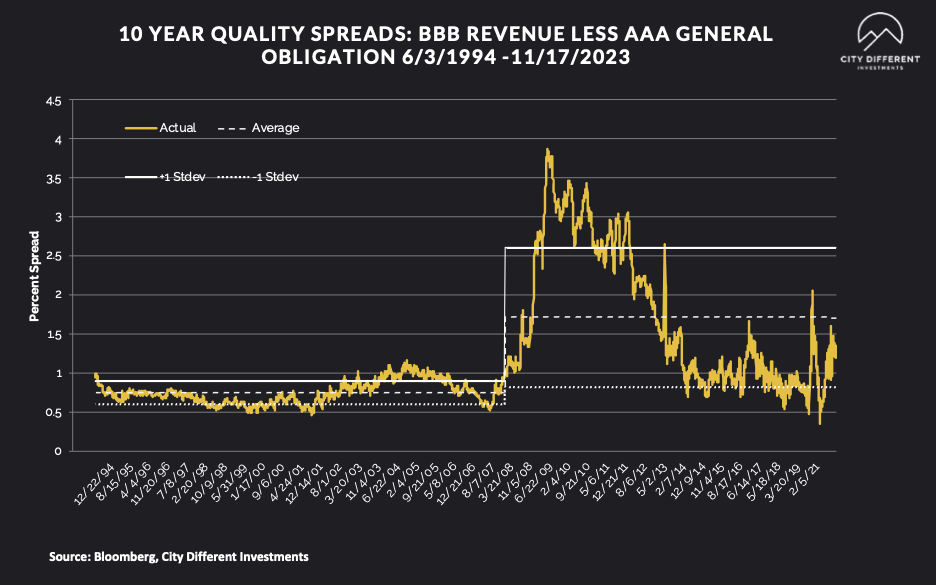

MUNICIPAL CREDIT

The 10-year quality spread (AAA vs. BBB) as of November 17 was 1.35%, ten basis points higher than the November 10 reading of 1.25% (based on our calculations). The long-term average is 1.71%.

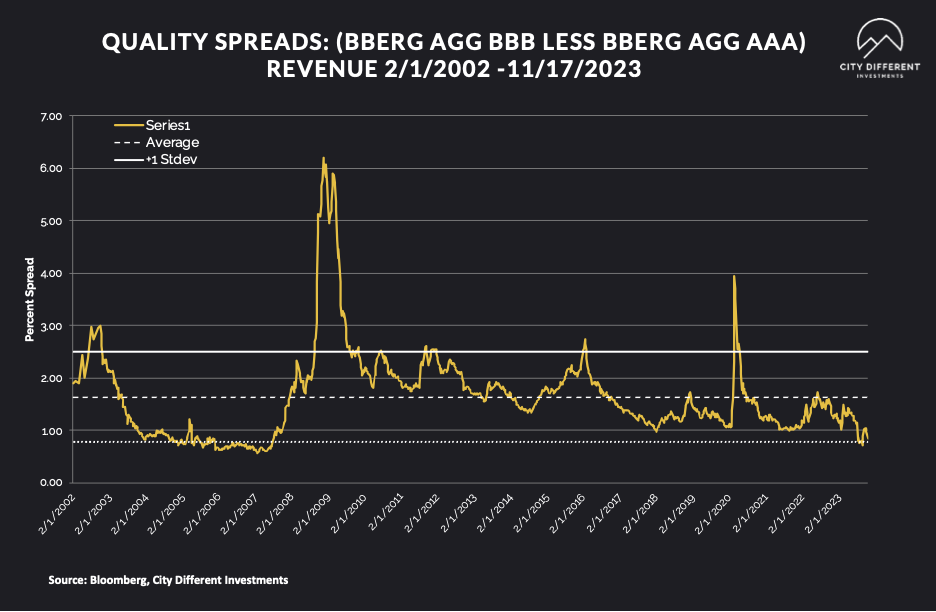

Quality spreads in the taxable market are not attractive but were narrower last week, ending the week at 0.84%. High-yield quality spreads moved from 3.49% on November 10 to 3.47% on November 17.

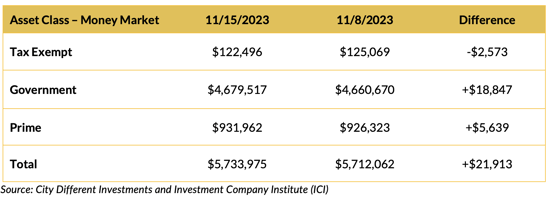

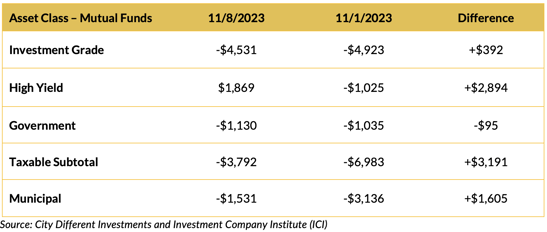

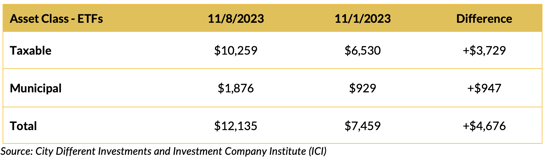

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Mutual Fund Flows (millions of dollars)

ETF Fund Flows (millions of dollars)

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $330 million. A slow holiday week in the muni market.

CONCLUSION

This is a slow holiday week with the 20-year Treasury auction being the highlight for the markets. Slowing inflation print has had an outsized reaction in both the bond and the stock market. However, we still don’t see the inflation threat completely subsiding; the hesitation from Fed officials to commit to a long pause reflects that.

Finally, we’d like to wish you a very happy Thanksgiving. We’re incredibly thankful for your readership and your trust in CDI. We’re off from writing next week, but we’ll be back December 4 with an all-new Week in Review.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.