WEEK ENDING 11/10/2023

- Moody’s moves US sovereign outlook to “negative.”

- Market participants’ outlooks and opinions mixed.

- Honoring our veterans.

A CITY DIFFERENT TAKE

The government is funded through this Friday. But the ratings agencies and the American public are getting tired of repeated political brinksmanship. In addition, the federal debt-to-GDP ratio is on an explosive path meaning the U.S. economy will be devoting a larger percentage of its GDP to debt service.

All three ratings agencies have warned the U.S. that it has two options in the face of a very large fiscal deficit: reduce spending or increase revenue. Moody's recent ratings watch is meaningful since it is the only rating agency that has continued to maintain a Aaa rating for U.S. sovereign debt since 1917.

What does a downgrade mean for the country’s debt? In the financial markets, this leads to higher yields for the Treasury. That permeates into all debt instruments, including higher mortgage rates.

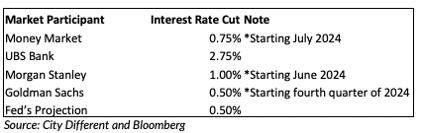

The market is still absorbing the “higher for longer” Federal Reserve. However, the “sell” side is closing 2023 with diverging prognoses on rate cuts for next year. At City Different, we have no reason to believe the Fed will change its guidance of a higher rate well into the second half of the year. But to underline the diverging opinions of market participants, we present a quick taste of interest rate cut jostling.

The summary of economic changes released by the Federal Reserve in September outlines two quarter-point cuts penciled in for 2024 and 2025 with a policy rate ending at 3.9%.

Finally, November 11 was Veterans Day. We’d like to take a moment to acknowledge all the brave men and women who served or are serving in our armed forces.

Veterans Day, formally known as Armistice Day, also commemorates the end of World War I. The armistice was signed on the morning of November 11, 1918, ending hostilities at the eleventh hour of the eleventh day of the eleventh month. Little did anyone realize that this would put events in motion, eventually leading to World War II.

CHANGES IN RATES

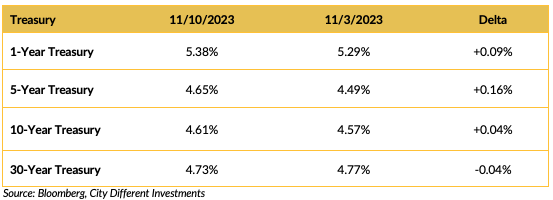

Treasury yields moved in different directions last week. Short-term rates moved higher, and longer-term rates moved lower. The results of the Treasury auction could be characterized as “weak.” Chairman Powell’s comments later in the day that the Federal Reserve may not be done raising short-term interest rates added to the confusion.

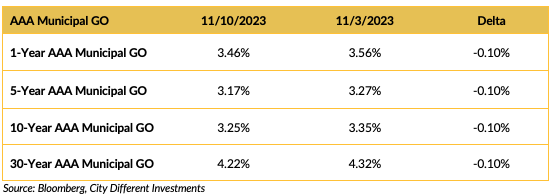

Yields in the municipal bond market moved lower across the maturity spectrum last week. Moderate new-issue supply and market participants preparing for the January effect were the major drivers of this move.

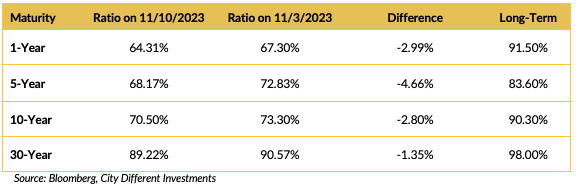

The municipal/Treasury ratios were down on the week and are still well below their long-term average.

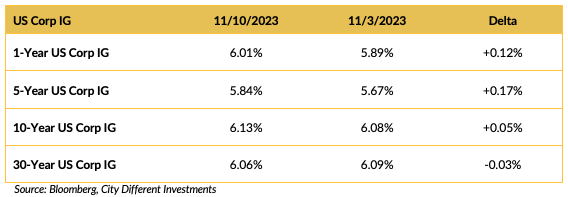

Corporate yields moved mostly higher last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Global conflict continues, and there is much to report. There is increased probability of a full-scale war breaking out between Israel and militants in Lebanon. The U.N. has withdrawn its humanitarian efforts from the region.

Political instability continues in Washington. Federal agencies have started to prepare for a shutdown. House Speaker Mike Johnson proposed a temporary plan to fund the government into early next year without dramatic spending cuts, hoping to buy some time to negotiate more significant budgetary items. Johnson is operating with a slim majority in the House, though enough Democrats could agree to such a proposal that it would move along to the Senate.

Former Speaker Kevin McCarthy struck a similar deal a couple of months ago, which led to him being ousted from the position. It’s unclear whether House Republicans will forgive Johnson for making such a compromise, given the narrow timeframe since his election to get a deal done.

Finally, we look toward 2024. Recent polls show that President Biden has a re-election problem and is trailing former President Trump in almost every battleground state. But how accurate are the polls a year before a presidential election? The answer: “not very.” Regardless, it will likely be an extremely tight race.

WHAT, ME WORRY ABOUT INFLATION?

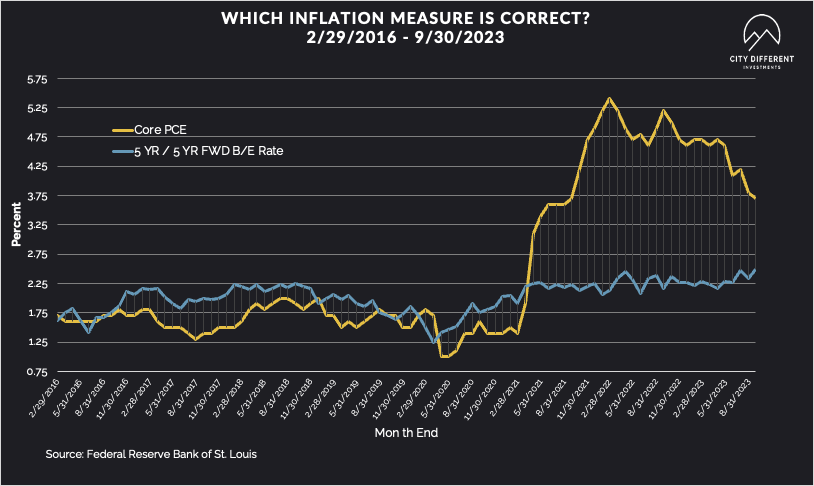

The 5-year Breakeven Inflation Rate finished the week at 2.36%, ten basis points lower than the November 3 close of 2.46%. The 10-year Breakeven Inflation Rate finished the week at 2.33%, six basis points lower than the November 3 close.

MUNICIPAL CREDIT

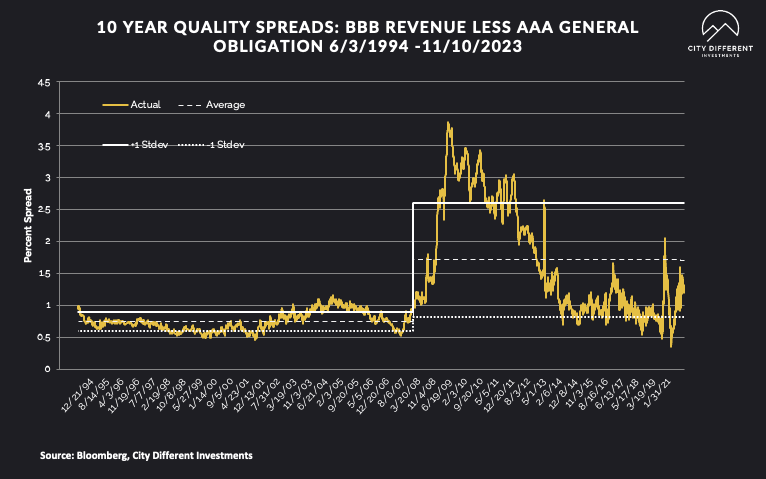

10-year quality spreads (AAA vs. BBB) as of November 10 was 1.25%, six basis points lower than the November 3 reading of 1.31% (based on our calculations). The long-term average is 1.71%.

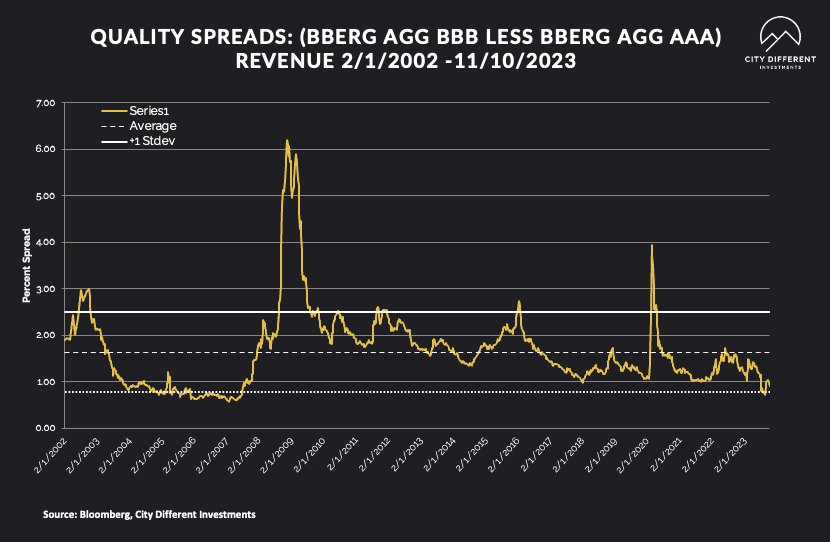

Quality spreads in the taxable market are not attractive but were marginally narrower last week, ending the week at 0.91%. High yield quality spreads moved from 3.53% on November 3 to 3.49% on November 10.

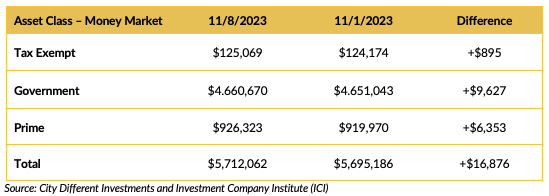

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Market participants continued to be enamored with money market funds. One thing we have learned from playing too much pool is that your initial shot may not be as important as your “leave.” What will investors do when money market rates decline? One would think that these alternative choices will be higher-priced when the herd of money market fund investors begins to move. Is it not better to get ahead of the herd? Yes! Please contact us if you would like to learn more about “The Cash Trap.”

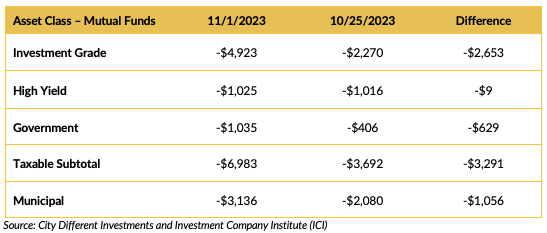

Mutual Fund Flows (millions of dollars)

Bond funds were again the “red-headed stepchild” of the cash flow sweepstakes. All categories we follow saw negative cashflows last week.

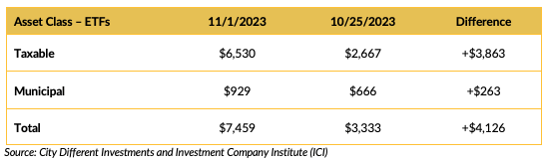

ETF Fund Flows (millions of dollars)

ETF flows were positive last week. So maybe it’s not the asset class but rather the distribution wrapper.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $8.9 billion.

CONCLUSION

The high cost of the U.S. fiscal deficit and political uncertainty are taking a toll on the U.S. sovereign debt rating. Moody's — the only rating agency that currently rates U.S. debt at Aaa — has put it on a negative watch. Speaker Johnson is working on his short-term funding bill to keep the lights on in Washington. The bill needs to pass the GOP-dominated House before this Friday. In market events, the 2024 outlook on rate cuts shows a divergence of opinion among participants.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.