WEEK ENDING 11/03/2023

- A kinder, gentler Fed? Color us suspicious.

- A slowing jobs picture?

- What does it all mean for inflation?

A CITY DIFFERENT TAKE

The Federal Reserve Board held its two-day meeting last week in which they left policy unchanged. The real interesting news came from the presser that followed the announcement:

“We're not confident that we haven't, we're not confident that we have” reached that sufficiently restrictive plateau, Powell told reporters. “Inflation has been coming down, but it's still running well above our 2% target ... A few months of good data are only the beginning of what it will take to build confidence.”

Market participants seemed to take Chairman Powell’s comments to mean that the Fed was more dovish about future rate increases. We are not so sure.

This reaction was soon followed by a jobs report that highlighted a cooling employment picture. Nonfarm payroll gains came in at 150,000, below expectations of 180,000. Last month’s increases were revised down by 39,000. The unemployment rate ticked up to 3.9% from 3.8%; the participation rate ticked down to 62.7% from 62.8%. The inputs to inflation, average hourly earnings on an M/M view, 0.2% compared to expectations of 0.3% with a 0.1% positive revision to last month’s reading, is a mixed picture, as are the Y/Y numbers.

All in all, we are suspicious of the market’s reaction to these reports as markets tend to overreact. One of the reasons we are more constructive on the fixed income markets is the relative value (vs. inflation) higher yields provide. With lower yields, those relative values are reduced, but for how long? See our conclusion for complete details.

CHANGES IN RATES

Treasury yields moved significantly lower on the week. The drivers of these moves were the market's perceptions of a softer, kinder Chairman Powell in his presser regarding future Fed moves (We did not hear the same message.). Couple that with softer jobs numbers — nonfarm payrolls came in at 150,000; expectations were for 180,000. Last month’s jobs numbers were revised downward from 336,000 to 297,000. The unemployment rate ticked up to 3.9% from 3.8% the prior month. The 2/10 Treasury spread moved from the prior week’s closing at -0.15% to a more inverted -0.26%. This type of mover would be referred to as a bull flattener.

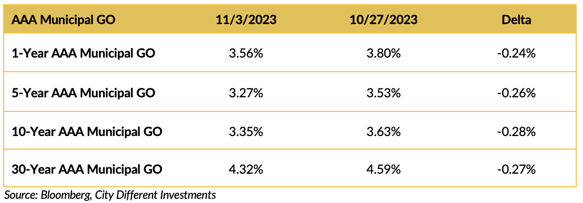

The municipal bond market followed the Treasury in lockstep lower in yield.

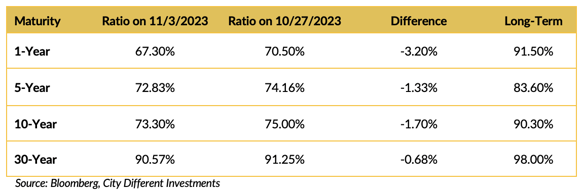

The municipal/Treasury ratios moved lower on the week.

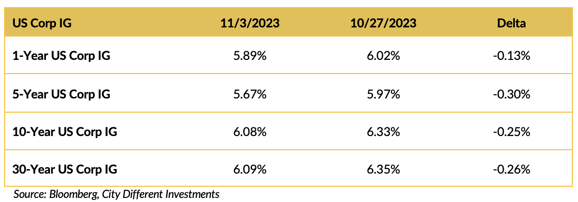

Corporate yields moved lower last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

The House finally has a new speaker. We hope that’s a good thing. One of Speaker Johnson’s first pieces of legislation to pass through the House was the Israel aid bill. It called for $14.5 billion in military aid to be offset by defunding the IRS measures.

“In a departure from norms, Johnson’s package required that the emergency aid be offset with cuts in government spending elsewhere. That tack established the new House GOP’s conservative leadership, but it also turned what would typically be a bipartisan vote into one dividing Democrats and Republicans. Biden has said he would veto the bill, which was approved 226-196, with 12 Democrats joining most Republicans on a largely party-line vote.”

This is reportedly dead on arrival in both the Senate and the White House. This sets the stage for future (but not far off) government shutdown negotiations.

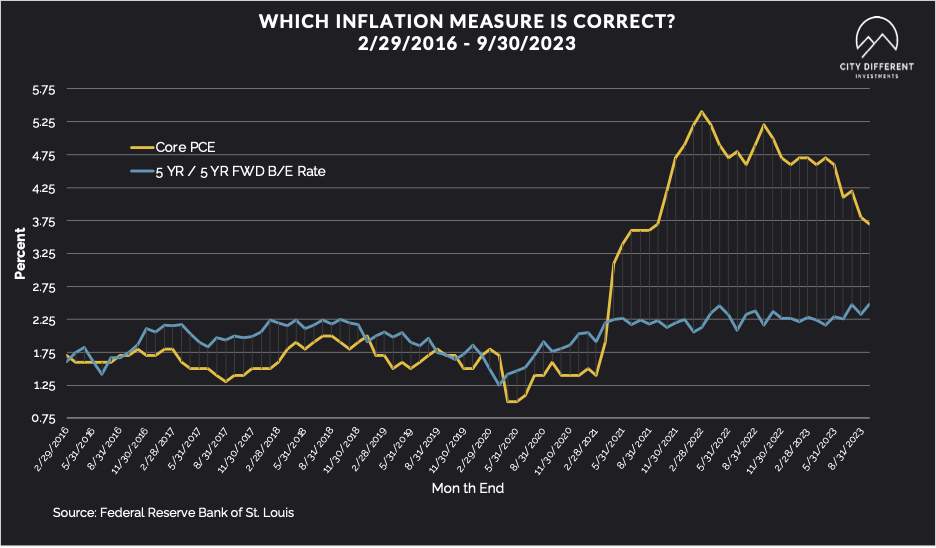

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.46%, one basis point higher versus the October 27 close of 2.45%. The 10-year Breakeven Inflation Rate finished the week at 2.39%, three basis points lower than the October 27 close.

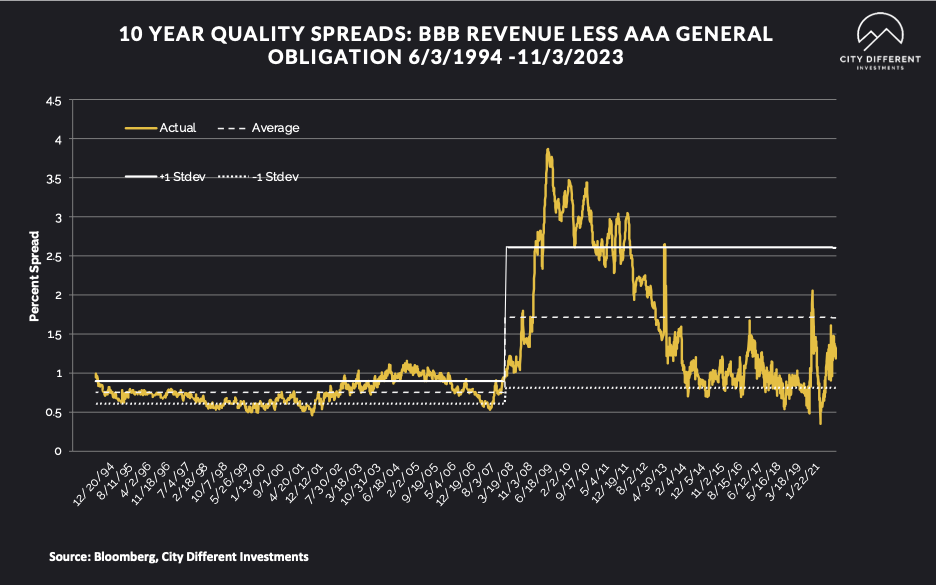

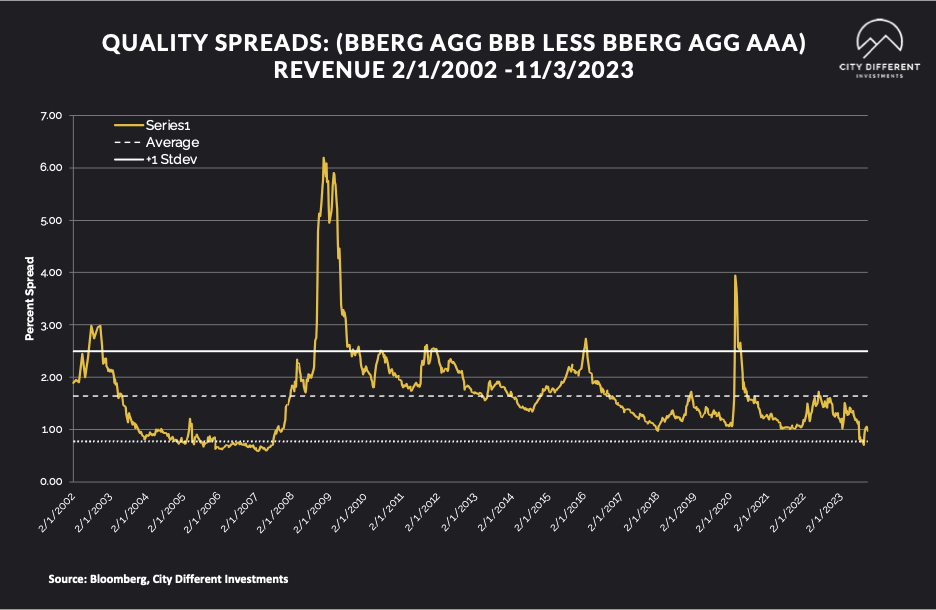

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of November 3 was 1.31%, one basis point lower from the October 27 reading of 1.32% (based on our calculations). The long-term average is 1.71%.

Quality spreads in the taxable market are not attractive but were marginally narrower last week, ending the week at 0.98%. High-yield quality spreads moved from 3.83 on October 27 to 3.53 on November 3.

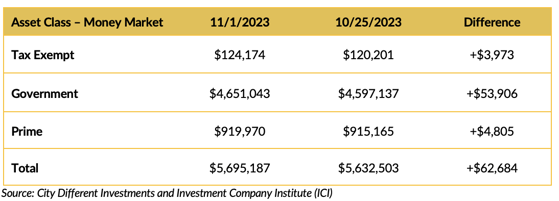

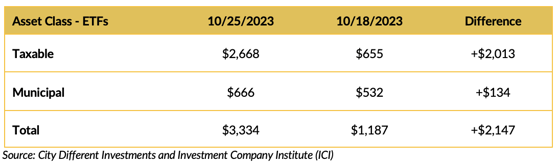

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

This week, market participants loved money market funds, and all categories saw positive flows. Investors should ask themselves, what is the biggest risk to a money market fund? Many believe they are risk-free. The answer is reinvestment risk. See our thoughts on Avoiding the Cash Trap.

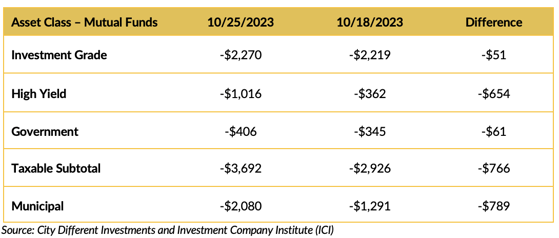

Mutual Fund Flows (millions of dollars)

Investor affection for money market funds was not shared in the bond market. Bond mutual funds' cash flows were negative across the board.

ETF Fund Flows (millions of dollars)

ETF flows were positive last week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $7.4+ billion.

CONCLUSION

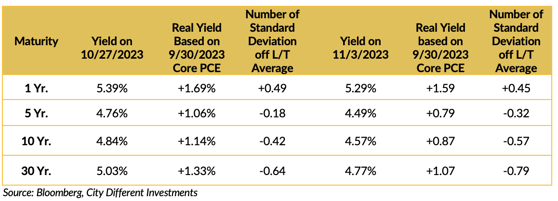

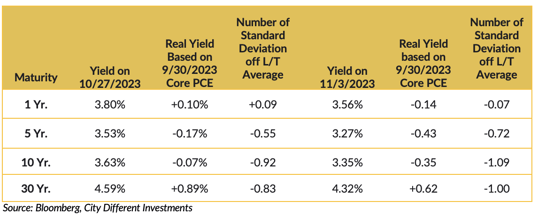

One of the reasons we are growing more constructive on the fixed income markets and counseling “prudent risk-taking” is that higher interest rates are allowing fixed income investors to earn more than inflation is eating up. This is the concept of “real yield” (yield on an investment less an inflation measure). The following tables illustrate this concept:

Treasury Market

Municipal Market

As you can see, the recent rally in yields makes this week’s fixed income markets less attractive than last week's. All measures are in the lower portion of the fair range as we calculate them. That said, we still think fixed income investments are attractive for the prudent risk taker — one that stays short on the maturity spectrum with moderate to high credit quality securities.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.