.png)

WEEK ENDING 10/20/2023

- Chair Powell says inflation is too high, recommitting to a 2% target.

- “Slow” Joe Biden has a good week, garnering compliments from the unlikeliest sources.

- Jim Jordan taps out after a “three count.”

A CITY DIFFERENT TAKE

This was a week filled with major market-moving events. Interest rates moved higher! Cable news market pundits are emphasizing the fearful side of these moves, such as 8% mortgage rates, but we feel this market is full of opportunities for the prudent risk taker.

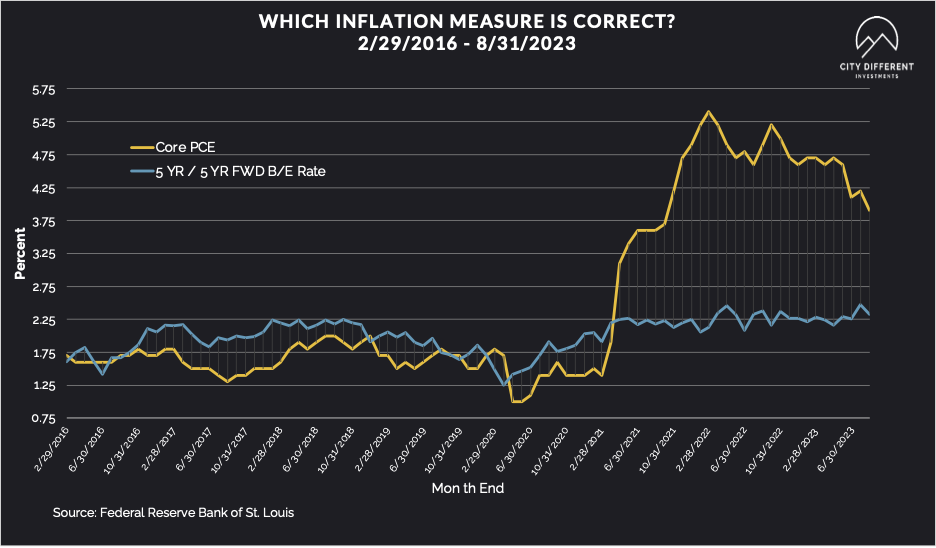

Real yields (yield less inflation measure) are positive. The inversion of the yield curve is lessening. The Treasury 10/2 year yield spread has gone from -1.06% on June 30 to -0.14% on October 20. The bear-steepening process is painful, but often in that pain lies opportunity.

On Thursday, Jerome Powell addressed the Economic Club of New York. Here are the major takeaways and quotes:

- There are signs that inflation is cooling, but the central bank is “resolute” in its commitment to an inflation target of 2%.

- “Inflation is still too high, and a few months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal,” said Powell.

- “Does it feel like policy is too tight right now? I would have to say no,” he said. Still, he noted that “higher interest rates are difficult for everybody.”

We think that the policy of “higher for longer” is still in place, but the market is making significant adjustments ahead of any potential problems, such as:

- Positive real yields based on the last core PCE reading.

- A steeper yield curve through a bear steepener.

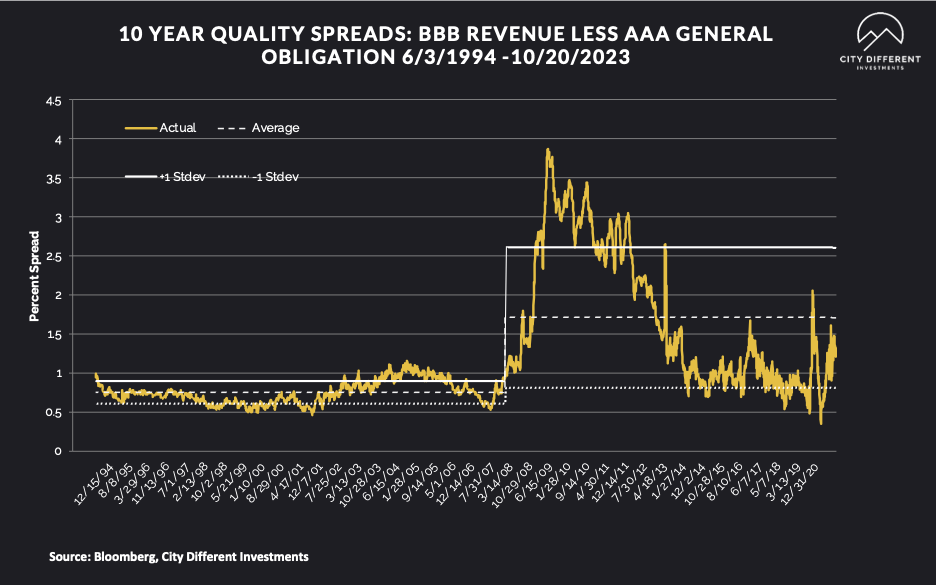

- Wider quality spreads.

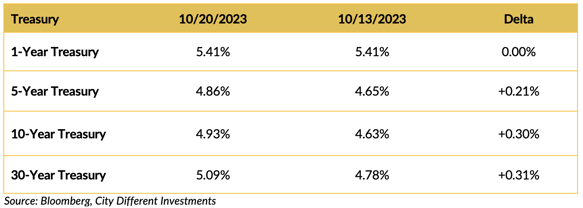

CHANGES IN RATES

Treasury yields moved higher on the week. Should investors be scared of increasing rates? Depending on how one’s fixed-income allocations are positioned, we think not! This is the first time in years that investors are actually earning more than inflation (positive real rates). However, it's important to be aware of potential risks within this market. The yield curve is still inverted, but steepening as we speak. And quality spreads are still very narrow. We believe an actively managed ladder portfolio in the one-to-ten-year range of the yield curve focusing on high-quality securities in the one-to-five-year range of the curve is a good bet (and not just because that’s where we manage the bulk of our fixed-income SMAs). Those portfolios currently provide the best income per unit of duration until the yield curve steepens into a more normal slope.

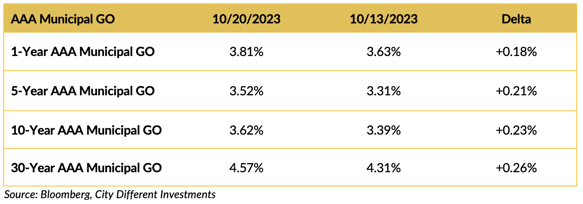

The municipal bond market kept pace with the Treasury market last week as muni yields moved higher, almost in lockstep with their Treasury equivalents.

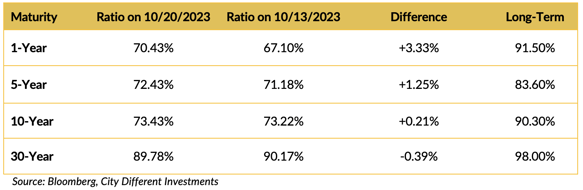

The municipal/Treasury ratios were marginally higher in the short end of the market and marginally lower in the long end of the market as the municipal market adjusts to the unique challenges it faces.

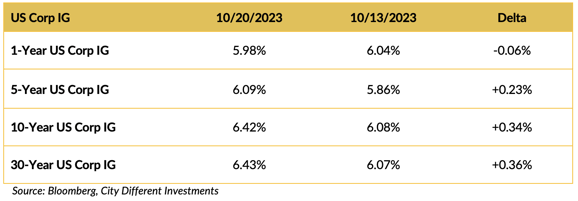

Corporate yields moved higher last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

The president had a pretty good week last week. “Slow” Joe Biden flew to a war zone in Israel to show solidarity in their war against Hamas and undoubtedly engaged in some diplomacy. He reportedly asked the Israelis to learn from the U.S. mistakes in Afghanistan and Iraq, which may explain the delay in the long-anticipated invasion of Gaza.

Biden then returned to the U.S. to give an Oval Office address to the American people. The address received praise from many unlikely sources:

“Fox News political analyst Brit Hume praised the prime-time address President Biden made Thursday evening on the growing unrest in the Middle East, a speech addressing the dueling crises widely viewed as major tests for the president on foreign policy.”

“I think it may be remembered as one of the best, if not the best speeches of his presidency,” Hume said during Fox’s special coverage of Biden’s address. “He was firm, he was unequivocal, he was strong, as he has been — particularly in recent days before he went to Israel, and while he was over there.”

Meanwhile in Congress, a House Speaker still hasn’t been elected after Jim Jordan finally submitted to the proverbial “three count.” Rep. Jordan lost three straight House votes for Speaker, then exited the race.

The clown show continues this week. Kevin McCarthy may be relieved that his time before the “Matt Gaetz of Hell” is over. (That’s not our line, but it’s a great one.) You cannot make this stuff up; if you did, no one would believe it.

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.47%, five basis points higher than the October 13 close of 2.42%. The 10-year Breakeven Inflation Rate finished the week at 2.47%, thirteen basis points higher than the October 13 close.

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of October 20 was 1.21%, five basis points lower than the October 13 reading of 1.26% (based on our calculations). The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive. Municipal market credit spreads usually take a little more time to adjust, given a significant baseline market revaluation.

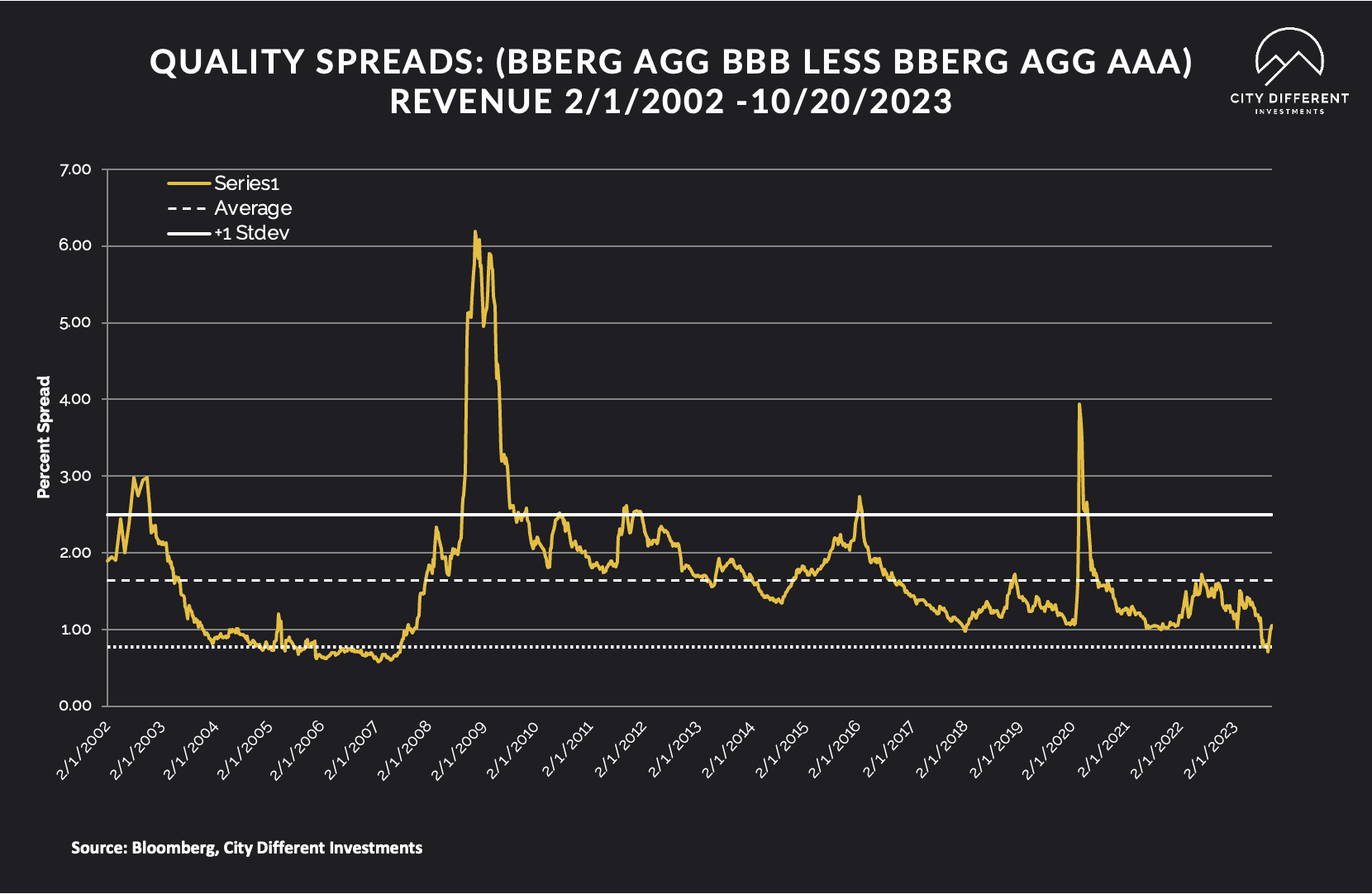

Quality spreads in the taxable market are not attractive but were wider last week, ending at 1.05%. High-yield quality spreads moved from 3.63% on October 13 to 3.86% on October 20.

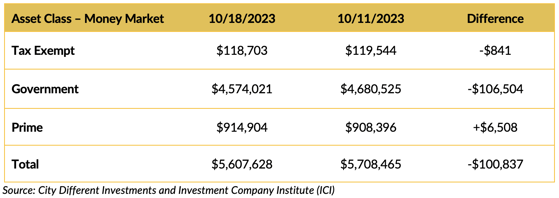

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money funds, in total, saw negative cash flows last week.

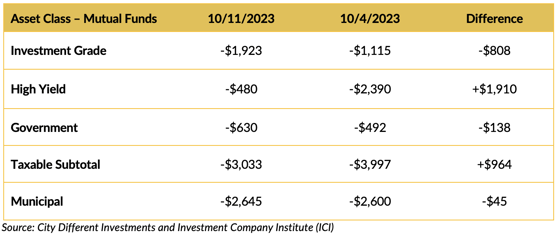

Mutual Fund Flows (millions of dollars)

Bond mutual funds' cash flows were negative across the board.

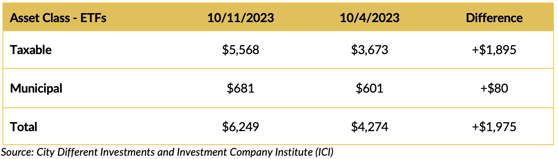

ETF Fund Flows (millions of dollars)

ETF flows were positive last week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $9.5+ billion.

CONCLUSION

Interest rates continue to move higher. The move can be attributed to any number of reasons:

- Middle East tension and the fear of higher oil prices.

- Supply imbalance, larger than expected Treasury auctions.

- A resilient economy and the resultant inflationary pressures.

Any way you slice it, this is the first time in a long while that fixed-income securities look attractive. This is not to say there are no risks to be wary of (inverted yield curve, narrow credit quality spreads, etc.) — but we believe this is a time for prudent risk taking.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.