.png)

WEEK ENDING 9/23/2022

Highlights of the week:

- The Federal Reserve raised targeted short-term rates by 0.75% for the third time in 2022.

- Fixed income and equity markets take it on the chin. Are they of value now?

- Is the Fed done? Time will tell.

A CITY DIFFERENT TAKE

We struggled to come up with this week’s commentary. What should we write about? Then it hit us. It’s all about the Fed!

This week, Chairman Powell announced a third increase in the Fed Funds target rate of 0.75%, bringing the total rate range to 3.00% to 3.25%. Following the announcement, Chairman Powell channeled his best Paul Volcker — again — by standing firm on fighting inflation.

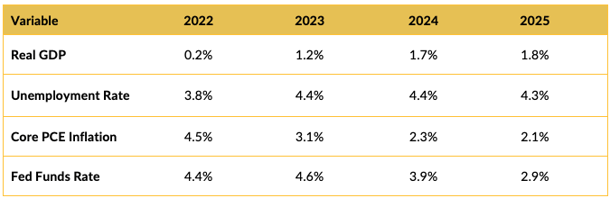

The following table from the Federal Reserve outlines other key Fed forecasts-

Not a very rosy picture. Lower growth, higher unemployment, a higher Fed Funds terminal rate — but hopefully lower inflation. (We find the Fed’s projection of lower inflation circumspect.)

Not a very rosy picture. Lower growth, higher unemployment, a higher Fed Funds terminal rate — but hopefully lower inflation. (We find the Fed’s projection of lower inflation circumspect.)

If the current range for the Fed Funds rate is 3.00% to 3.25% and the Fed’s projection for the 2023 terminal rate is 4.60%, more pain for fixed income investors is on the way. All markets took the news poorly; both equities and fixed income markets were down for the week.

We at City Different Investments like to take a contrarian view toward this new information because being believers in the power of laddered portfolios to generate exceptional long-term returns makes the Fed’s picture a little easier to handle. Rather than thinking about the money we have lost, we are looking at the unique opportunities this new market presents. For the long-term fixed income investor, there are three components of total return: price change, annual interest received, and the compounding of that interest — which is the largest driver of total return by far. As Albert Einstein once said:

“Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn't, pays it.”

Now the world is fresh with new opportunities to earn more compound interest. Ok, this take may not lessen the sting out of any losses incurred — those are sunk costs. And the trick will be to avoid compounding any past mistakes with new, boneheaded decisions. But time, if an investor possesses it, is on the investor's side.

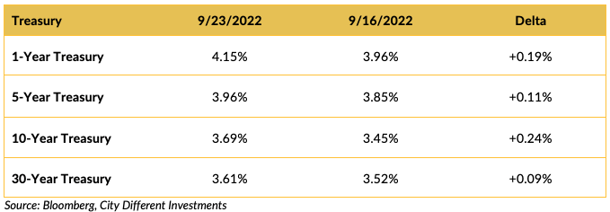

CHANGES IN RATES

Interest rates in the Treasury market moved higher last week. The slope of the yield curve remains inverted for 1 to 30 years and increases its inversion by 0.10% (-0.44% to -0.54%).

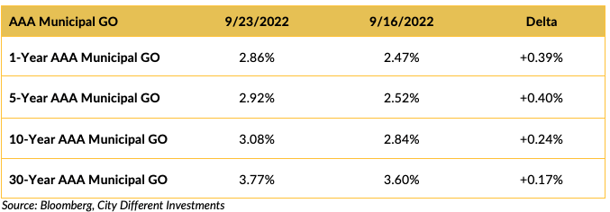

The municipal market, after lagging behind the other fixed income markets in terms of yield adjustment, chose to catch up last week. Municipal interest rates have been moving higher. The front-end rates moved higher still.

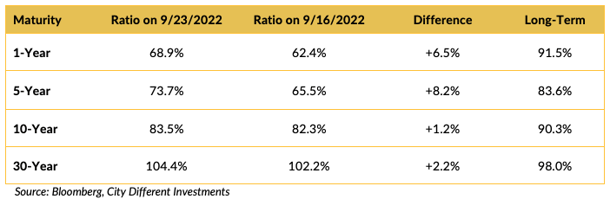

Muni-Treasury ratios moved higher still last week. A higher M/T ratio tends to make Munis a more attractive buy.

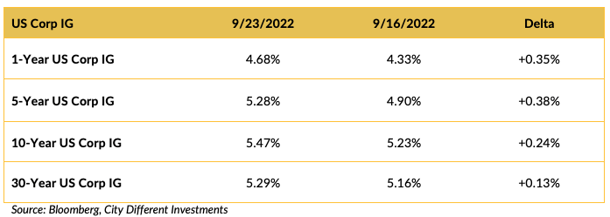

Investment-grade rates marched higher as well. The increase delta was much higher in the front-end tenors.

THIS WEEK IN WASHINGTON

As most world dignitaries attended the Queen’s funeral on Monday, last week was relatively quiet, politically. President Biden did, however, make a strong speech at the U.N. on Wednesday.

In the U.N. speech, the president covered the most salient points on the war in Ukraine. It seems that Russian men aren’t too hot on the idea of conscription. After Putin announced on Wednesday that hundreds of thousands of men would be mobilized, airline tickets out of Russia sold out and checkpoints clogged to countries not requiring a visa to enter. Meanwhile, protests inside of Russia continue to intensify. It seems like everything Putin wanted to accomplish by invading Ukraine has had the opposite effect.

- Ukrainians can fight; Russia’s long-feared military power is a paper tiger (with nukes).

- NATO is expanding.

- Europe looks united (which is easy to do with a bear at your door).

The January 6 select committee will resume televised hearings this week, which should be interesting. Former President Trump’s legal trouble expanded last week with a civil suit from the New York attorney general. If this were a movie, would anyone believe it?

The midterms are roughly six weeks away. (Oh, joy.) Surely, nothing upsetting or disturbing could possibly happen in this lead-up to a potential change in Washington’s power dynamic.

WHAT, ME WORRY ABOUT INFLATION?

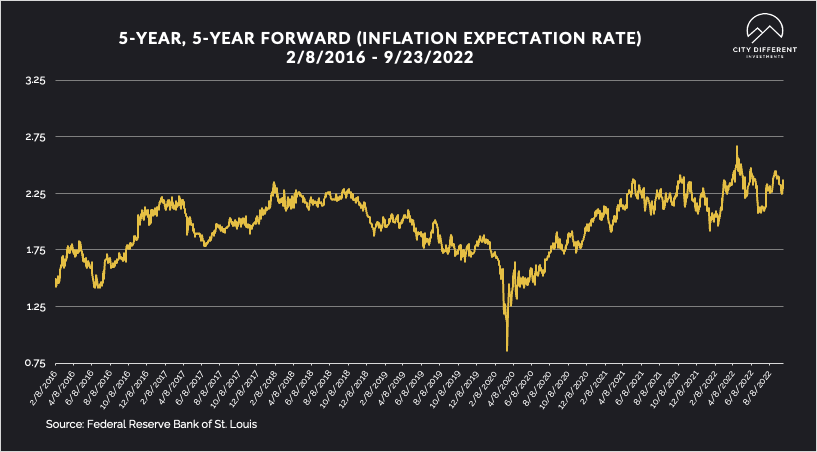

The 5-year Breakeven Inflation Rate ended the week at 2.36%, 9 basis points higher than the prior week closing at 2.27%. The 10-year Breakeven Inflation Rate ended at 2.37%, 1 basis point lower than the last reported observation of 2.38. Both of these readings seem low, given where inflation is today.

MUNICIPAL CREDIT

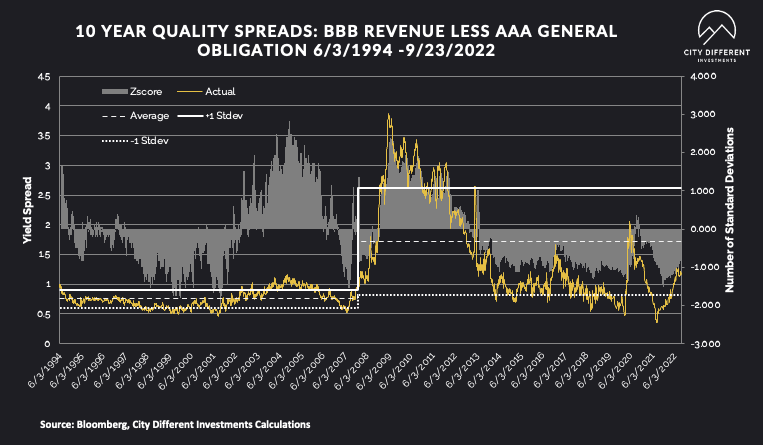

Quality spreads continued to widen, moving further into the fair range, and are starting to pique our interest. While we don’t think the move has been significant enough to change our strategic outlook towards credit, it's getting close.

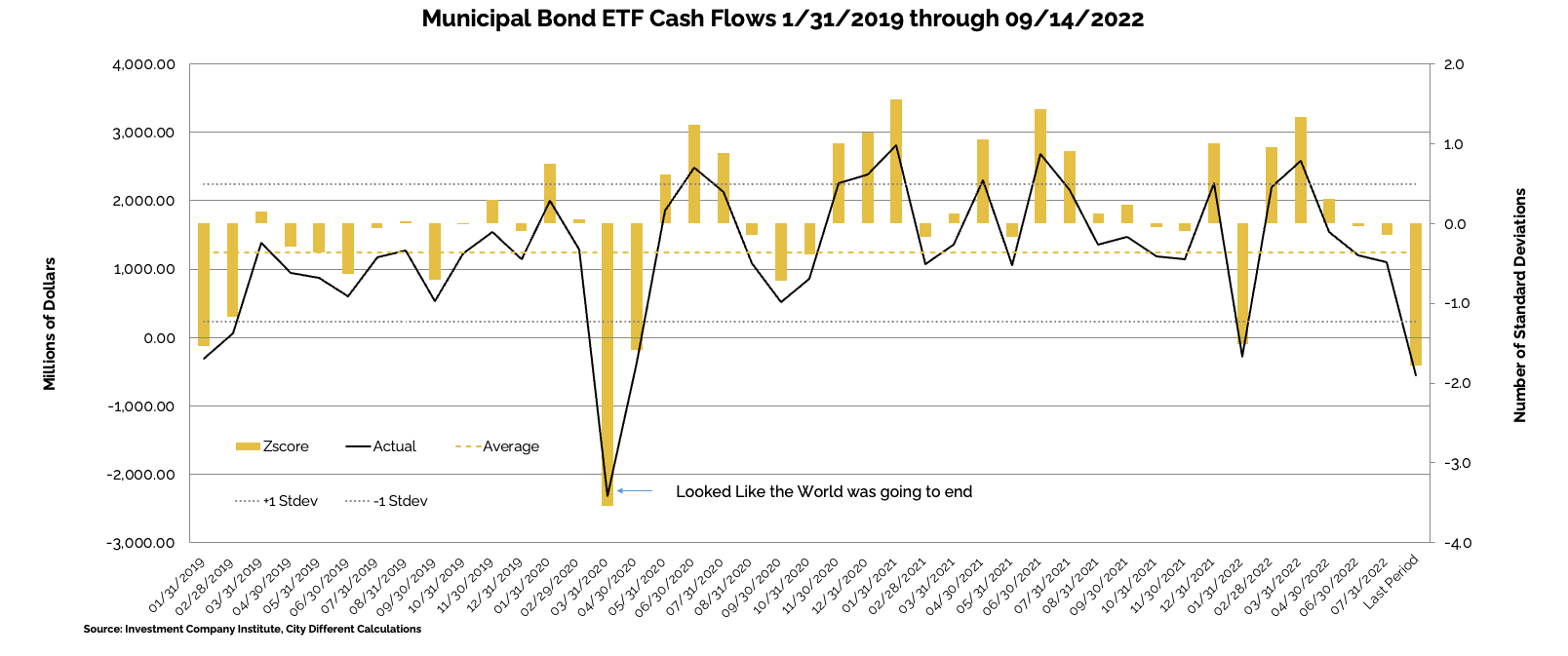

WHY IS THE MUNICIPAL MARKET BEHAVING THIS WAY?

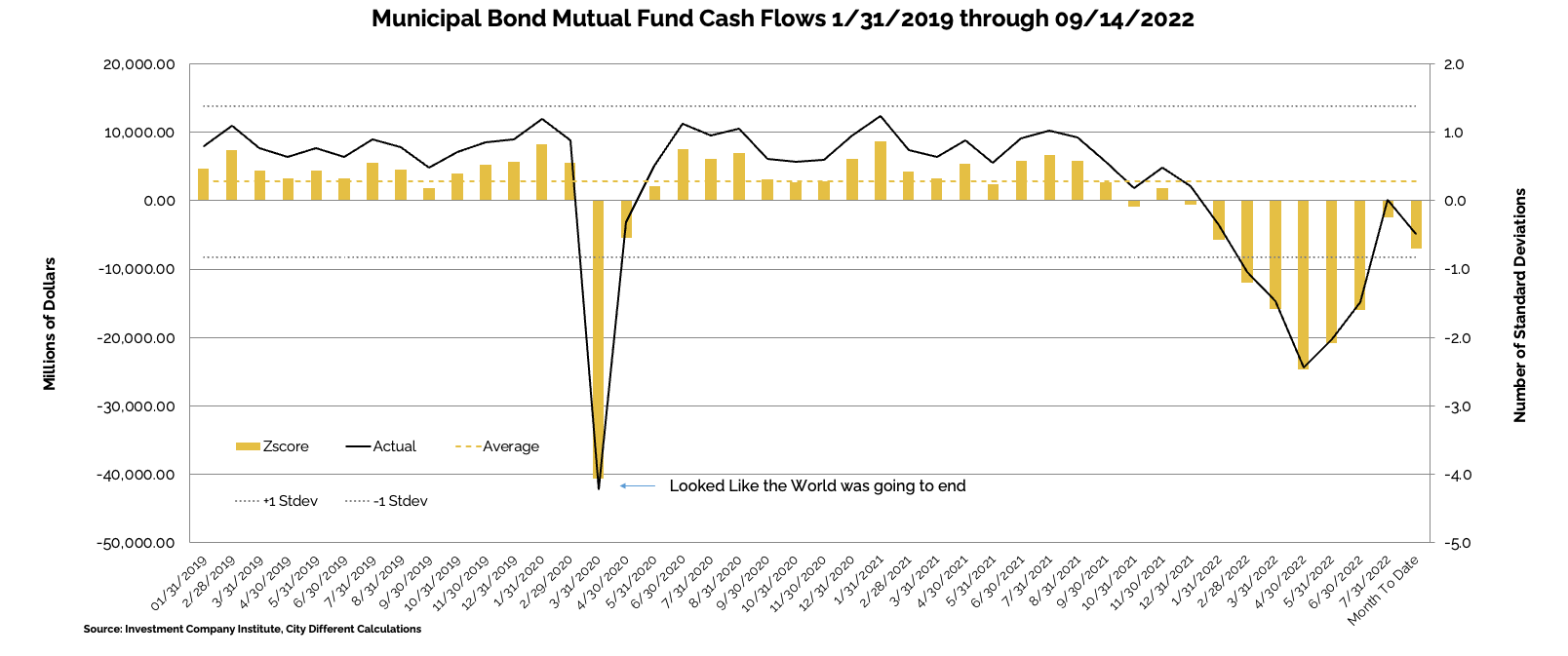

Various sources are used to report cash flows related to municipal bond mutual funds and ETFs, all reporting at different times. The source we have chosen to use is the Investment Company Institute (I.C.I.). The I.C.I. reported weekly cash flows from municipal bond mutual funds for the week of September 14, as -$1.7 billion compared to -$2.0 billion from the week before.

Municipal bond ETF cash flows for the same period were -$51 million, compared to +$130 million the prior week.

Other cash flow sources:

Lipper reported a 7th consecutive combined weekly and monthly outflow, with $2 billion leaving Muni funds for the period ending September 21, increasing the record YTD outflows to $87.9 billion.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

In its Municipal Markets Weekly newsletter, JP Morgan commented on the supply picture this week, stating that:

“Next week, we expect total supply of $7.5 billion, or 81% of the 5-year equivalent week average ($9.2 billion). We anticipate tax-exempt supply of $6.8 billion (111% of average), and taxable/corp cusip supply of just $0.7 billion (25% of average).”

The supply picture does not get interesting until it exceeds $10 billion tax-exempt issuances in a given week.

CORPORATE INVESTMENT GRADE AND HIGH YIELD OVERVIEW

In U.S. Investment Grade land, spreads widened slightly to reflect the pushback from the strong US CPI data.

In its weekly "Credit Flows" report, Wells Fargo commented:

"Targets. We continue to target credit spreads and prices of 200bps, 800bps and $89 for IG, HY and leveraged loans, respectively. While these are six-month targets we think they are reachable before the end of the year.

Powell’s Volcker moment, redux. With the rates market pricing 80bps of rate hike heading into today’s FOMC meeting, in order to stay true to Fed Chair Powell’s very hawkish message from Jackson Hole the Fed had to deliver either a 100bps or a hawkish 75bps hike — they chose the latter. This as the new dot plot indicates much higher year-end funds rates of 4.4%, 4.6% and 3.9% for 2022, 2023, 2024, respectively, (up from 3.4%, 3.8% and 3.4% in June). That implies another 125bps of hikes over the remaining two FOMC meetings of the year, which the market is pricing as 75bps in November and 50bps in December.

Fool me once, fool me twice… In fact Fed Chair Powell was so keen on making sure he didn’t make the usual mistake of coming off dovish during FOMC press conferences that he read a prepared message before answering one of the first questions — which was a risky one in this context about “how you'll know when to slow down the rate increases and when to stop?”. His statement began as follows: “My main message has not changed at all since Jackson Hole. The FOMC is resolved to bring inflation down and we will keep at it until the job is done”. This of course sends a strong signal that the Fed is happy about the reaction in markets since August 26 (until this morning stocks down 8% and 10-year Treasury yields 50bps higher) and also implicitly challenges investors that fight the Fed — which some did for a period of time during the presser as equities briefly rebounded before ending the day 1.7% lower (2.5% lower post FOMC).

Inflection point: 3Q earnings preview. The consequences of stubbornly high global inflation are finally set to make their mark on third quarter earnings results. Recent high profile warnings from companies — including FedEx, GE and Ford — make us think the 3Q earnings reporting season starting next month marks an inflection point toward sharply weaker corporate performance for non-financials. Consensus estimates for revenue and earnings growth of IG companies is 6.5% and 3.5% YoY, respectively, but have been revised lower by 1% and 3% since 2Q. For HY, the expected revenue and earnings growth rates for 3Q22 are 9.0% and 3.0%, respectively, down 1.3% and 3.9% since June. Even so, we do not think the risks of material earnings weakness are nearly priced into credit spreads, meaning we would be set up for heightened vol and positioned short heading into earnings season."

CONCLUSION

Compound interest is the largest component of total return, given a long enough investment horizon. Understanding an investor’s time horizon is a key element in building a well-diversified investment portfolio. Now might be a good time to reevaluate your time horizon. Once that is done, move cautiously in any type of rebalancing. Remember, time can bail out previously suboptimal investment decisions.

.png?width=500&name=signature%20block%20(3).png)

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.