.png)

WEEK ENDING 9/22/2023

- Fed reinforces “higher for longer.”

- Out with the new normal, in with the old.

- The House is burning.

A CITY DIFFERENT TAKE

The Federal Reserve chose to pause its rate-hiking strategy yet again. The fixed-income and equity markets took the statement and Chair Powell’s news conference as a bearish indicator.

Higher short-term interest rate policies were the rule of the day; this should have been no surprise as Chair Powell has been consistent with this message. On September 1, the market was forecasting one more increase in short-term rates (with a 31% probability for November) and a high probability of cuts in 2024. By September 22, that forecast had changed to a 20–27% probability of an increase in both November and December of 2023 with much lower probabilities of cuts in 2024. Of course, all bets are off if the “higher for longer” rate policy breaks something. (Think of an incident worse than the SVB collapse.)

The fixed-income markets reaction caused us to do a little research, which we will publish shortly. (Look for “Welcome to the Old Normal” soon.) Our conclusions were not earth-shaking for those of us with more gray hair than we care to admit. Basically, all the markets are enduring a return to the “old normal,” recovering from emergency policies taken by the Fed to combat two existential economic traumas (the 2008 financial crisis and the 2020 pandemic).

We pass no judgment if those policy reactions were good or not because the counterfactual is hard to prove and even worse to contemplate. These have caused a spike in inflation and an economy less sensitive to short-term interest rates. We suspect that the aging of the “boomer” generation has had an impact on the employment picture, but we have seen no research to support or refute this theory. The only support we can muster is that this demographic “pig in a python” has changed everything as it has passed through its life cycle. The last 15 years were not normal. They were an anomaly. Beware of recency bias.

CHANGES IN RATES

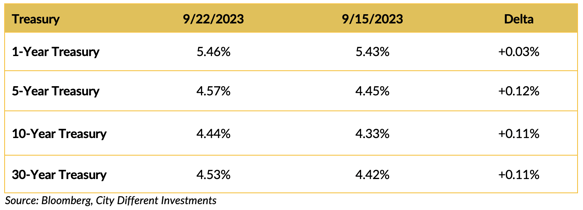

Treasury yields were higher on the week. The reaction to the Fed’s Wednesday announcement was quite stark. The spread between the two-year and 10-year Treasury securities was -0.66%, a little less negative than last week's -0.69%.

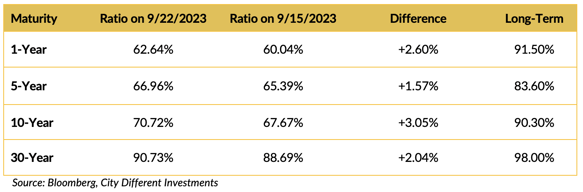

The municipal bond market played a little catch-up last week, increasing yield by more than the Treasury market. This is probably in anticipation of a growing new-issue calendar and investors moving money into money market funds. Open-ended municipal bond mutual funds have lost $16 billion of cash flows in 2023. Money market fund yields are attractive, but it takes two elements to ensure a superior total return: attractive yield and time. Yields must be durable over time. With about a 20-day average maturity, money markets have a high degree of reinvestment risk.

After playing catch-up, the municipal/Treasury ratios cheapened across the board.

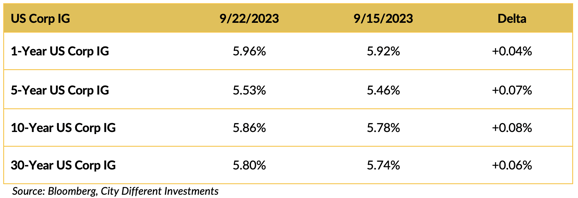

Corporate yields moved higher last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

As of this writing, we are about one week away from a government shutdown. Speaker McCarthy has sent the House home for the long weekend. It seems Abraham Lincoln was right with his “house divided” speech. The slim majority in the House of Representatives is fraying over spending plans.

“The Republican leader slammed his far-right flank for wanting to ‘burn the place down,’ after conservatives dramatically bucked McCarthy and GOP leadership on a procedural vote over a Pentagon funding bill, throwing the House into total paralysis. And now, members are not set to return to session until Tuesday as the possibility of a shutdown at the end of next week appears ever more likely.” The House is Burning.

The Speaker of the House was not the only Republican showing frustration. Rep. Mike Lawler (R-NY) showed his frustration with his more radical colleagues last week:

“‘If the clown show of colleagues that refuse to actually govern doesn’t want to pass the CR, I will do everything we need to make sure that a CR passes,’ Lawler said.”

We are glad he used the “clown show” line, so we didn’t have to. We have gone through a couple of government shutdowns in the past with no long-term ramifications. But that doesn’t mean we’ll always be so lucky.

President Biden addressed the United Nations last week. He also met with Ukrainian President Zelenskyy, announcing more Ukrainian support (though on a smaller scale). Support for Ukraine seems to be slipping with Republicans in Washington. Speaker McCarthy denied Zelenskyy’s request to address a joint session of Congress. Again, the counterfactual is hard to prove but even scarier to contemplate. If we are playing “chess” on a global scale, we must ask ourselves the following questions:

- What does waning U.S. support mean for our country’s stature in NATO and on the world stage?

- What does Russian success in Ukraine mean for Europe?

- Does waning U.S. support for Ukraine embolden China and its plans for Taiwan?

As we said, it’s scarier to contemplate.

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.45%, two basis points higher than the September 15 close of 2.43%. The 10-year Breakeven Inflation Rate finished the week at 2.37%, 2 basis points higher than the September 15 close.

Is the 5-year Breakeven Inflation Rate worth anything?

We have noted the difference between this measure and CORE PCE for some time. The 5-year Breakeven Inflation Rate is the market’s current estimate of the average inflation rate for the next five years. We took some time to look at this measure for the periods from 2/16/2016 through 8/31/2018. This is a small sample, but it is all we have. The average difference between this measure and the 5-year average CORE PCE measure is 0.23%. The maximum difference is 0.76%. And the minimum difference is -0.28%. The standard deviation of this analysis is 0.32%.

Our analysis is the sample size is too small to judge, but the 5-year Breakeven Inflation Rate’s value as an inflation forecast (unless used for hedging calculations) is suspect.

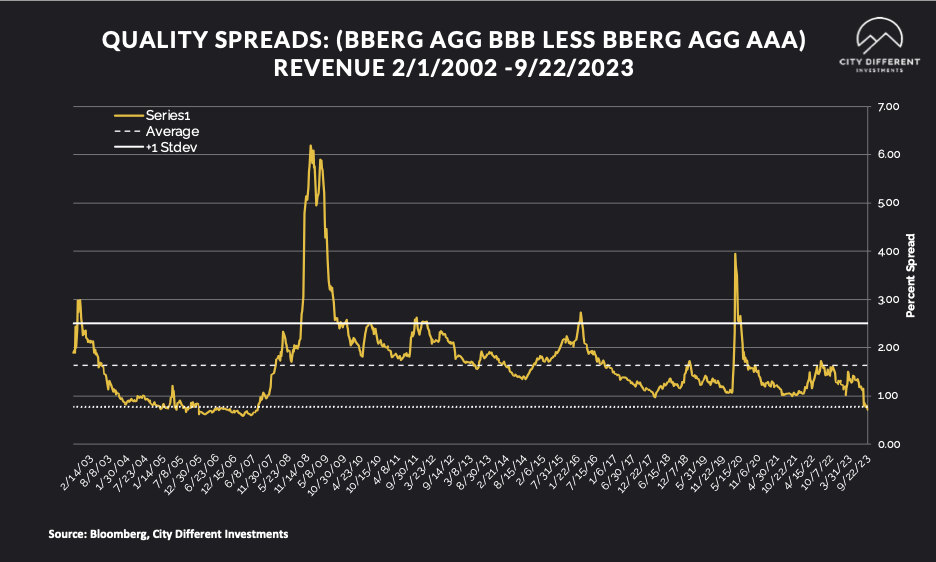

MUNICIPAL CREDIT

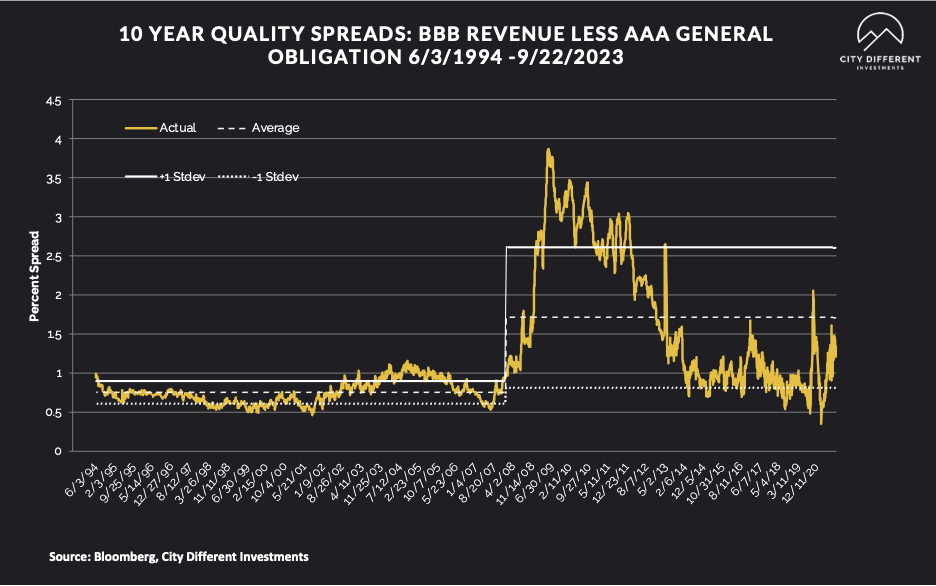

10-year quality spreads (AAA vs. BBB) as of September 22 was 1.20%, one basis point lower from the September 15 reading of 1.21% (based on our calculations). The long-term average is 1.71%. By our way of thinking, we still think lower-quality securities are not attractive. Municipal market credit spreads usually take a little more to adjust, given a significant baseline market revaluation.

Quality spreads in the taxable market are not attractive but were narrower last week, ending the week at 0.71%. The shift in street thinking from an imminent recession to one of a soft landing or no landing for the economy should be a factor.

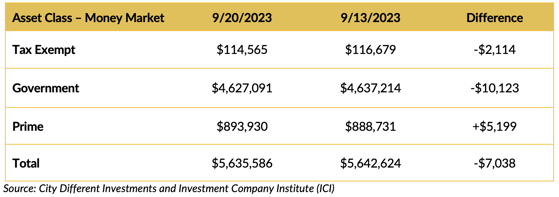

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money funds, in total, saw negative cash flows across two of the three subcategories last week.

Mutual Fund Flows (millions of dollars)

Bond mutual funds cash flows were mostly negative except for high-yield funds.

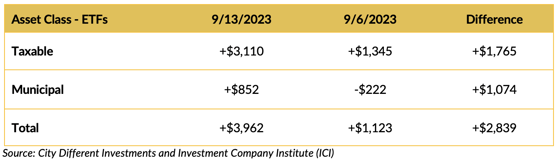

ETF Fund Flows (millions of dollars)

Investors look like they have an appetite for bond ETFs, at least they did last week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $7 billion.

CONCLUSION

Rates are moving higher; the yield curve is still inverted. We think that this environment is conducive for investors to buy bonds. Investors still must be careful about the duration risk they take on, but investments in the 1-to-10-year space seem attractive, especially compared to two years ago.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.