.png)

WEEK ENDING 9/15/2023

- A Fed meeting this Wednesday, but all eyes are on 2024.

- Brent crude prices could make for a scary Halloween.

- Is the US economy on a path to a soft landing?

A CITY DIFFERENT TAKE

FOMC meets this Wednesday. According to the markets, there is a nearly 100% probability of a hawkish hold. Key takeaways of Wednesday’s meeting will be Jerome Powell’s tone and a new dot plot. Currently, there is a 40% chance of another hike by the end of the year. Remember, this is a data-dependent Federal Reserve. Core PCE, employment numbers, and growth for the economy remain key data that the Fed continues to monitor.

The current Fed policy range is between 5.25% and 5.5%, with perhaps another 25 basis points in play for this year based on the summary of economic projections. The bigger question is how 2024 will play out with regard to rate cuts. Economists and Federal Fund futures have been pricing in several rate cuts next year. In June, the Federal Reserve dot plot had projected 1 percentage point of rate cuts.

Rate cuts for next year are dependent on data showing lower inflation. We believe this is pure speculation at this point. We continue to be in the camp of “higher for longer” until data shows otherwise.

Brent crude is currently spiking at $95 a barrel. The last time Brent prices were this high was the fourth quarter of 2022. One of the reasons for recent high pricing is supply cuts by Saudi Arabia and Russia. In addition, there is demand from China’s pressure to reopen. Remember, Core PCE does not include energy prices. But if energy prices stay high for long enough, they start to impact Core Inflation. Analysts are predicting a triple-digit price for Brent crude by Halloween.

Finally, The Wall Street Journal published a piece exploring the possibility of a soft landing. The Fed has achieved a soft landing only once in history: the mid ‘90s. But one cannot draw on history to get the rates cycle right. Every cycle is unique. In 1994–96, for example, inflation was already low, unlike now, where the Fed's goal is to lower inflation.

CHANGES IN RATES

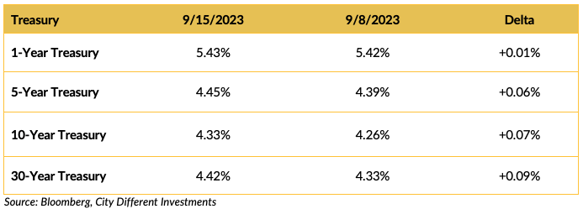

Treasury yields were moderately higher on the week, given the release of the latest CPI and PPI readings. Each demonstrated that the Fed’s 2% inflation target may prove elusive — close to unchanged, point to point, over the last two weeks. The “Bear Steepener” continues to drip. The spread between two-year and ten-year Treasury securities is -0.69% versus last week’s -0.72%.

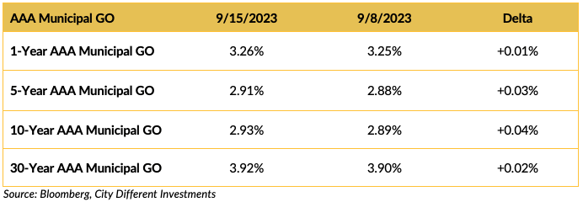

Municipal yields were higher on the week. A lack of new issuance supply led to the outperformance of the municipal market last week. Next week’s estimated $5 billion in supply will support continued relative outperformance.

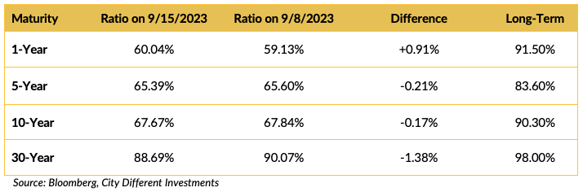

Municipals richened slightly versus Treasuries in all but the one-year maturity range. We anticipate that to change in the next few weeks.

Yields in the investment grade (IG) corporate market were mixed. The U.S. Corp. Investment Grade yield curve steepened.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Congress has not passed appropriations for the 2024 budget. Republicans crafted a short-term bill, that includes spending cuts and border security provisions, which are already drawing protest. Congress must pass a continuing resolution by September 30th to keep the government operating past September. Tick tock goes the clock…

McCarthy now has to keep the promises he made to secure his position, which is proving problematic. Part of those promises include the recent impeachment investigation into President Joe Biden.

The summer of strikes continues, with Auto Workers going on strike last week. There is no real material movement in the negotiations as of yet.

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.43%, 3 basis points higher than the September 8 close of 2.40%. The 10-year Breakeven Inflation Rate finished the week at 2.35%, 2 basis points higher than last week’s close.

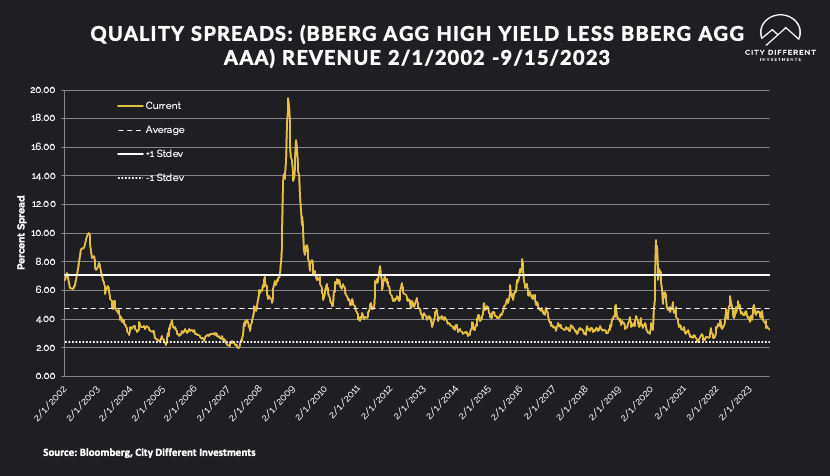

MUNICIPAL CREDIT

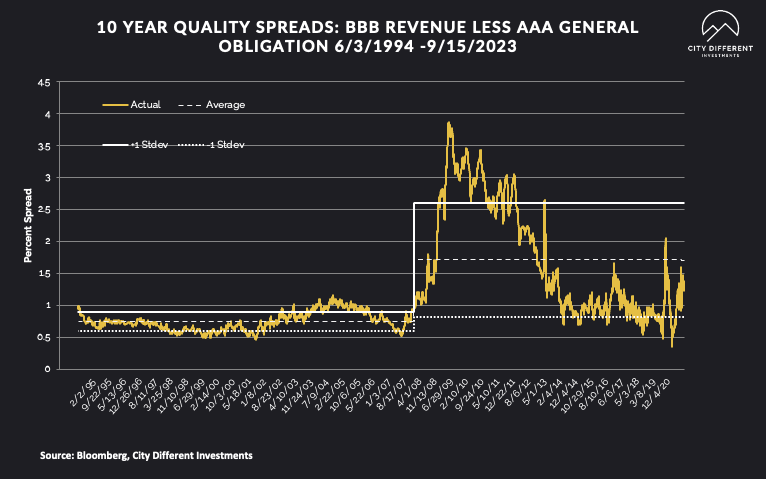

10-year quality spreads (AAA vs. BBB) as of September 15 were 1.23%, 11 basis points lower than the September 8 reading of 1.34% (based on our calculations). The long-term average is 1.71%. By our way of thinking, we still believe lower-quality securities are not attractive.

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 0.79%. The shift in street thinking from an imminent recession to one of a soft landing or no landing for the economy should be a factor.

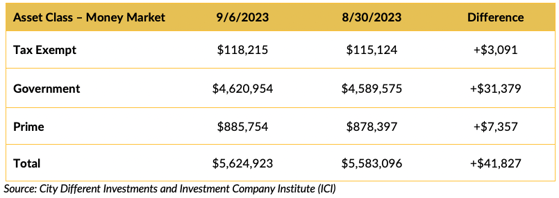

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money funds, in total, saw increased cash flows across three of the four categories last week. Money market yields are attractive, but how long will that last? Beware of the cash trap.

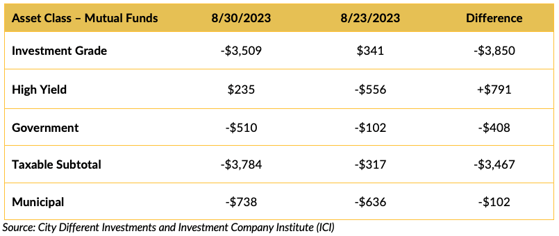

Mutual Fund Flows (millions of dollars)

Flows related to three of the four bond categories were negative. Only government bond funds saw positive flows.

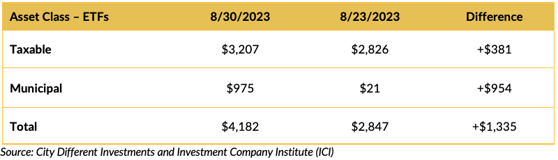

ETF Fund Flows (millions of dollars)

Investors didn't care for municipal bond ETFs last week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $5 billion.

CONCLUSION

There are many data releases scheduled from now to year-end for a data-dependent Federal Reserve. A hawkish rate hold for this September is a forgone conclusion. The bigger question revolves around rate cuts in 2024. Brent crude has gone back to record-breaking high prices. And in terms of recovery, the Fed has managed only one soft landing in its history.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.