.png)

WEEK ENDING 9/8/2023

Today is the 22nd anniversary of the Sept. 11 terrorist attacks; here are a few things we are thinking about today:

- This was the deadliest attack on U.S. soil in our nation’s history. The attacks killed nearly 3,000 people and injured more than 6,000 others.

- Remember the schoolmates, colleagues, and colleagues’ children lost that day.

- Remember the bravery of the first responders running into the flaming towers, the Pentagon to rescue those stranded, and the people on Flight 93 who brought it down well before its ultimate target. That is American patriotism!

A CITY DIFFERENT TAKE

There was a good deal of data released over the last two weeks that could possibly move the market. The fixed-income markets seemed to take it all in stride, however, and rates remained little changed over the period.

This week, we get to look forward to the nattering around a possible government shutdown. We are starting to feel like the villagers from “The Boy Who Cried Wolf.” The threats and actual government shutdowns are becoming passé. Let’s hope this one doesn’t eat our financial sheep.

We also have a potential United Auto Workers strike to look forward to this week. Their demands include:

- A 40% wage hike over four years (amounting to 46% compounded).

- Cost-of-living increases.

- Beefed-up retirement benefits.

- A shortened 32-hour work week. Nice work if you can get it.

When do the WIN buttons come out? The last time we heard of cost-of-living adjustments, President Ford tried to “whip inflation now.” Chris’s reaction to all of this is “I would like to be 25 again, 6’4”, 250 lbs. and cut — but only one of those things stands a chance of happening.”

CHANGES IN RATES

Treasury yields were close to unchanged, point to point, over the last two weeks. The “bear steepener” continues. The spread between two-year and ten-year Treasury securities is 0.72% versus two weeks ago at 0.78%.

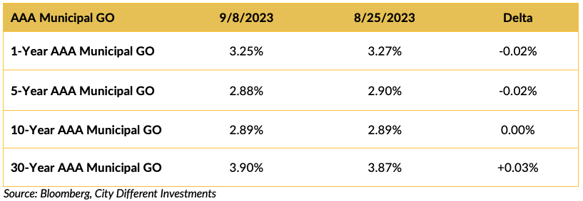

Municipal yields went nowhere over the last two weeks, point to point.

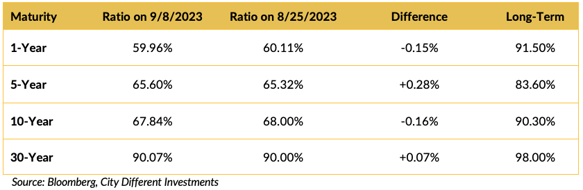

There was no significant change in the relative value of AAA General Obligation Municipal bonds over the two-week period. We anticipate that to change in the next few weeks.

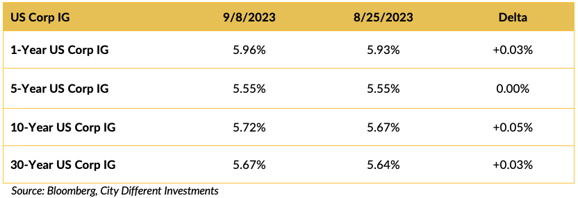

Yields in the investment grade (IG) corporate market followed the Treasury market pattern.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Congress is coming back to town, which means trouble must be right around the corner. The U.S. government could shut down at midnight on September 30 if Congress fails to pass spending legislation. Stopgap measures would avoid this outcome, but far-right representatives in the House wish to attach conditions to any solution. Those conditions include crackdowns on undocumented immigration and a vote on a presidential impeachment inquiry. A shutdown would put hundreds of thousands of federal workers on furlough without pay and lead to numerous service disruptions impacting the American public.

Earlier, we mentioned American patriotism. This must be the opposite of that. At least with Congress back, this part of the commentary will be more interesting to write.

Other notable political headlines include:

- On the world stage, President Biden secured deals with Vietnam on semiconductors and minerals as the strategic Southeast Asian Nation lifted Washington to Hanoi’s highest diplomatic status alongside China and Russia. This should help secure supply chains from China-related risks.

- “Presidential candidate says he would deport US-born children of undocumented migrants along with their parents.” So much for a bright city on the hill.

- Tuberville has been holding up 300+ military promotions since March over the Pentagon’s abortion policy. He’s now claiming poetry is an example of the “wokeness” that is causing a decline in our military.

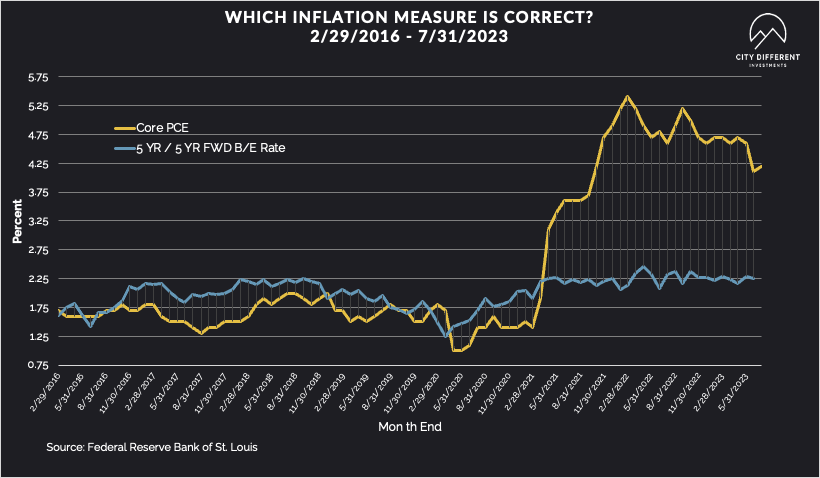

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.40%, slightly lower than the August 25 close of 2.41%. The 10-year Breakeven Inflation Rate finished the week at 2.33%, unchanged from the August 25 close.

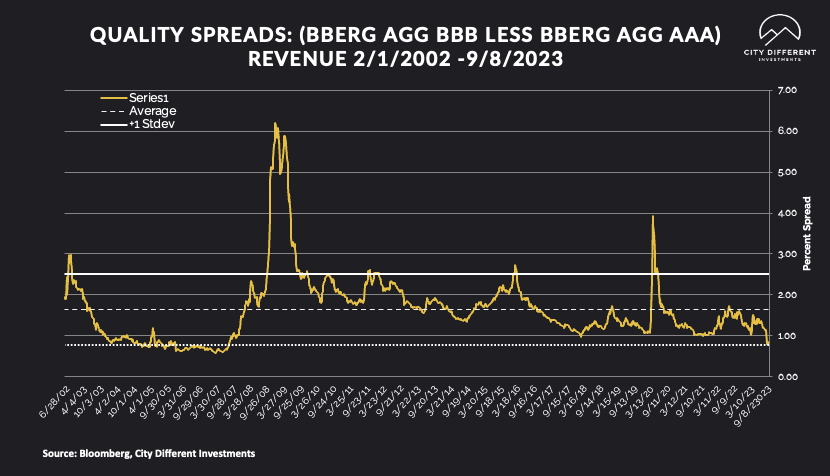

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of September 8 was 1.34%, unchanged from the August 25 reading of 1.34% (based on our calculations). The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 0.79%. The shift in street thinking from an imminent recession to one of a soft landing or no landing for the economy should be a factor.

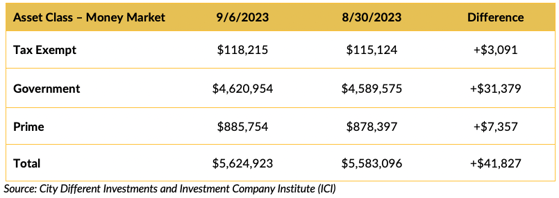

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money funds, in total, saw positive cash flows across all categories last week. We know we are sounding like a broken record (or maybe a corrupted MP3 file). Money market yields are attractive, but how long will that last? Beware of the cash trap.

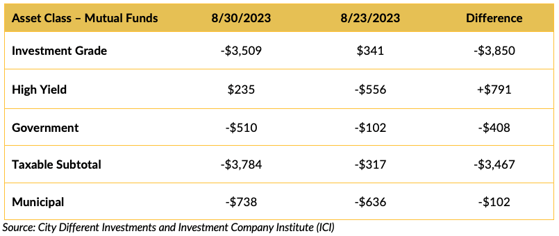

Mutual Fund Flows (millions of dollars)

Few folks liked bonds last week unless you were a high-yield bond. More evidence of a changing outlook for the economy.

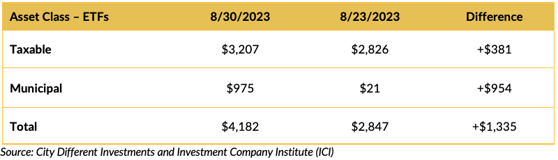

ETF Fund Flows (millions of dollars)

Investors liked Bond ETFs last week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $7 billion.

CONCLUSION

Activity in the fixed-income markets should begin to pick up now that the Labor Day holiday is behind us.

The yield curve is still flat but there are signs of a “bear steepener” taking hold. Street prognosticators are changing their outlooks from a recession being right around the corner to a soft-landing or “no landing” in the offing. We’re not sure we agree. We expect to extend the durations in our fixed-income accounts to the top end of their neutral range but would wait until the relative yield curves achieve their normal shape to move durations any higher.

We also feel that quality spreads reflect the street’s change in opinion and therefore lower-quality bonds are not a value yet. Yields on money market funds are attractive to investors but we feel they are falling prey to a “cash trap.” Money market funds have a very short average maturity (about 20 days in some cases). When short-term rates eventually fall, those yields evaporate very quickly.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.