.png)

WEEK ENDING 8/4/2023

Highlights of the week:

- U.S. Government Bond rating downgraded to AA+ by Fitch — a tempest in a teapot.

- Treasury rates increased but not because of the downgrade.

- Former President Trump arraigned for the third time this year.

A CITY DIFFERENT TAKE

Last week was a wild ride for fixed-income markets of all kinds. Fitch downgraded the long-term credit rating of the United States from AAA to AA+. The U.S. is now rated AAA/AA+/AA+. We do not think this action is a big deal. We share Warren Buffet’s and Jamie Dimon’s views of the event. Fitch cited three reasons for the downgrade:

- Fiscal deterioration over the next three years

- High and growing general government debt burden

- Erosion of governance

Long-maturity Treasury bonds increased in yield most of the week before tapering their increases Friday on the back of some tepid economic numbers. Over the weekend, the Wall Street Journal published an article that cited three reasons for the sudden increase in rates:

- Strong economic data

- Added pressure from the Bank of Japan

- The U.S. Treasury announcing it faces greater borrowing needs in the coming months

Nowhere in this article did they mention the downgrade of the U.S. debt rating as a cause for the increase in rates.

Other publications like Bloomberg shed more color on the increased borrowings, “Benchmark 10-year yields rose to the highest level since November after the Treasury said it will sell $103 billion of longer-term securities at its so-called quarterly refunding auctions next week.” Those rumors seem to be enough to send a chill up the spines of fixed-income traders.

Friday’s nonfarm payroll numbers showed an employment increase of 187,000 (below estimates of 200,000). The unemployment rate slipped to 3.5% from 3.6%. Year-over-year average hourly earnings were higher than expected (4.4% vs 4.2%). Given the increase in nonfarm productivity (3.7% vs. 2.2%) and the slowdown in year-over-year unit labor costs (1.6% vs. 2.5%), taken as a whole, these numbers support the soft-landing thesis. We, however, are not firmly convinced this is the correct conclusion.

We think the most significant driver of last week’s higher rates was the Treasury's announcement of increased borrowing needs.

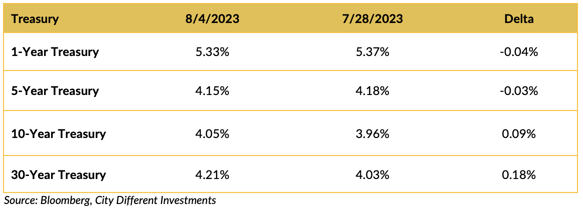

CHANGES IN RATES

Yields on long-maturity Treasury bonds moved higher last week, while the yield on short-maturity Treasury securities was marginally lower. This phenomenon is known as a “bear steepener” across the board. The spread between two-year and ten-year Treasury security yields finished the week at 0.73%.

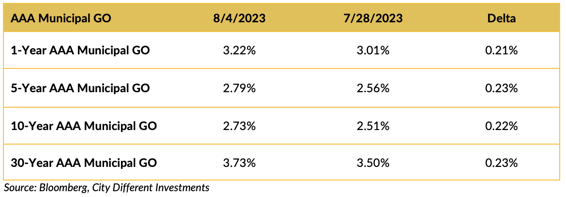

Municipal yields also moved higher last week across the curve and at a higher rate than the Treasury. We think that the rise in yield levels was fed by initial relative rich ratio levels to the Treasury, supply fears in the Treasury market, and high levels of new issue supply in the municipal market.

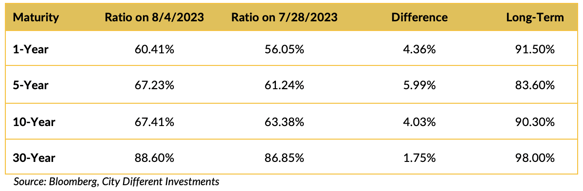

Relative values can change rapidly and with little warning, as they did last week. Muni/Treasury ratios are higher but still below the long-term averages.

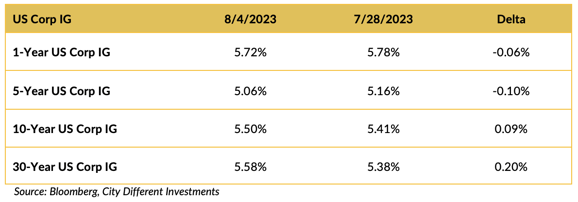

Yields in the investment grade (IG) corporate market followed the Treasury market’s pattern.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Congress is on its summer recess. (Thank God, except this section is now harder to write!)

As we shared earlier, the United States was downgraded by Fitch last week. Of the three reasons given, we find the “erosion of governance” to be the most concerning. Especially considering the potential for a conflict over a government shutdown in September.

Oh yeah, former President Trump was arraigned for the third time this year. It is getting to be old hat, with at least one more on the horizon. Erosion, indeed.

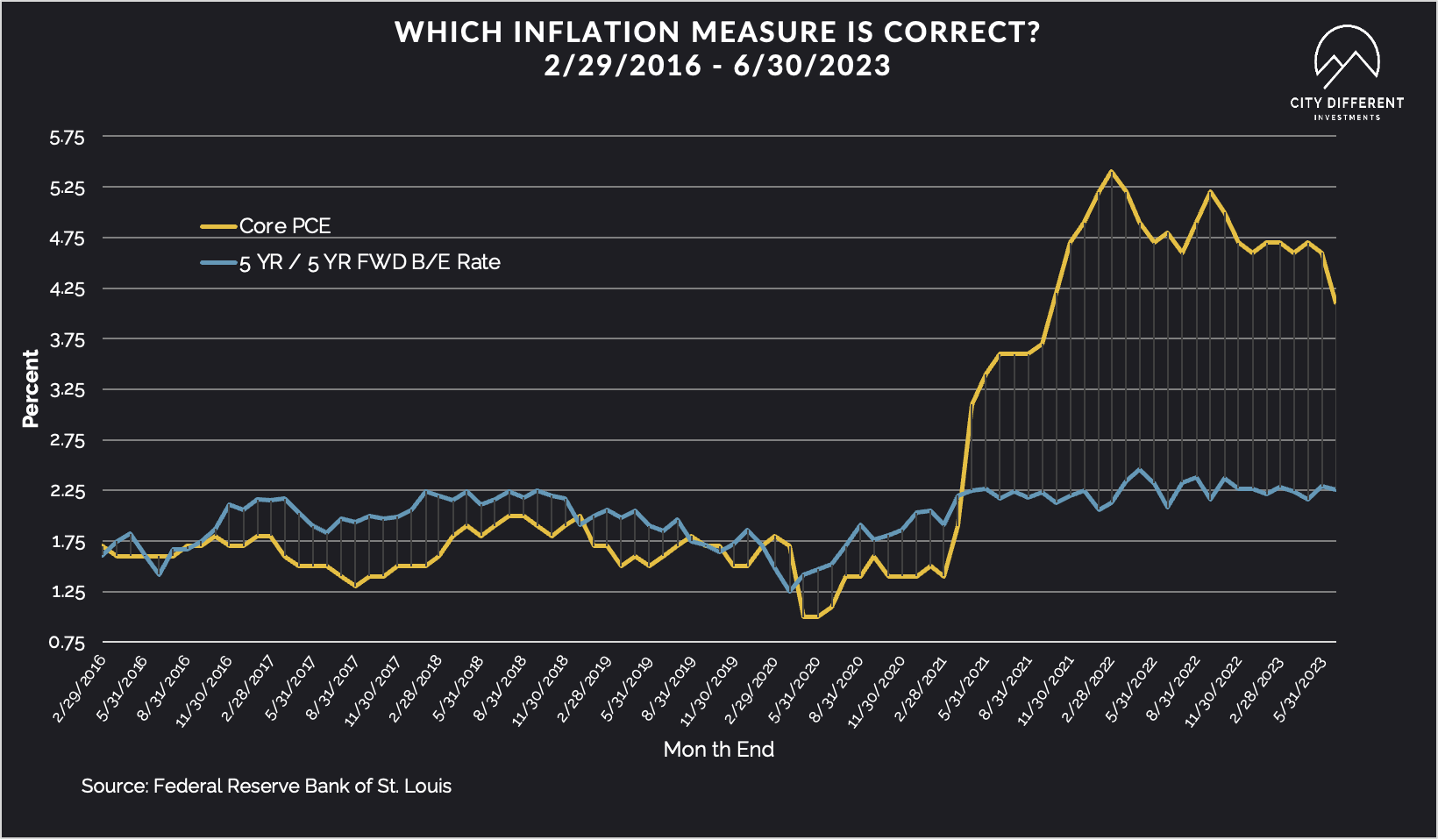

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.50%, a 2-basis point increase over the July 28 close of 2.48%. The 10-year Breakeven Inflation Rate finished the week at 2.38%, unchanged from the July 21 close.

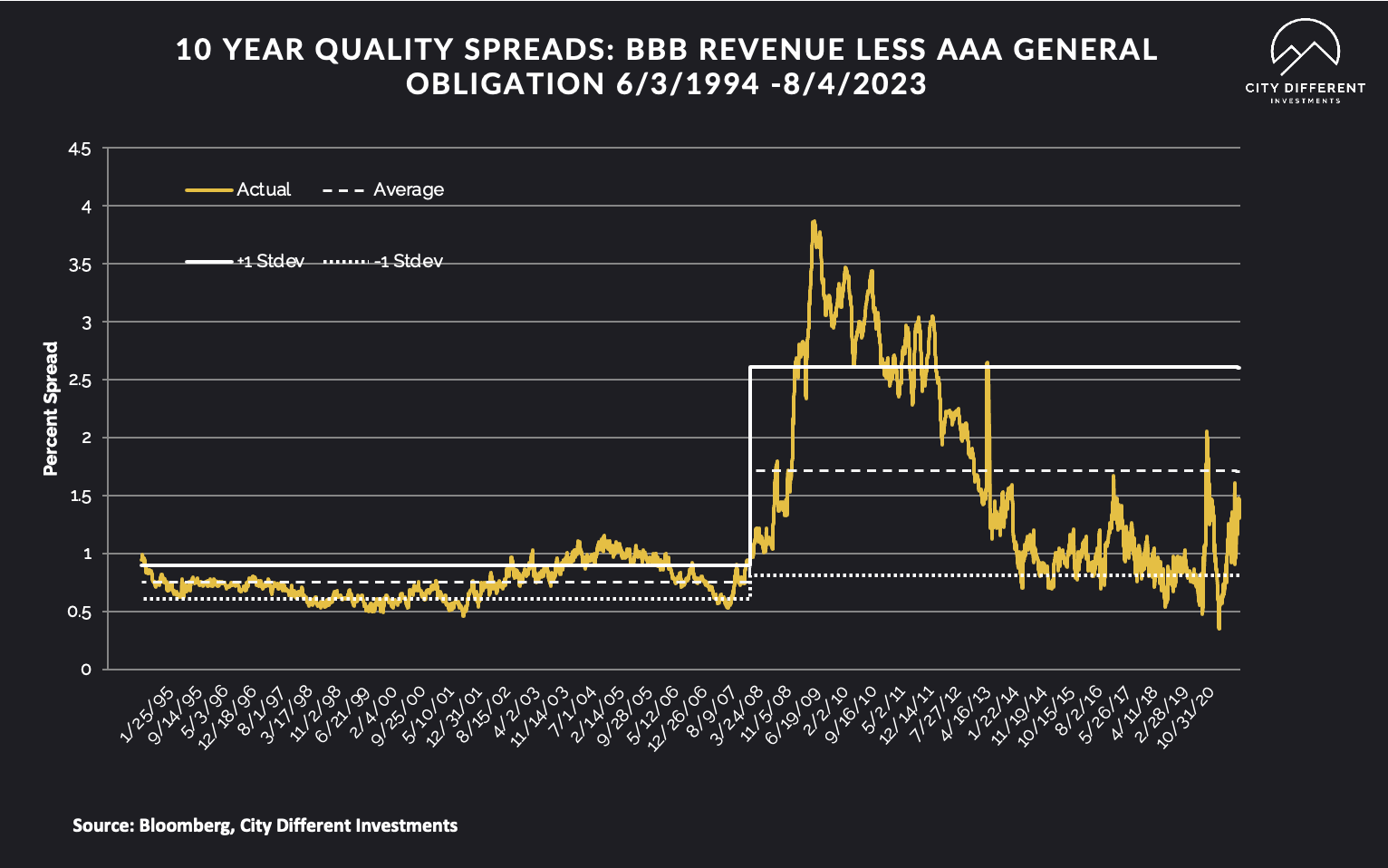

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of August 4 was 1.36% (based on our calculations), 0.05% lower than the July 28 close of 1.41%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

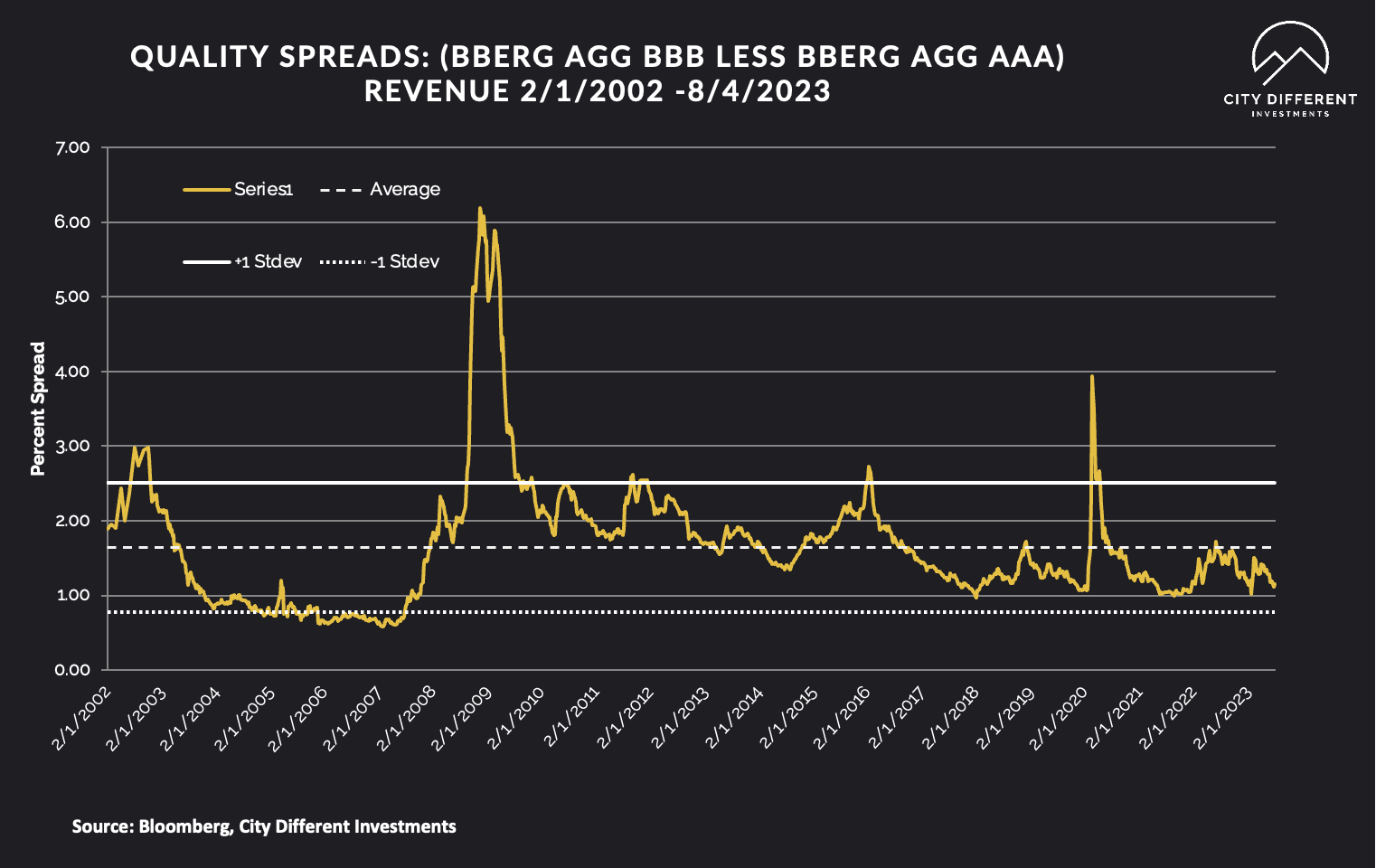

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 1.15%.

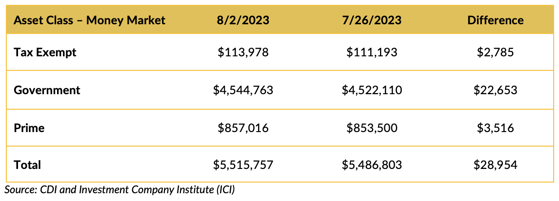

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

All money fund categories saw positive cash flows last week. Money market yields are attractive, but how long will that last? If you would like our view on this issue, please reach out to Sweta or Chris.

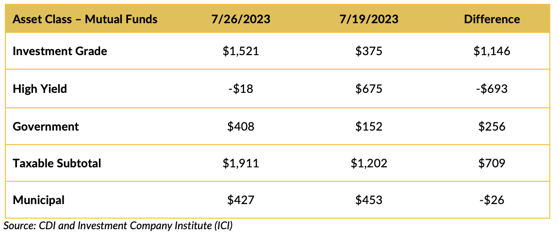

Mutual Fund Flows (millions of dollars)

Flows into bond funds are positive for the week and up from the week prior.

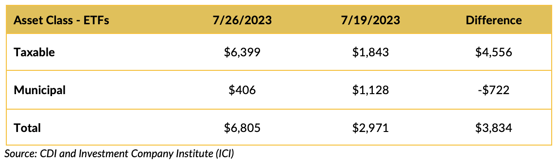

ETF Fund Flows (millions of dollars)

Bond ETFs also saw positive cash flows.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply is slated for somewhere around a moderate $7 billion. This should be manageable.

CONCLUSION

Supply scares, the Street is falling in line with the soft-landing forecast, and a U.S. credit downgrade. We cannot wait to see what Chair Powell pulls out of his hat at Jackson Hole.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.