.png)

WEEK ENDING 8/11/2023

Highlights of the week:

- Inflation data mixed, with expectations of the Fed being on hold in September

- Treasury continues to bring big supply to the market

- China has a liquidity problem

A CITY DIFFERENT TAKE

Inflation data was largely unchanged last week, despite last Thursday’s Consumer Price Index or CPI showing that Core Inflation rose by 0.2%. This was the smallest consecutive monthly increase in the last two years. Warning, there Is another CPI release to come out before the Fed's September meeting. Even though food and energy are stripped out of Core, we are seeing an increase in non-Core prices. This was followed by the Producer Price Index or PPI release on Friday, showing that PPI rose by 0.3% In July, which was more than expected.

What does this mean for the markets? Currently, Fed fund futures are showing rates to largely be on hold for the September meeting, with only an 11% probability for a 25-basis point increase, and a 25% chance of an additional rate rise In November.

What about guidance from the Fed itself? We think this is going to be tricky now that the Federal Reserve is in restrictive territory. Last week we saw conflicting language from various Fed officials; Mary Daly of the San Francisco Fed and Governor Miki Bowman seem to be advising for additional rate hikes, while NY Fed President John Williams and Philly Fed President Pat Harker are advocating a hold policy.

The other theme continues to be mega issuance by the Treasury. Last week we saw $103 Billion in treasury auctions for 3, 10, and 30-year bonds. We continue to expect a larger treasury supply to fund the budget deficit for the government.

Lastly, a quick mention of China's liquidity problem. China's economy has had a tough time rebounding back from Covid with two issues in particular. One is the property market. Country Garden, the Chinese property developer, has suspended trading and is asking creditors for extensions. Second, China's wealth manager, Zhongzhi Enterprise Group Co, has missed several payments on its high-yield debt. They are the largest player in China's $2.9 trillion dollar trust industry.

CHANGES IN RATES

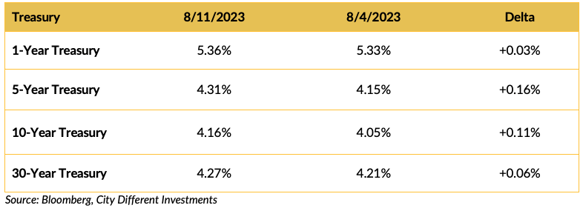

Treasury yields continued to move higher in spite of some fix-income-friendly inflation data. The “bear steepener” was sustained. The spread between two-year and ten-year Treasury security yields finished the week at 0.73%

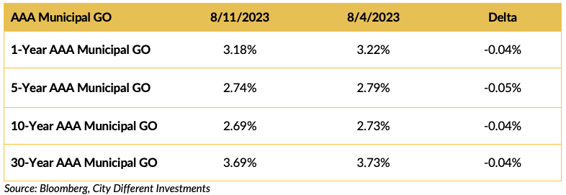

Municipal yields moved marginally lower last week across the curve. With the supply fears behind us, the municipal market exhibited a slight recovery.

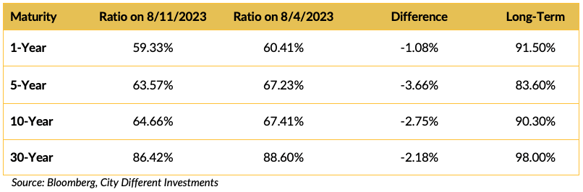

Relative values can change rapidly and with little warning, as they did last week. Muni/Treasury ratios are lower and well below the long-term averages.

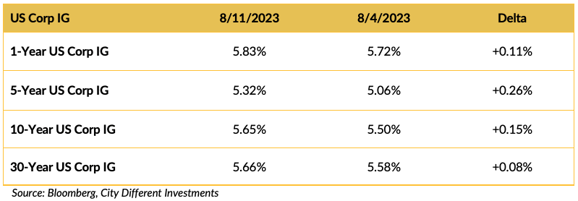

Yields in the investment grade (IG) corporate market followed the Treasury market pattern.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

As mentioned last week, Congress is still in recess therefore so is this section. We don’t have much to report from Washington. The next big Fed announcement will be coming out of next week's Jackson Hole symposium.

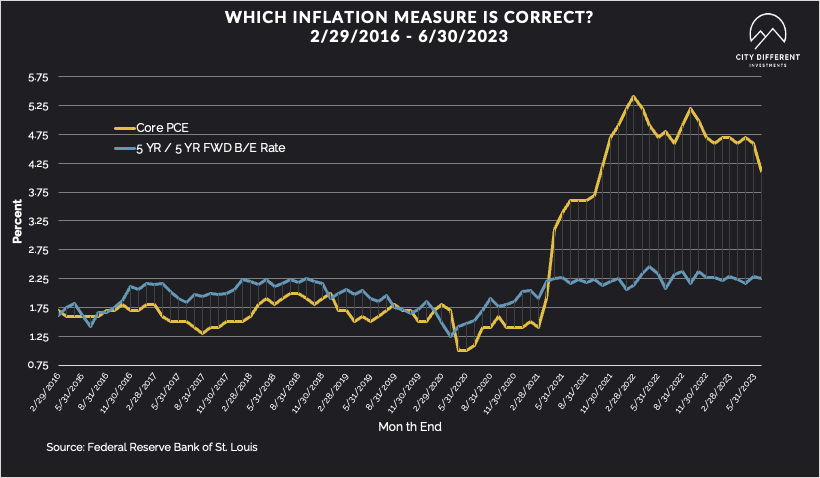

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.42%, an 8-basis point decrease over the 8/04/2023 close of 2.50%. The 10-year Breakeven Inflation Rate finished the week at 2.36%, a two-basis point decrease from the 8/4/2023 close.

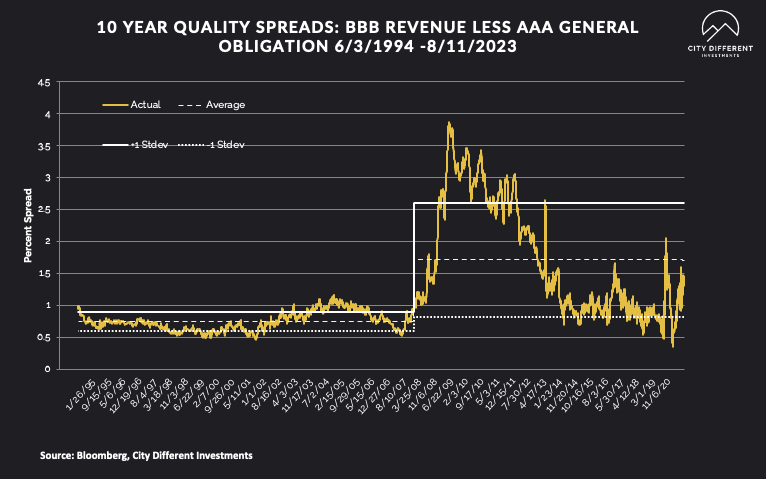

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of 8/11/2023 was 1.38% (based on our calculations), 0.02% higher than the 8/4/2023 close of 1.36%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

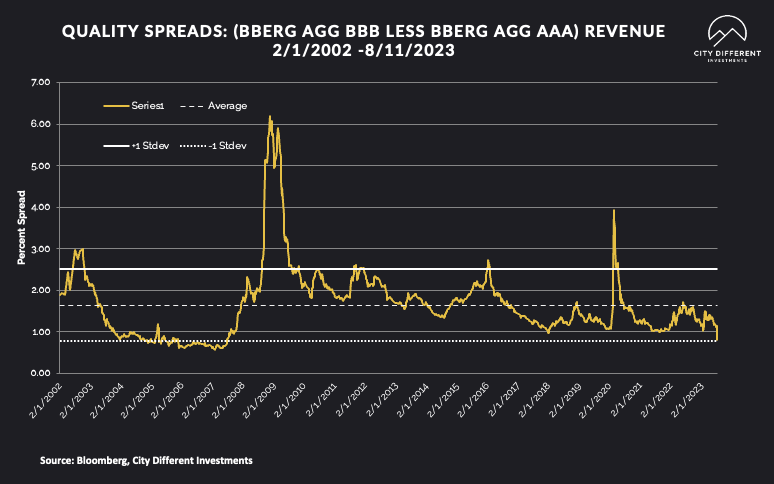

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 0.81%.

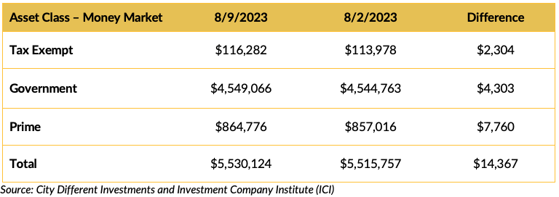

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

All money fund categories saw positive cash flows again last week. Money market yields are attractive, but how long will that last? If you would like our view on this issue, please reach out to us.

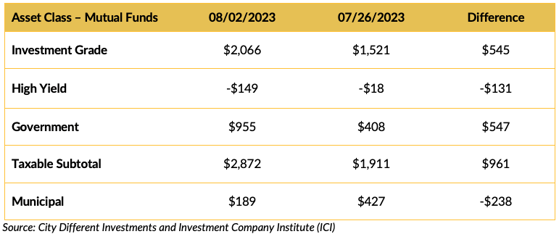

Mutual Fund Flows (millions of dollars)

Flows into bond funds are mixed for the week. It looks like municipal bond investors do not like higher yields.

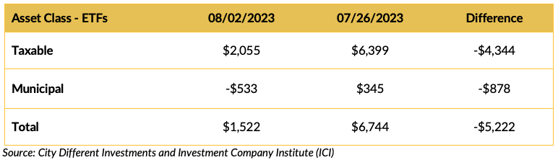

ETF Fund Flows (millions of dollars)

Bond ETFs were also mixed, with municipals recording a net outflow for the week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around a moderate $7 billion again. This should be manageable.

CONCLUSION

We think that the Fed is committed to its inflation mandate. July's CPI and PPI data were mixed; however, we do think that Fed is likely to hold in September. Treasury issuance remains robust to fund the federal deficit. China most certainly has a liquidity problem, with two of Its biggest firms asking creditors for an extension.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.