.png)

WEEK ENDING 8/25/2023

Highlights of the week:

- The rodeo came to Jackson Hole last week.

- Important economic data is hitting this week.

- China's stimulus fails to get investors excited.

A CITY DIFFERENT TAKE

Jackson Hole, Wyoming, again played host to central bankers last week. And, along with the media, the whole rodeo came to town.

After hearing Chair Jerome Powell speak on Friday, our takeaway is that the Federal Reserve is not messing around with its 2% inflation target. The meeting was an affirmation of the unequivocal 2% target. Not 3%. Not 3.5%. To that end, Powell outlined two monetary policies that the Fed could pursue.

The first is being “prepared to raise rates.” The second is to continue a restrictive policy. The market is hailing this as a hawkish tone from the Fed and is now factoring in a 50% chance of a rate increase in the November meeting. We would like to reiterate that easing has not been outlined by the Federal Reserve as an option.

The contradictory forces of “navigating by the stars under cloudy skies” remains a challenge for the Fed. Inflation in the super core also remains a challenge. U.S. GDP continues to grow and so does consumer spending. The housing market is showing signs of picking up as well.

As much as the market participants have been consumed by r-star (i.e. the real neutral rate of interest that equilibrates the economy in the long run), Powell refrained from addressing it directly. Doing so has been a big challenge for the Fed.

This is a data rich week, and the Fed will need to be data dependent for their upcoming meetings. Tuesday, we see August’s Consumer Confidence and July JOLTs numbers. ADP reporting comes out on Wednesday, along with a Q2 GDP revision. On Thursday, personal income, spending, and PCE will be available. But the real highlight of the week will be Friday’s August employment report, which kicks off the long holiday weekend.

Moving globally to China, investor confidence in the country has not been revived yet by the flurry of recent regulatory changes. The market needs to see some kind of fiscal confidence on a national level. The headwinds in China have been its property market and exports. In addition, China has seen weak consumer sentiments domestically. Foreign investors have been net sellers. Two different agencies have come out with easing measures. China is cutting its stamp duty. In addition, the securities regulator is going to put a moratorium on IPOs for now.

CHANGES IN RATES

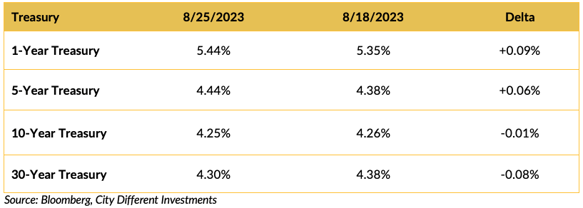

Treasury yields were stable last week; short-maturity yields moved higher, and long-maturity yields moved a little lower.

The “Bear Steepener” reversed slightly. The spread between two-year and ten-year Treasury security yields finished the week at 0.78%.

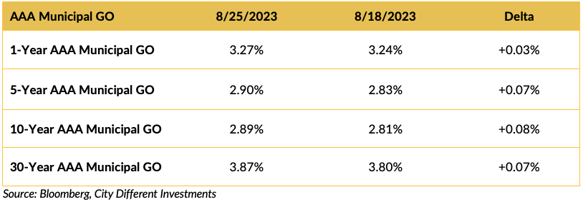

Municipal yields moved higher last week across the curve. The municipal market is still playing catchup with prior Treasury moves.

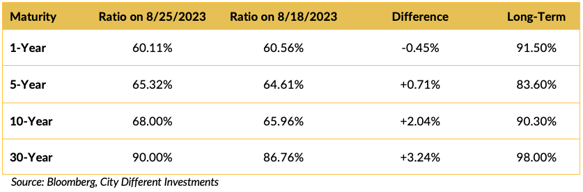

Relative values can change rapidly and with little warning, as they did last week. Muni/Treasury ratios are higher but still well below the long-term averages.

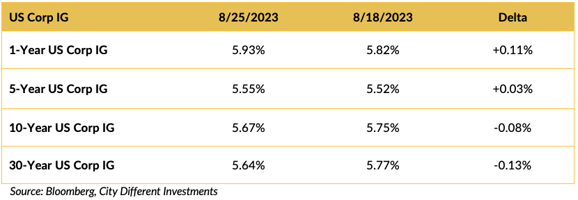

Yields in the investment grade (IG) corporate market followed the Treasury market pattern.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Last Thursday, for the fourth time this year, former President Trump turned himself in after criminal charges were filed against him. He will enter a plea to his 13 felony charges in Georgia on September 6, and the other 18 defendants in the Georgia election case will also be arraigned on that day.

The Rodeo may have been in Wyoming, but the Circus was in Milwaukee. The first of the Republican presidential primary debates took place last week, sans Trump. Eight candidates took the stage for a two-hour debate, which seemed like a lot of unnecessary competition for second place. One thing is for sure: we are not looking forward to a long campaign season.

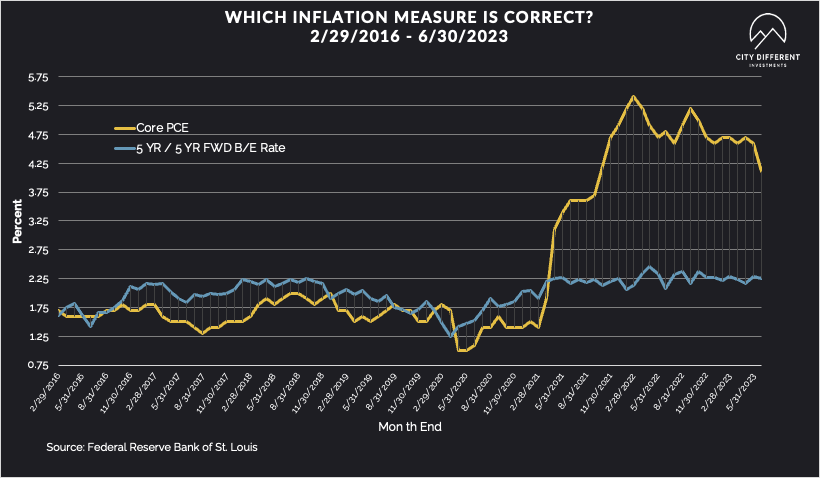

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.41%, one basis point lower than the August 18 close of 2.42%. The 10-year Breakeven Inflation Rate finished the week at 2.33%, a one-basis point decrease from the August 18 close.

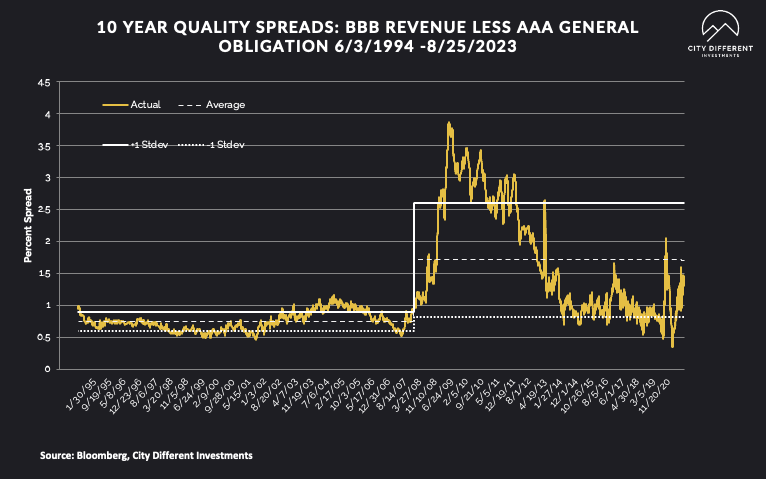

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of August 25 was 1.34% (based on our calculations), 4 basis points higher than the August 18 close of 1.30%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 0.77%.

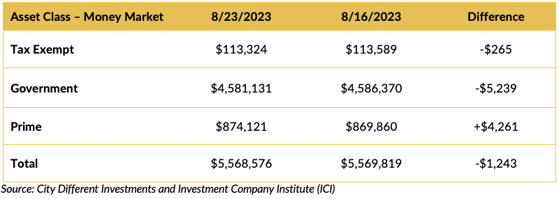

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money funds, in total, saw negative cash flows again last week. The first time in a long while. Money market yields are attractive, but how long will that last? See our thoughts on the subject in our latest blog on the issue.

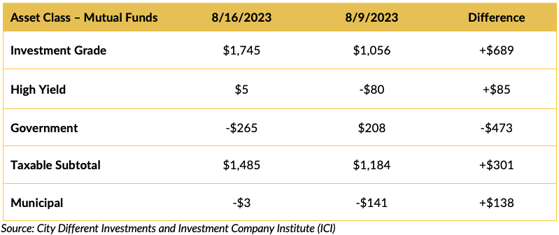

Mutual Fund Flows (millions of dollars)

Flows into bond funds are mixed for the week.

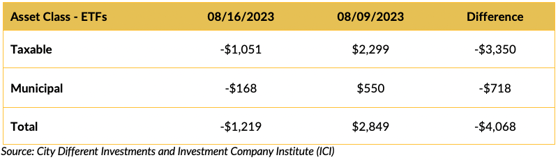

ETF Fund Flows (millions of dollars)

Bond ETFs showed both taxable and municipals recording net outflows for the week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $4 billion. The municipal market slows down before the holiday.

CONCLUSION

Chair Powell was direct in his support for the Fed’s 2% inflation target. To that end, this Fed is prepared to raise rates or remain restrictive. For ongoing meetings, the Federal Reserve will remain data dependent. On the global level, China is facing headwinds and to that effect we are seeing some stimulus measures being passed to shore up investor confidence

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.