WEEK ENDING 7/21/2023

Highlights of the week:

- A quiet week for the markets awaiting Fed’s July rate decision and the latest inflation read.

- You cannot make this stuff up! MTG with Hunter Biden nudes, and what planet is RFK Jr. reporting from?

- O.S. — the summer of strikes! Who has the leverage: labor or capital?

A CITY DIFFERENT TAKE

It was a quiet week in terms of major economic releases.

Interest rates moderated slightly. Most of the market participant's attention is focused on next week's Federal Reserve meeting and Personnel Consumption and Expenditure (PCE) Index release. Municipal bonds outperformed their taxable equivalents, no doubt because of the summer doldrums this market experiences almost annually.

Labor seems to be gaining leverage with the number of ongoing and looming strikes. We think that with labor victories, wages should increase — which should add inflationary measures. This translates into a higher-for-longer Fed policy, unless something breaks in the economy. Given the amount of money in circulation (M2 money supply and the increase in its velocity, or turnover) we see a break low-probability outcome.

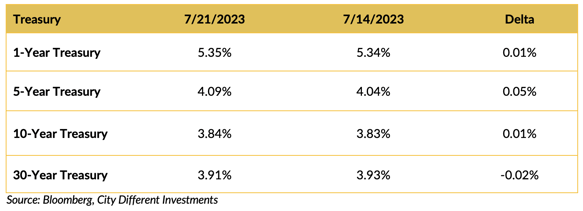

CHANGES IN RATES

By the looks of the above table, it was a quiet week in the Treasury market. Next week will be more interesting. The market is forecasting a 96% chance the Fed will increase short-term interest rates by 0.25% at it’s July meeting, and the PCE inflation numbers will be released on July 28.

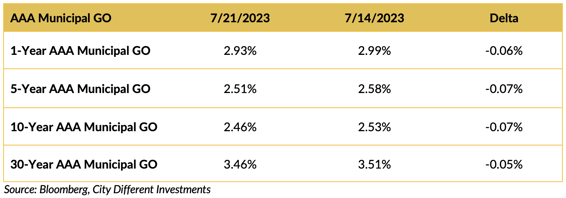

Yields moved lower across the municipal market over the last two weeks but at a much lower level than the Treasury market.

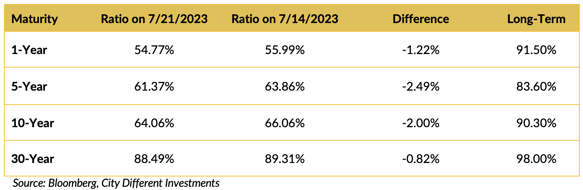

Muni/Treasury ratios are lower across all maturities. Municipals richened relative to Treasuries by this measure.

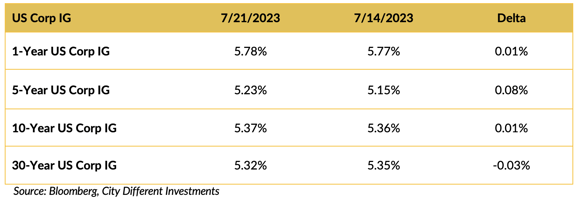

Yields in the investment grade (IG) corporate market were mixed over the last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

You can’t make this stuff up.

President Biden had a quiet week. He met with several tech executives to discuss the benefits and risks of artificial intelligence. This seems like a setup for the Will Rogers quote (let’s try this one), “The American people are a very generous people and will forgive almost any weakness, with the possible exception of stupidity.”

We hope that is true about our intelligence, artificial or otherwise. But the next three observations bring that precept into question.

Rep. Marjorie Taylor Greene did her best Larry Flint impression at a congressional hearing. Last week, Greene showed up to a House oversight committee meeting with nude photos of Hunter Biden. Now, that’s oversight!

“On Wednesday she turned up at the House oversight committee with a large poster board sporting a montage of photos showing a nude Hunter Biden engaged in sex acts. Where on earth did she get these? Assuming the photos are authentic and not doctored, probably from the laptop Hunter Biden famously left in a repair shop back in 2019.” Oh Baby, Baby

For the life of us, we don’t know what legislative purpose this served. Maybe it was just to have folks talk about MTG. If that was the case, it was successful.

Robert F. Kennedy Jr. testified before the Republican-led Select Subcommittee on the Weaponization of the Federal Government.

“Robert F. Kennedy Jr. worked to defend himself Thursday against accusations that he traffics in racist and hateful online conspiracy theories, testifying at a House hearing on government censorship despite requests from outside groups to disinvite the Democratic presidential candidate after his recent antisemitic remarks.” You said what?

Jack Schlossberg, the grandson of President John F. Kennedy, is not the only one embarrassed.

And last but not least, Gov. Ron DeSantis is defending Florida’s new African American standards by arguing that some Black people benefited from slavery. The Washington Post highlighted the following:

“They’re probably going to show that some of the folks that eventually parlayed, you know, being a blacksmith into doing things later in life,” DeSantis said on Friday in response to reporters’ questions while standing in front of a nearly all-White crowd of supporters.” Slavery was good for enslaved people

Yeah, perhaps being kidnapped from your home, sailed halfway around the world in squalid conditions, toiling like a beast of burden, and finally — if lucky enough to have a family — watching it sold away from you is a price worth paying for blacksmith skills. (This last sentence is intended to be dripping with sarcasm.) If we don’t understand our true history, we will be condemned to repeat it.

All in all, this kind of stuff makes for some cringeworthy reading and a longing for Congress to get out of town.

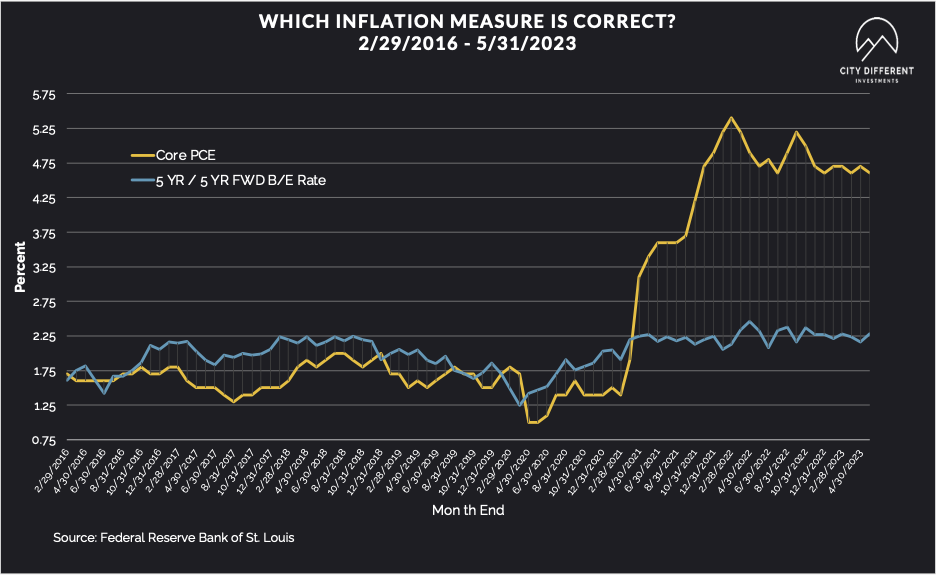

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.47%, a 14-basis point increase over the July 14 close of 2.33%. The 10-year Breakeven Inflation Rate finished the week at 2.35%, an 11-basis-point decrease over the July 14 close of 2.24%.

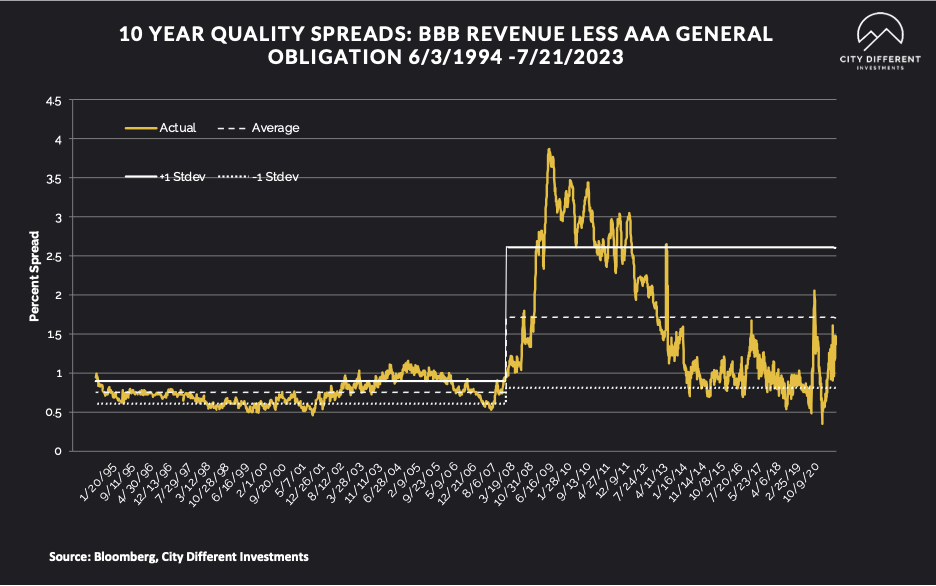

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of July 21 was 1.47% (based on our calculations), 0.06% higher than the July 14 close of 1.41%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

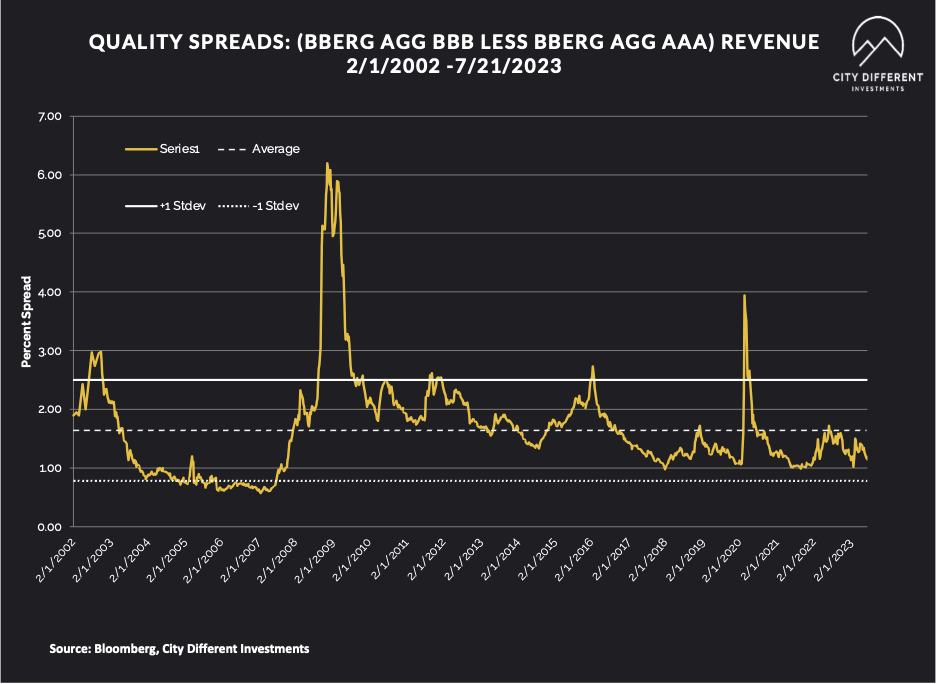

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 1.15%.

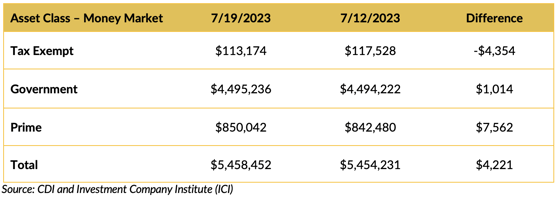

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

In total, money market funds saw positive cash flows. Municipal money market funds saw negative cash flows. That could be because of the richening of the municipal/taxable ratios.

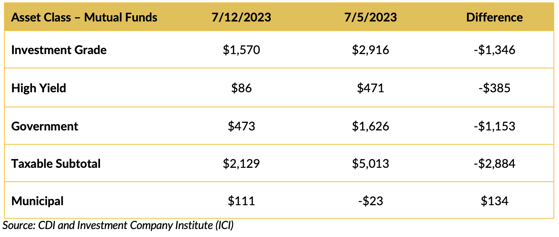

Mutual Fund Flows (millions of dollars)

Flows into bond funds are negative for the week.

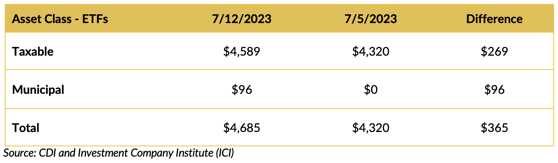

ETF Fund Flows (millions of dollars)

Bond ETFs also saw positive cash flows.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply is starting to build, with reports slated somewhere around a moderate $7.1 billion.

CONCLUSION

Congress, please leave town! Let the national embarrassment stop.

Markets should be getting ready for what could be a volatile week. The Fed’s next action will be announced along with their favorite inflation measure. This could prove to add volatility to a quiet market.

To borrow a line from “Jurassic Park,” participants: “hold on to your butts.”

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.