WEEK ENDING 06/24/2022

Highlights of the week:

- In his semi-annual testimony before Congress, Chairman Powell was resolute in the Fed’s desire to tame inflation.

- The stock market rallied for the first time in weeks, abating fears of a recession.

- Two significant Supreme Court rulings were announced Friday. And we don’t feel that much freer or safer.

A CITY DIFFERENT TAKE

Last week, the stock market rallied for the first time in a long time. Chairman Powell was adamant in the Fed’s resolve to fight inflation. Market sentiment turned away from the view that a severe recession is on the horizon to one that extends the horizon and lessens the estimated severity of any potential recession. It’s kind of hard to see a near-term recession materialize, given that unemployment is at 3.6% and there are two jobs for each individual seeking employment.

The U.S. Supreme Court captured the headlines on Friday with two important decisions. (More on that below in our “This Week in Washington” section.) One question: will these decisions motivate voters in the midterms and in 2024?

Shareholders kept on “moving to the exits” of municipal bond mutual funds while municipal bond ETFs continued to see marginal positive cash flows.

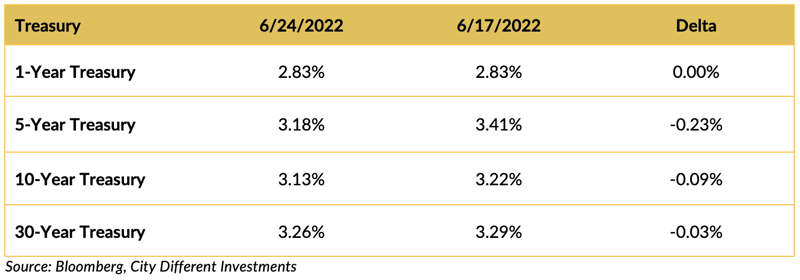

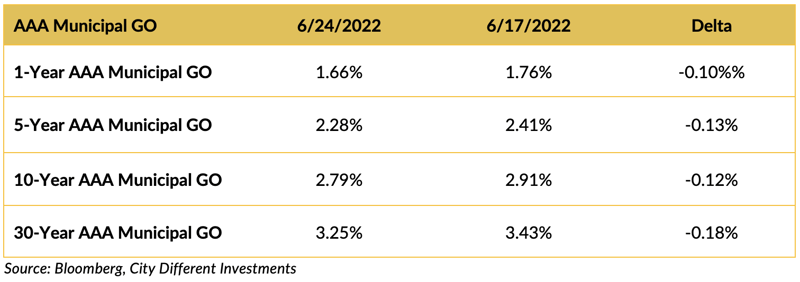

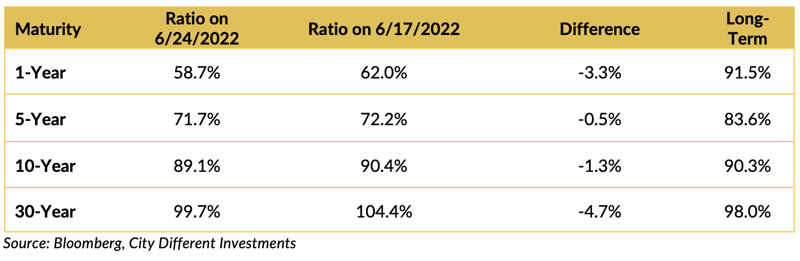

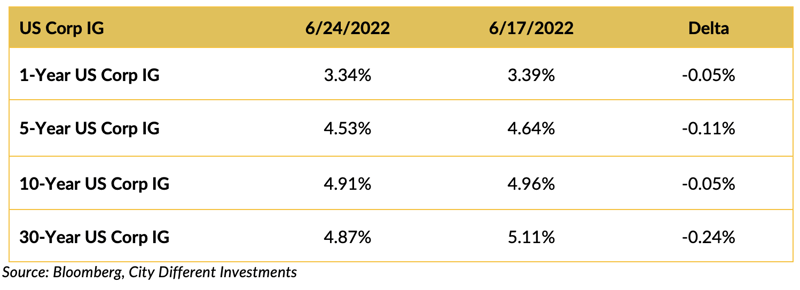

CHANGES IN RATES

Rates in the Treasury market moved lower last week, and the slope of the yield curve was essentially unchanged.

Rates in the municipal market decreased in the holiday shortened week and the curve marginally flattened.

Muni-Treasury ratios decreased from last week and remain in-line with historical averages on the long end. A higher M/T ratio tends to make munis a more attractive buy.

Investment-grade rates were lower last week following the Treasury market’s lead.

THIS WEEK IN WASHINGTON

In this week’s review on Washington, let’s discuss Chairman Powell’s semi-annual congressional testimony; Congress passing a watered-down gun safety bill; and the Supreme Court’s two landmark opinions (along with Justice Thomas’s hope for the future).

Federal Reserve Chair Powell testified before Congress this week, reinforcing the Fed’s commitment to curtail inflation with the tools available to them. The semi-annual Kabuki dance followed political lines as the members of the various committee’s took every opportunity to engage in demagogy in front of the cameras.

Congress passed the first gun safety bill in decades, albeit a very watered-down bill. It seems like passing this bill should have been easier, given that Americans widely support gun safety legislation. A Quinnipiac Poll reported:

“Americans support 74-24 percent raising the minimum legal age to buy any gun to 21 nationwide, according to a Quinnipiac University national poll of adults released today. Democrats (91-7 percent), Independents (76-22 percent), and Republicans (59-39 percent) all support raising the minimum legal age to buy any gun to 21 nationwide.”

The other big news out of Washington centered around two important SCOTUS opinions.

First, on Friday, SCOTUS overturned Roe v. Wade. The ruling sparked both pro-choice and anti-abortion demonstrations across America. On June 13, the Pew Research Center reported:

“Today, a 61% majority of U.S. adults say abortion should be legal in all or most cases, while 37% think abortion should be illegal in all or most cases. These views are relatively unchanged in the past few years. The latest Pew Research Center survey, conducted March 7 to 13, finds deep disagreement between — and within — the parties over abortion. In fact, the partisan divide on abortion is far wider than it was two decades ago.”

Given all the controversy surrounding the Supreme Court, one must wonder if SCOTUS risks losing its legitimacy.

The other opinion handed down was New York State Rifle & Pistol Association v. Bruen, which eased conceal and carry rules across the country. Some law enforcement officials have stated this in fact makes their job more challenging and will put more guns on the street – not a move to make our lives safer.

And if that’s not enough — while the SCOTUS dust was settling, CNBC reported this headline over the weekend: “Supreme Court Justice Clarence Thomas says gay rights, contraception rulings should be reconsidered after Roe is overturned.” To be fair, this is a long-held position of Justice Thomas. It’s starting to feel like the camel’s nose is sticking under the American tent.

The conservative philosophy was once based on the tenant of “personal accountability” and the corollary of “staying out of people’s bedrooms.” The only conclusion we can draw is that gun rights are more important than women's rights.

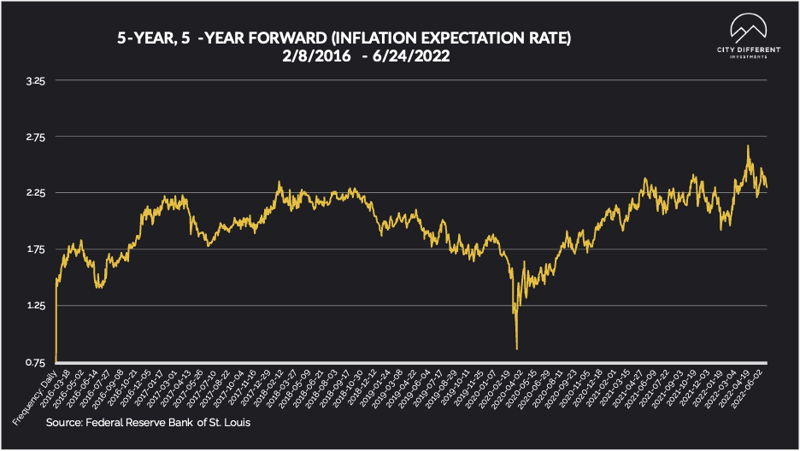

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended the week at 2.30%, down 6 basis points from last week's 2.36%. The 10-year Breakeven Inflation Rate was 2.56% at week's end, down 2 basis points lower from the prior week's 2.58%.

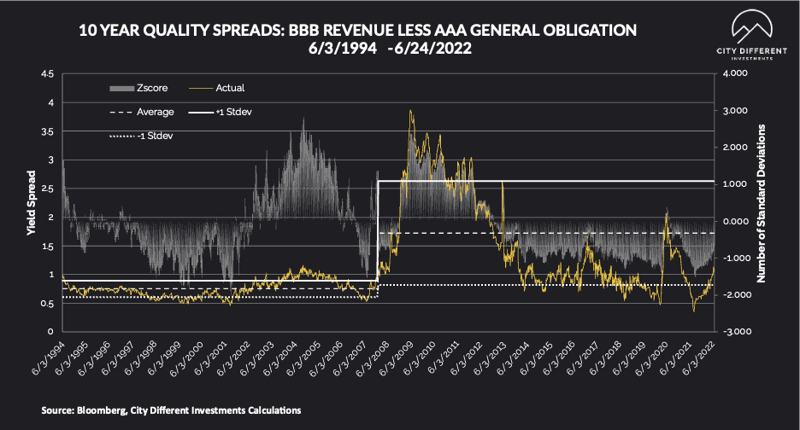

MUNICIPAL CREDIT

While we saw an increase in rates, credit spreads remained steady.

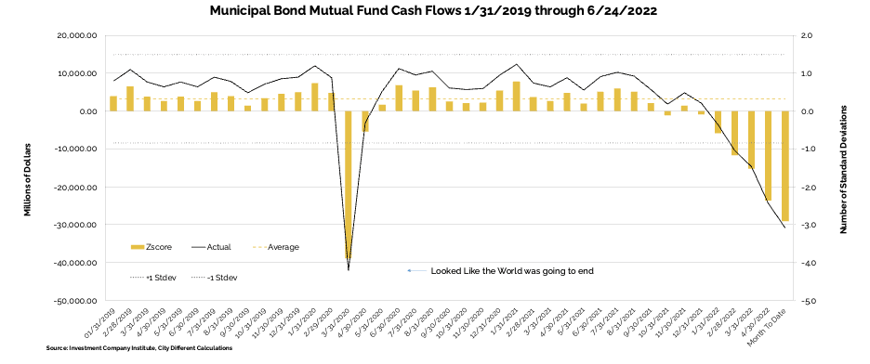

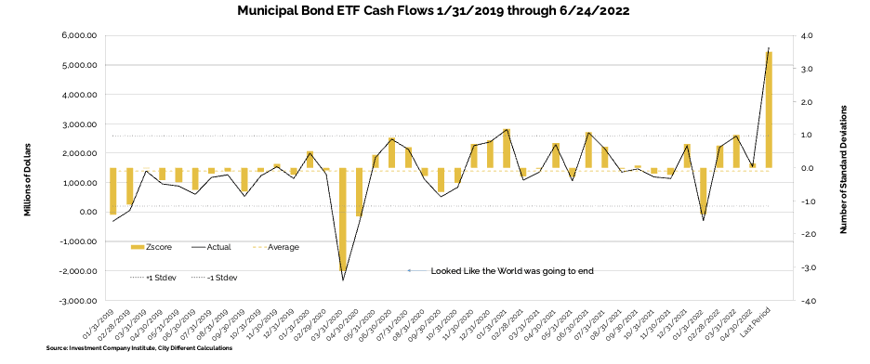

WHY IS THE MUNICIPAL MARKET BEHAVING THIS WAY?

Various sources are used to report cash flows related to municipal bond mutual funds and ETFs, all reporting at different times. The source we have chosen to use is the Investment Company Institute (I.C.I.). The I.C.I. reported weekly cash flows from municipal bond mutual funds for the week of June 15 as -$6.2B compared to -$2.2B from the week before.

Municipal bond ETF cash flows for the same period were -$633M, compared to -$398M the prior week.

Lipper reported combined weekly and monthly outflows of $1.6 billion for the period ending June 22, increasing YTD outflows to $74.7 billion. High Yield funds recorded $416 million of outflows. Intermediate funds saw $293 million of outflows. And Long Term funds saw $1.1 billion of outflows. Municipal ETFs registered $422 million of inflows.

Lipper reported combined weekly and monthly outflows of $1.6 billion for the period ending June 22, increasing YTD outflows to $74.7 billion. High Yield funds recorded $416 million of outflows. Intermediate funds saw $293 million of outflows. And Long Term funds saw $1.1 billion of outflows. Municipal ETFs registered $422 million of inflows.

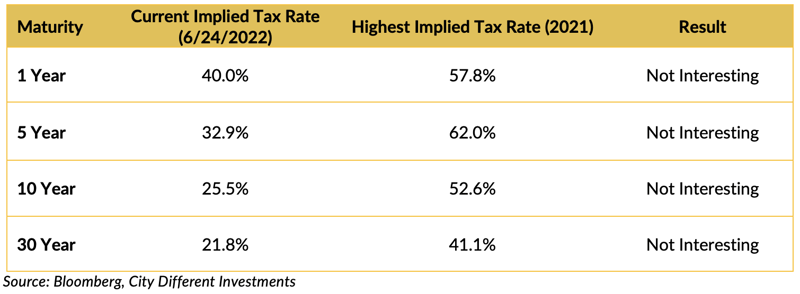

TAXABLE VS. TAX-EXEMPT MUNICIPAL BONDS

The implied tax rate for a taxable vs. a tax-exempt A.A. municipal bond in various maturities is as follows:

Municipal bonds have given back some of the rally that they experienced a week ago, catching up to their taxable counterparts.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

In its Municipal Markets Weekly newsletter, JP Morgan commented on the supply picture this week, stating that:

“Next week, we expect total supply of $7.9 billion, or 108% of the 5-year equivalent average ($7.3 billion). We anticipate tax-exempt supply of $7.6 billion (126% of average), and taxable/corp cusip supply of $0.3 billion (22% of average).”

The supply picture does not get interesting until it exceeds $10 billion tax-exempt issuances in a given week.

CORPORATE INVESTMENT GRADE AND HIGH YIELD OVERVIEW

In U.S. Investment Grade land, new issue activity has petered out as the fixed income market digests the volatility.

In its weekly "Credit Flows" report, Wells Fargo commented:

“Breaking Bad, redux. Our title of the outlook for this year was “Breaking Bad”, which refers to financial markets being well behaved most of the time after the financial crisis but now misbehaving. The key reasons for well-behaved markets were low monetary policy rates and QE — translating into inflows to credit and anyone being underweight suffered in terms of performance. Hence outperformance of “buy the dip” type strategies. This year in contrast is characterized by global central bank rate hikes and fading QE, now turning into aggregate QT as we speak. Hence increasing outflows and any episode where buy the dip works is a bear market rally that should be faded. Our ultimate endgame is recession. Small upward mark-to-market adjustments to our spread targets for Eurozone credit to 200bps and 650bps by year-end and 225bps and 850bps by the end of 1Q23 for IG and HY, respectively.

Sell what you can most easily replace. While recession means further decompression of spreads (i.e., we recommend going up in quality), there are some differences compared to past episodes. First of all, with outflows and higher yields we expect selling pressures where money managers reached into non-core asset classes — like HY investors selling loans and IG liquidating HY. Second, we like to be short senior banks globally as investors sell risk that can most easily be replaced (when it comes time to that) — so expect the already wide banks-industrials relationship to widen further. Third, while in a normal recession IG spread curves steepen this time outflows lead to selling pressure in the front end of the curve and flattening while higher yields trigger yield sensitive buying in the back end of the curve, adding flattening pressure.

Need more barbell. We recommend credit investors position in a barbell approach with large BBBs. For IG investors this means a 50/50 portfolio of large BBBs and ultra-short (<1 year) high quality paper, which should outperform A or AA rated positions as the reduced notional in BBBs overcomes decompression. HY investors should sell BBs and buy BBBs with the same duration — even if they have to put 1.5 times the notional in the latter.

When the tide goes out. We view the Italy situation as an example of issues masked by years of super-easy global monetary policies that are now coming to the forefront given the shift to policy tightening in order to combat inflation. Yields suddenly matter for debt sustainability.

Contagion to global credit. Furthermore, Italy’s debt burden is highly systemic — especially to global corporate credit — as Bloomberg estimates the country has more than €2.3 trillion of BBB2 rated sovereign debt outstanding — exposures to which likely runs deep in Italian banks and global insurance companies. Some of these mandates are likely ratings sensitive IG accounts forced to sell in case of a downgrade to HY.”

CONCLUSION

Markets will continue to be volatile. Investors should focus on fundamentals and invest using well-known risk mitigation techniques such as dollar-cost averaging. Rates have been so low for so long that the initial uptick in rates are tempting. We are maintaining our accounts on the lower end of their respective risk spectrums until we feel we are being adequately compensated to take on more risk.

.png?width=500&name=signature%20block%20(3).png)

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.