.png)

WEEK ENDING 6/23/2023

Highlights of the week:

- A short-lived revolt in Russia over the weekend could cause even more market volatility.

- As the world gets scarier, remember that fear is never a good investment strategy.

- Fed takes a break but promises more increases. Kind of.

A CITY DIFFERENT TAKE

It has been two weeks since we published our last weekly commentary, and there is a lot to talk about. We had anticipated writing about the Federal Reserve’s hawkish skip, the Fed governor's comments, and inflation. But by Saturday morning, it seemed the world had gotten scarier with a potential civil war in Russia. We’ll start there.

On Friday, the Wagner group, having pulled its mercenaries out of Ukraine, headed towards Moscow. The Kremlin readied its defenses to meet this new idiosyncratic risk, with armored vehicles in the streets and the mayor telling citizens to stay home on Monday. An initial concern from the US and others was the potential impact to Russia’s nuclear arsenal. Another outside question: what does this do for China’s intentions toward Taiwan? Will China view the West’s focus on Russia as an opening to reacquire the island nation?

On Saturday, after a short-lived revolt, a deal had been reached that called for the Wagner group to halt the advance in exchange for an immunity deal for Prigohzhin and his troops. It is good to remember that once you go after the king, you need to kill the king! Volatility indeed.

What does this mean for the markets? While this particular crisis was averted, major one-off events can lead to a huge spike in volatility. Let’s explore what we might have seen in the markets today if Wagner had kept up its march (or if some other crisis arises).

If not resolved, we would have expected to see a significant sell-off in the equity market (perhaps a buying opportunity?). Following the fear trade into the bond market, we would expect a flight to quality in the Treasury market; additional fuel should be provided by anyone short Treasury securities as they try to cover those shorts. One might also expect the Treasury curve to steepen, with short-term rates declining more than long rates. The 2s10s Treasury spread closed Friday at -1.00%. Additional momentum to a steepening move would be provided by market participants covering any flattening trades, which have worked up until now. If this steepening does occur, all those investors that were attracted to the enticing yields of money market funds will be disappointed when they see how quickly they can drop. (Can you say “reinvestment risk”?)

Our strategic outlook has not changed since November, when we moved all our accounts to the neutral duration range because we could build a bearish and bullish scenario for fixed-income markets with equal conviction. Making significant strategic portfolio decisions in such periods of chaos has not proved to be a winning strategy in our experience.

Now back to the Fed…

At its last meeting, the Fed skipped raising short-term interest rates, continued quantitative tightening, and forecasted two additional rate increases (without specifying when). Inflation still has “a long way to go” and companies are still hiring. A hawkish tune is evident in other Fed Governor statements and Chairman Powell’s semi-annual congressional testimony. The 2s10s slope widened to 1.01% as of Friday.

Core inflation, measured by core CPI, is proving to be sticky at 5.3%. We must wait a few days to see what the latest core PCE reading will yield.

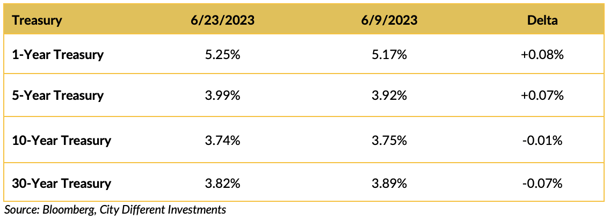

CHANGES IN RATES

All the movement in yield in the Treasury market took place in the front end of the curve. Yields increased in the front end and were essentially unchanged in the long end of the market. No doubt a reaction to the Fed’s hawkish skip. In the news conference, Chairman Powell indicated that there were two more 25-bps increases on the bale but did not say when.

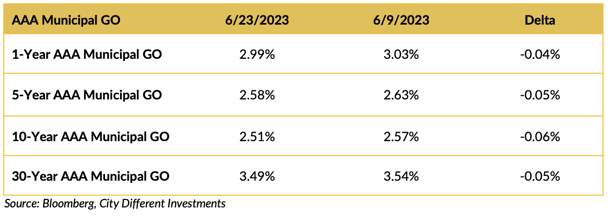

Yields moved slightly lower across the municipal market over the last two weeks. Factors driving this move are low supply and a turnaround in negative cash flow into mutual funds.

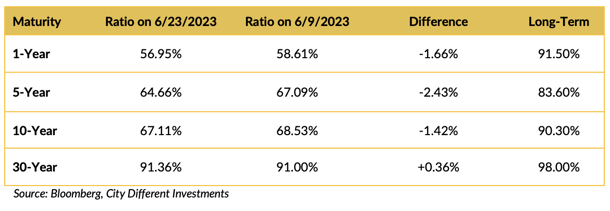

Muni/Treasury ratios are lower across most of the curve. This is nothing more than a reaction to the yield movements of the two markets.

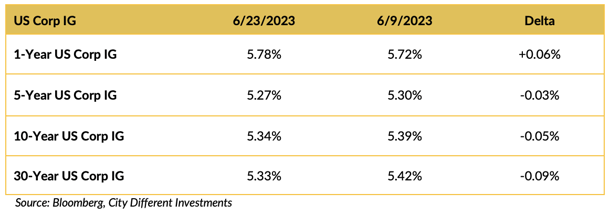

Yield in the investment grade (IG) corporate market moved lower over the last two weeks.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

It was a relatively quiet week in Washington if you exclude the whole “Russian Weekend” incident—see above.

The Prime Minister of India visited Washington. Chairman Powell testified before Congress in his semi-annual visit.

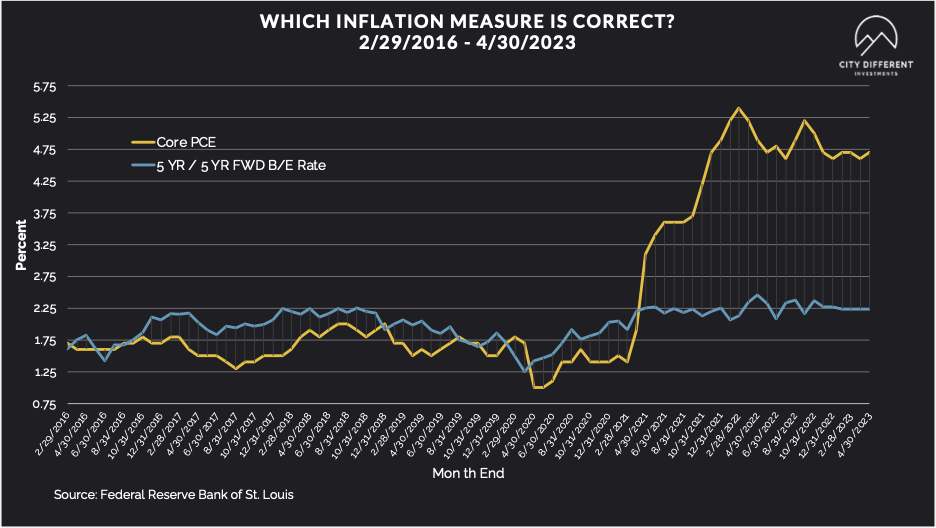

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.26%, a one-basis point decrease from the June 9 close of 2.27%. The 10-year Breakeven Inflation Rate finished the week at 2.21%, a one-basis point increase over the June 9 close of 2.20%.

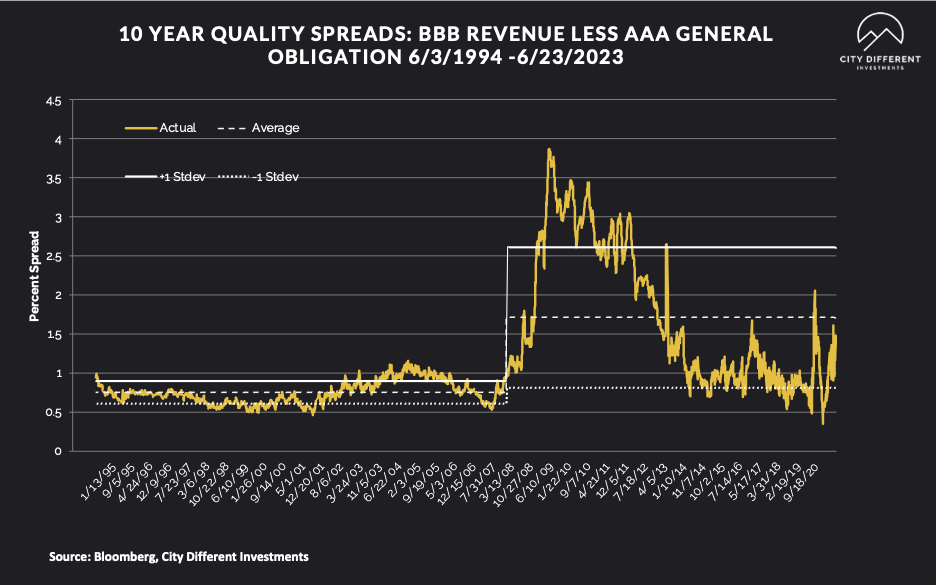

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of June 23 was 1.37% (based on our calculations), 11 basis points lower than the June 9 measurement of 1.44%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

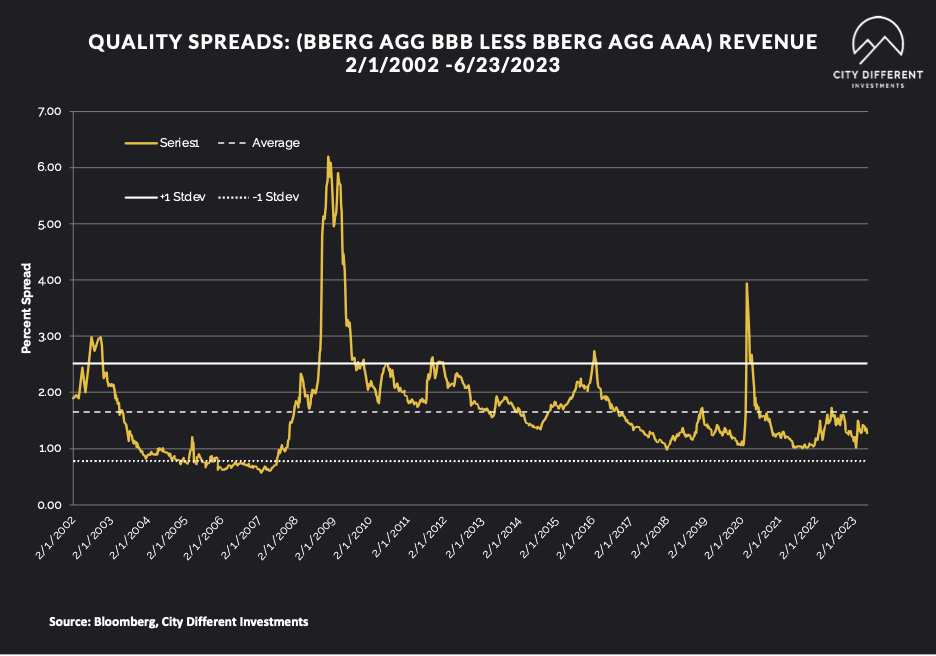

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 1.28%.

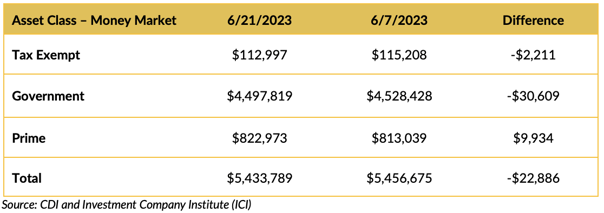

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Looks like flows into money market funds took a break over the last two weeks, all but prime money market funds.

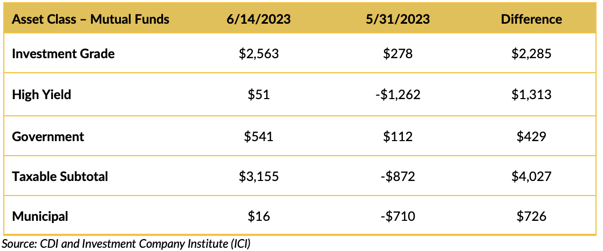

Mutual Fund Flows (millions of dollars)

Flows into bond funds are positive. High Yield bond funds were the weekly winner. Municipal bond funds turned positive.

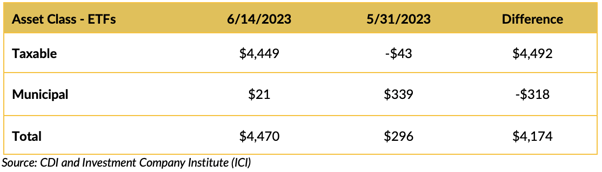

ETF Fund Flows (millions of dollars)

ETFs saw positive cash flows.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply is starting to build, with estimates slated somewhere around $10 billion.

CONCLUSION

The world got scarier this weekend. The “Russian Weekend” was an example of that, and the full ramifications have not been fully felt. If we were Prigozhin, we would stay away from the windows (and we’re not so sure that Belarus is the safe haven it’s cracked up to be).

Time will tell. All of this should add to the market’s volatility.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.