.png)

WEEK ENDING 6/9/2023

Highlights of the week:

- Market expects a temporary pause from the Fed this Wednesday.

- What’s the status of the recession?

A CITY DIFFERENT TAKE

Chairman Powell's Federal Reserve does not like to surprise the market. Communication is important for this Fed. The message for June is that the Fed may pause and signal guidance for the future. Going into Wednesday’s meeting, we are giving credence to Powell's message from May’s monetary policy symposium where he said, “Having come this far, we can afford to look at the data and the evolving outlook to make careful assessments.”

Nevertheless, this is a big week for macro data releases. CPI data comes out on Tuesday right before the Fed meeting. The current tone is that between now and July the Fed will look at wage and Core PCE to see if another hike is needed.

It is widely expected that Powell will set a hawkish tone, even if the Fed pauses rate hikes for June. The market has priced a 30% chance for a June hike and an 85% chance for a July hike. The median dot plot for the anticipated Fed funds rate is at 5.3% for year-end 2023.

The case to support a hike is simple if Core PCE does not budge.

On the macro front, remember CDI has always presented the thesis of making a case for the bull and bear market with equal conviction. This is rooted in our study of economic data, which has been conflicting so far. But the call for an economic recession has gone unanswered in the face of a strong labor market. The U.S. consumer has remained strong with the support of excess savings from the pandemic shutdowns.

Goldman Sachs has lowered the U.S. recession probability to 25% versus the consensus call which still predicts a recession in the second half of 2023 or early 2024 at 65% probability. Morgan Stanley seems to agree with Goldman Sachs and is also calling for a soft landing. Consumer spending in the U.S. is rising. April numbers show a strong 2.3% rise in spending YoY.

The bears are resting their case on a slowdown in growth momentum and lags from the large rate tightening.

A study of Fed tightening cycles by NDR research shows that ten of the 13 Fed tightening cycles since 1953 have ended in a recession. This typically starts on an average of six to seven months after the last rate hike. There is a lot of uncertainty around when the last rate hike will be.

It is incredibly hard to call a recession in real-time. We only know of this in retrospect, when NBER declares one.

CHANGES IN RATES

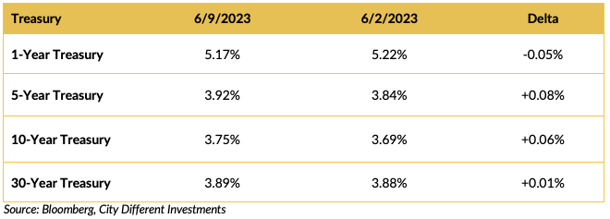

Yields in the Treasury market were very quiet last week, which is not surprising given that the debt ceiling deal is behind us. We expected today’s market opening to be interesting given the announcement of the former president’s indictment, but the impact seems to be more political thus far.

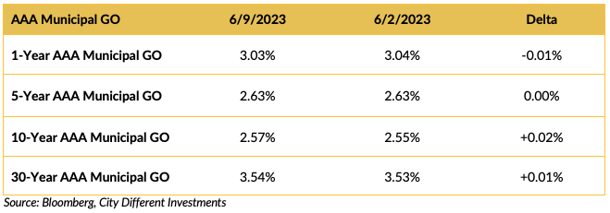

All quiet on the municipal yield front.

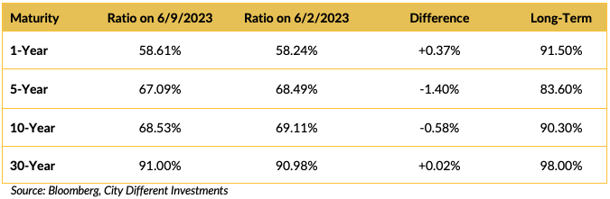

Yet again, the muni/Treasury ratios moved marginally lower on the week. AAA general obligation municipal bonds in maturities greater than five years make sense for anyone in the 33% marginal tax bracket or higher.

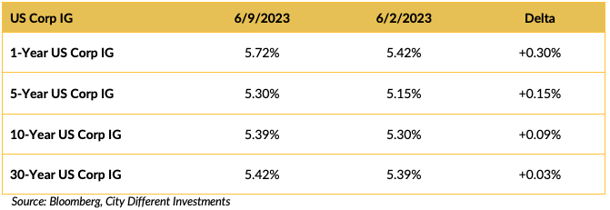

Yields in the investment grade (IG) corporate market moved higher, with short maturities sustaining the most significant increases. The investment grade corporate market option-adjusted spread currently stands at 137 bps, compared to the average over the last 30 years of 127 bps.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Former President Trump was federally indicted last week on more than three dozen counts of possessing and refusing to return highly classified government data. He is expected to surrender to authorities on Tuesday afternoon. While the politics surrounding the indictment are expected to be stupendous, markets have remained calm thus far.

On the global front, Putin is threatening to place “tactical nuclear weapons” in Belarus next month.

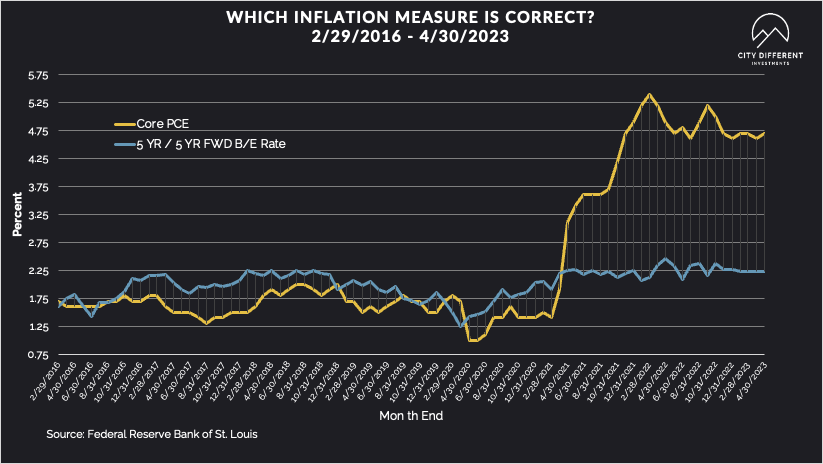

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.27%, a 4-basis-point increase over last week’s close of 2.23%. The 10-year Breakeven Inflation Rate finished the week at 2.20%, 2 basis points higher than last week’s close of 2.18%.

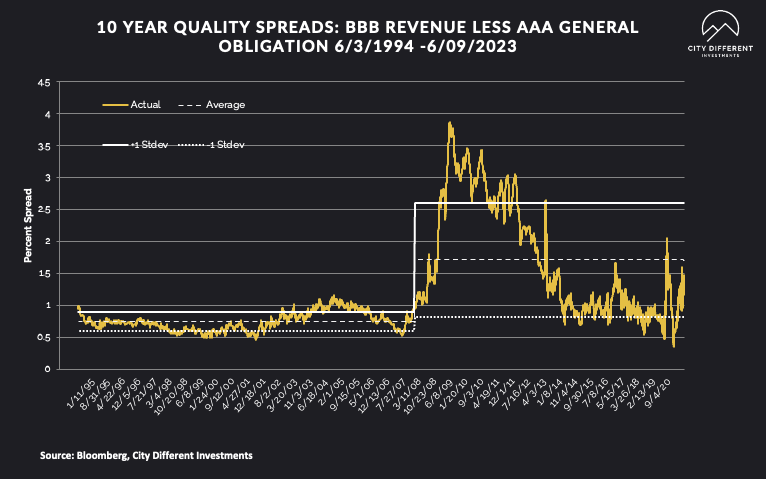

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of June 9 was 1.48% (based on our calculations), 4 basis points higher than last week’s 1.44%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

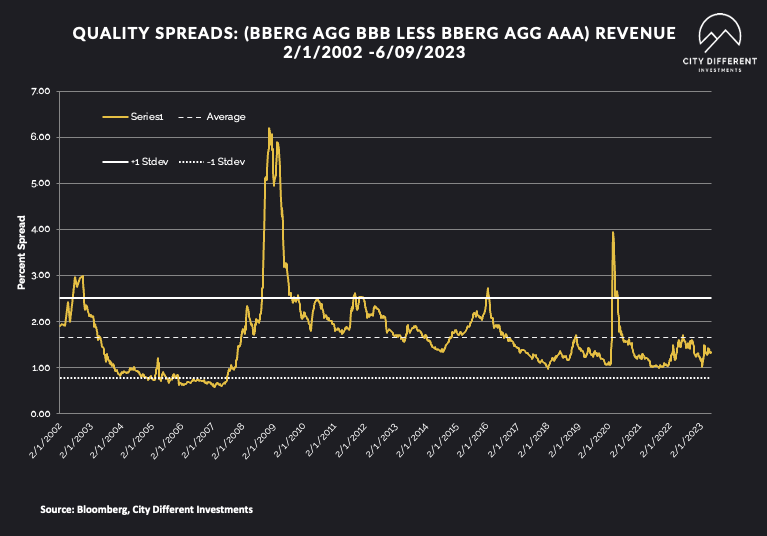

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 1.35%.

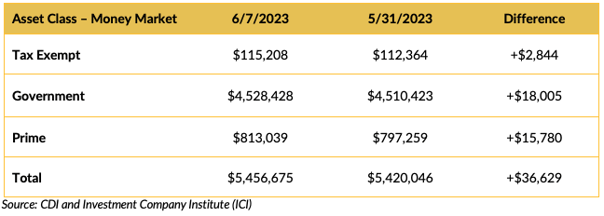

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds saw positive cash flows. Disintermediation continues; high money market yields are pulling cash out of bank deposits.

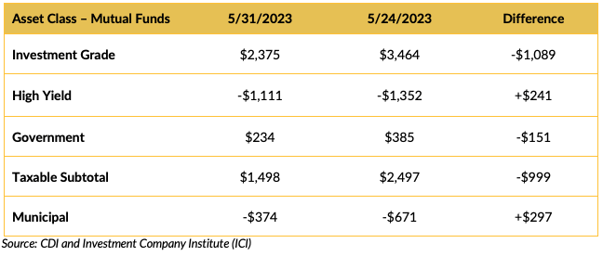

Mutual Fund Flows (millions of dollars)

Flows into bond funds are weak. Investment grade bond funds were the weekly winner. Municipal bond funds continue to see withdrawals, although some more current reports show a reversal in the negative cash flows.

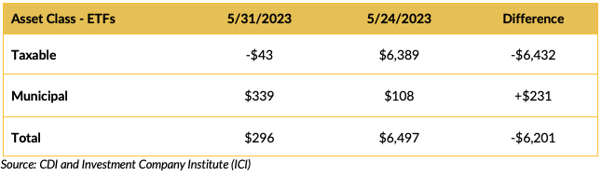

ETF Fund Flows (millions of dollars)

ETFs saw negative cash flows, driven by taxable funds.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Reports are that this week’s supply is slated somewhere around $4.9 billion.

CONCLUSION

This is a big macro week. Tuesday's CPI release will be followed by “Fed Day” on Wednesday. The market expects a rate pause, with new guidance to emerge from Powell and his team. Calls for a recession appear to be wrong so far in the face of a strong U.S. consumer drawing on savings and a robust jobs market.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.