WEEK ENDING 5/5/2023

Highlights of the week:

- Fed hikes rates by 25 bases points as expected—Powell leaves the door open for June pause.

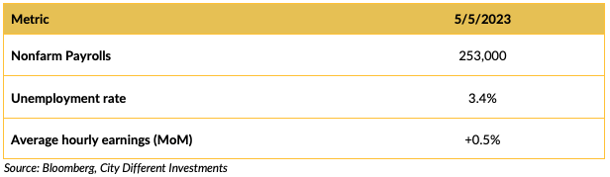

- On Friday, non-farm payroll rose by 253,000.

- What does a brief debt ceiling default look like?

A CITY DIFFERENT TAKE

There is much to discuss from last week. The main takeaway from the Federal Reserve is that they are becoming more data dependent. Whether they hold or hike (cuts are a distant third option, it seems) will hinge on their assessment of the damage from the 500 basis points of rate increases within 14 months. This is the 10th rate hike for the Fed from last year’s 0% interest rate.

How will they measure that? Powell is highlighting the importance of credit conditions. In the near term, that means an even greater focus on today’s Fed Senior Loan Officer Survey. Market expectations show a 4% probability of a cut at the June meeting. There’s still a lot of economic data to be released before the June meeting, and six weeks for the banking sector to convince investors that any future issues are isolated and contained. Before the June FOMC, we’ll see two jobs reports, two CPI reports, and one month of PCE data. Along with a status check on banking sector stability and credit tightening impacts, these reports will shape the Fed’s decision on how to balance the risks between leaving stubborn inflation unchecked and potentially exacerbating banking industry jitters.

The dark cloud that would accelerate a pause or a pivot truly are more unintended consequences in banking, credit crunch, and a debt ceiling political drama gone wrong. Of course, there are lagged and varied consequences of monetary policy. These are just the horsemen on the horizon for now. We saw SVB, Signature, and others collapse in March. First Republic collapsed last week, and now Pac West, among other regional banks. All this shows the reverberation of the 500-basis point’s impact on our financial system. The FDIC plans to release a proposal as soon as this week to refill its Deposit Insurance Fund. The proposal is said to target all larger lenders, with smaller banks with assets less than $10-$50B exempt from the proposal.

On Wednesday, Chairman Powell spoke about the labor market that remains “extremely” tight and is one of the data points he and his colleagues will carefully assess as they determine whether more hikes are needed to cool the economy. Guess what? Friday’s jaw-dropping nonfarm payroll suggests a robust job market.

The unemployment rate is now at a multi-decade low of 3.4%

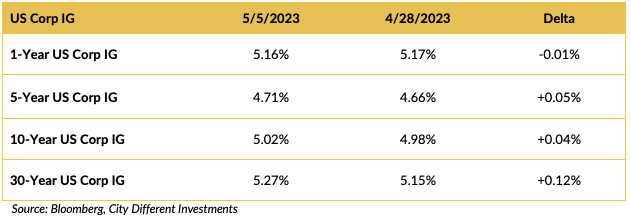

CHANGES IN RATES

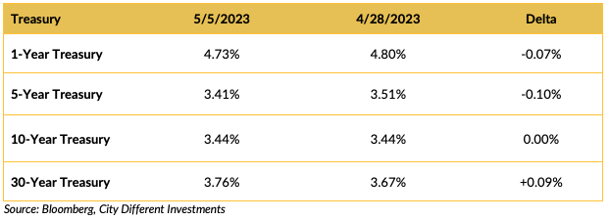

Looking at the table above, we think the strong labor market reduces the probability of rate cuts.

Yields on short Treasury securities moved lower on the week. While yields on longer-maturity Treasury securities were unchanged or higher for the week, causing the yield curve to steepen. A favorite market measure of the Treasury yield curve slope is the 2–10-year spread, which finished the week at -0.48%, ten basis points steeper than the previous weeks’ -0.58%. The maximum negative spread this measure achieved was -1.08% on 3/8/2023. Then a couple of California banks ran into trouble, and the curve steepened, based on the market anticipating a pause or pivot by the Federal Reserve (Friday's employment report put a damper on that hope). Next week’s inflation reports should add to the volatility.

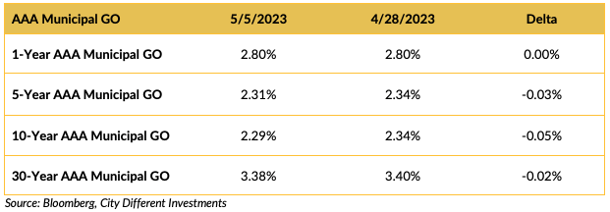

The municipal market has a mind of its own, with yields in the municipal market unchanged for the week. This represents a further adjustment from very rich levels.

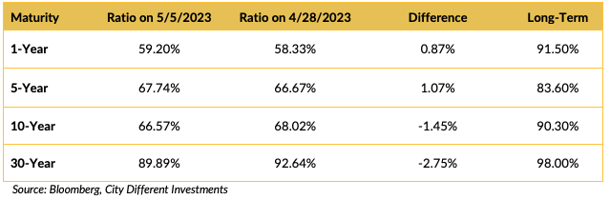

Municipal ratios moved higher in the short end of the market and lower in the long end of the market.

Yields in the investment grade (IG) corporate market moved higher on the week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

On the debt ceiling, Bloomberg News summarized a series of White House talking points about the horrors of default. According to the Council of Economic Advisors to the President, a brief default would result in a half-million job losses and a 0.3% increase in unemployment. In contrast, a protracted default would mean 8.3 million jobs lost and a 5% increase in unemployment. The White House continues to insist it will not compromise in negotiations, despite the fact it does not have enough support in the Senate to move the President’s version of a debt-ceiling increase. Thankfully, according to the WSJ, the White House and congressional leaders are considering alternative ways to avoid default, including a short-term deal allowing ceiling negotiations alongside budget negotiations. Treasury Secretary Yellen recently warned default could come as soon as June 1, though the Treasury tends to be conservative, and traders are skeptical it would be so soon.

Will bondholders be compensated for any delays in Treasury payments from a failure to reach a debt ceiling resolution? Our best understanding comes from this 2021 NY Fed document, particularly this statement:

“It would require explicit legislation by Congress to provide compensation to holders of securities subject to a delayed payment on Treasury debt for the delay in these payments.”

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended the week at 2.23%, seven basis points higher than the April 28 closing of 2.16%. The 10-year Breakeven Inflation Rate ended the week at 2.21%, three basis points higher than last week’s observation of 2.18%.

MUNICIPAL CREDIT

Most of the action was contained on the rates side for the municipal market. 10-year quality spreads (AAA vs. BBB) as of 5/5/23 were at 1.30% (based on our calculations), 0.08% lower than last week’s 1.38%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

Quality spreads in the taxable market are not attractive but are moving in the right direction ending the week at 1.42%.

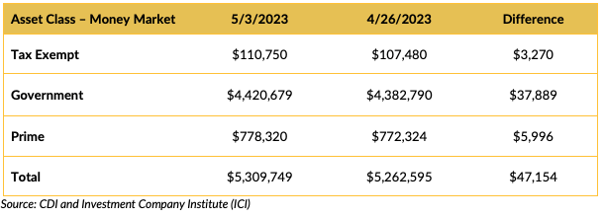

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds saw some love (in the form of positive cash flows) in the week ending 5/3/23. All funds saw positive cash flows, with the government money market funds seeing the most cash in.

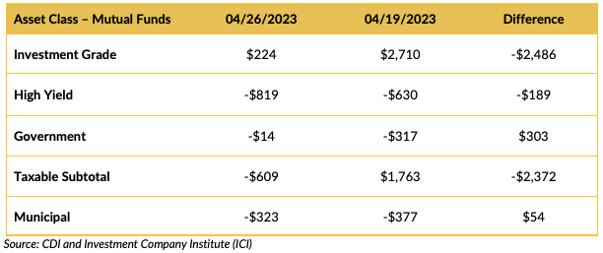

Mutual Fund Flows (millions of dollars)

Flows into bond funds were negative for the week of 4/26/2023. Competitive money market rates are proving to be some competition for bond funds.

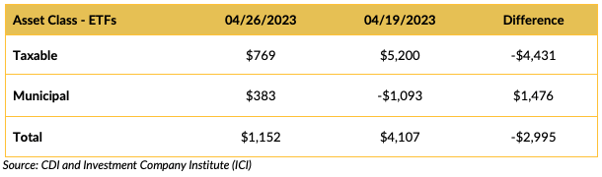

ETF Fund Flows (millions of dollars)

ETFs saw a lower volume of flows at a slower pace than the week before.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply outlook is moderate, slated somewhere around $9.1 billion.

CONCLUSION

Last week brought about a 25-basis point rate increase. But more clarity came from the Fed statement that read,

“In determining the extent to which additional policy firming may be appropriate.”

Essentially, we are now looking at an explicit data-dependent Federal Reserve that is watching for tighter credit conditions and their effect on the economy. In addition, regional banks are heightened on the Fed’s radar. The other left-field event, of course, is the political drama surrounding the debt ceiling that is keeping the market and the Fed on its toes.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.