.png)

WEEK ENDING 5/19/2023

Highlights of the week:

- Soft landing still a possibility.

- June rate hike slowly being put back on the table.

- Is it a good time to buy bonds?

A CITY DIFFERENT TAKE

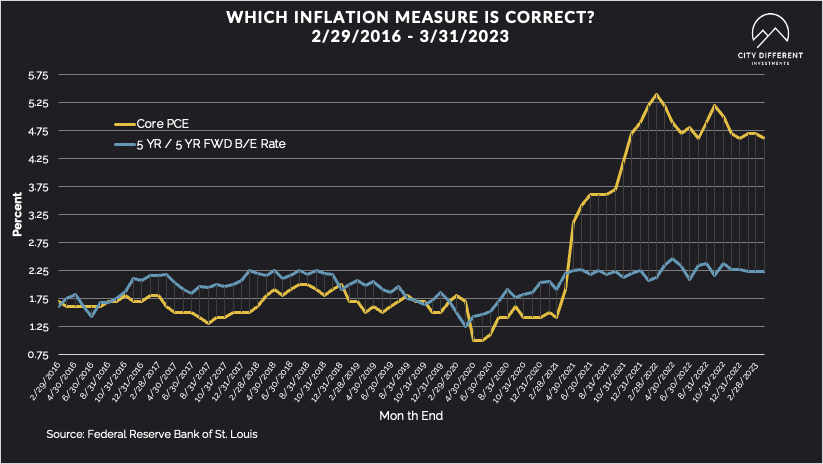

CPI and PPI numbers were softer last week. We are starting to believe inflation has been trending lower for many months.

On the labor market front, unemployment stands at a multi-decade low of 3.4%. Last week, payroll numbers came in at 250,000 (though revisions of -140,000 were too easily dismissed).

We also saw good retail numbers for April as far as inflation is concerned. Retail sales rose by 0.4% versus the consensus expectation of 0.8%. The Federal Reserve’s soft-landing scenario requires claims to stay steady and inflation to trend in the negative direction. Even though Core PCE (a measure quoted in this piece) doesn’t include energy prices, it is hard to ignore oil. Prices for crude are down 35% year-over-year.

Fed speakers demonstrated a hawkish shift in tone last week. After the May hike, the market wrote off the possibility of any June raises. But the Fed speakers are clearly putting June back on the table. We now have around a 40% chance of a June hike priced in, although reports remain that it will still be a close call. To remind our readers what a fickle friend market expectations can be, at one point, the futures market had a rate cut built in for June.

To summarize all of the Fed speak from last week, the central message was that inflation still is on the higher side. The Fed really does not want a repeat of the 1970s when it abandoned the tightening cycle prematurely. Adding to everyone’s amazement is that the labor market is surprisingly strong. The lagged and varying effect of the monetary policy could complicate the picture in the form of regional banking instability. The other curveball will be politics and the debt ceiling. More on that in “This Week In Washington.”

CHANGES IN RATES

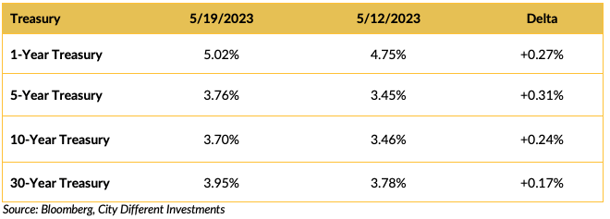

Yields in the Treasury market increased across all maturities. The slope of the yield curve between 2 and 10 years was essentially unchanged week over week.

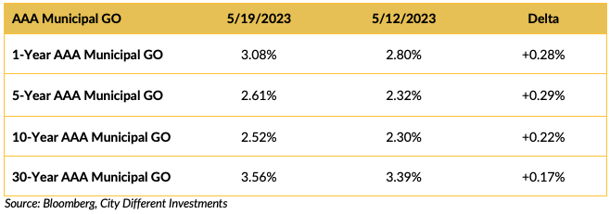

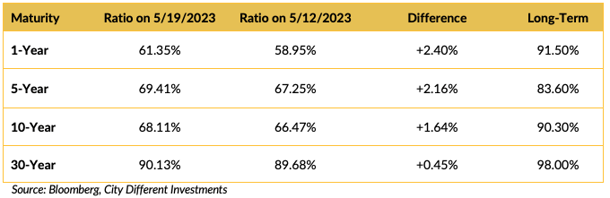

Yields in the municipal market increased on the week. After weeks of lagging the Treasury market, adjustments to the yield in the muni market have come. This adjustment moves the muni/Treasury ratio closer to fair ranges.

The muni/Treasury ratios moved marginally higher on the week. AAA general obligation municipal bonds in maturities greater than five years make sense for anyone in the 33% marginal tax bracket or higher.

For those friends who have asked us whether now is a good time to buy bonds, our answer is, “Yes.” It is a good time to buy bonds. But the more important question is “What bonds should I buy?”

On the municipal front, remember the highly unusual nature of the muni curve, which has been inverted all of this year. The municipal curve slope has 1-year bonds trading near implied yields of 30-year maturities, with a declining gap in the rest of the curve. Credit conditions remain strong. Given the attractiveness of the short part of the curve, the 1-to-10-year duration looks interesting for those looking to invest in munis.

A limited-term approach is a defensive hedge against a "bull steepener.” We believe this positioning appears optimal if short-term rates fall faster and quicker than the longer-term part of the curve. Just a few paragraphs earlier, however, we spoke of a potential June hike. An active ladder portfolio structure allows us to overweight shorter maturities with higher rates and underweight the part of the curve around 6–10 years. As the slope of the curve changes, the portfolio is attractively positioned to take advantage of that change.

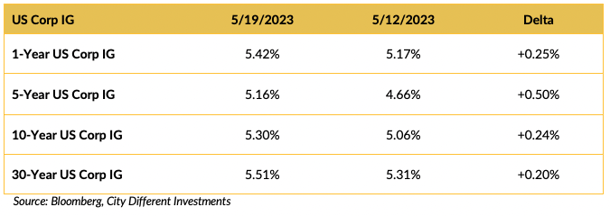

Yield in the investment grade (IG) corporate market moved higher on the week. On the taxable portfolio side, we like a limited-term strategy for the reasons stated above. Corporate supply has been healthy.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

The change in tone on the debt ceiling discussion is dizzying. The debt ceiling and delay in interest payments on bonds have been front-and-center for the market. Most of the week was spent in a positive tone territory where the market felt this issue would be resolved. But is it even “Washington” if reason prevails? Currently, President Biden and Speaker McCarthy are back to digging in their heels in support of their respective positions.

Let’s look at three possible scenarios for what would happen if we don't meet the debt ceiling “X-date” deadline.

Scenario #1 — Brief Extension: If a brief extension of the deadline happens, this means both sides are optimistic they can reach a solution in a short period of time. In this scenario, negotiators can reset the deadline by lifting the debt ceiling by an incremental amount or, the more likely scenario, by suspending it for a brief period (such as days, weeks, or months).

Scenario #2 — Prioritized Spending: If Congress refuses to move either the date or the limit briefly, the next most likely option is a prioritized payment schedule for the Treasury.

This was the plan the Treasury prepared in 2011. The market will be on high alert if there is a possibility of missed debt-service payments. In this scenario, the Treasury prioritizes debt service over Social Security and other payments.

Scenario #3 — Default: What constitutes a default is not just a non-payment but a delay in payment. How do you measure this probability? Look at the Tresaury bills that are maturing May 30 versus June 1. (June 1 is the start of the “X-date,” stated by Treasury Secretary Janet Yellen.) There is a 200-basis-point premium for Treasury bills maturing on May 30.

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended the week at 2.29%, 4 basis points higher than the May 12 closing of 2.25%. The 10-year Breakeven Inflation Rate ended the week at 2.24%, 6 basis points higher than last week’s observation of 2.18%.

MUNICIPAL CREDIT

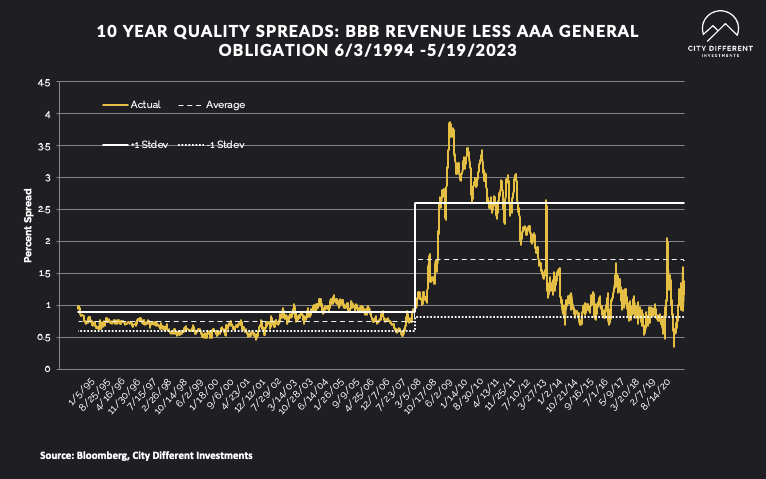

Most of the action was contained on the rates side for the municipal market. 10-year quality spreads (AAA vs. BBB) as of May 19 at 1.16% (based on our calculations), 0.04% lower than last week’s 1.20%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

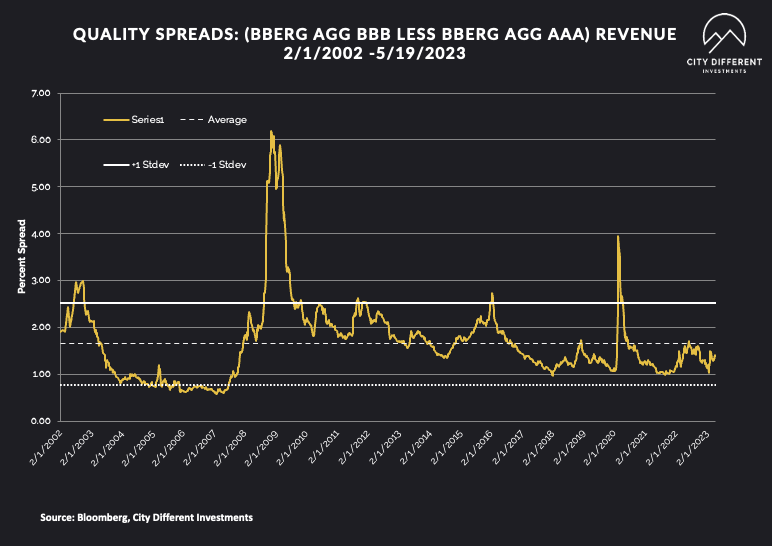

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 1.40%.

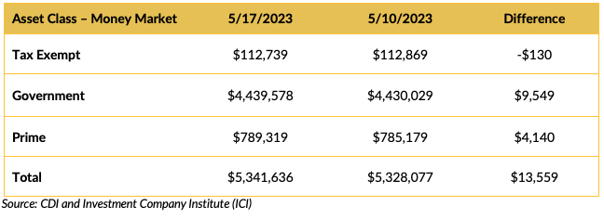

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds saw positive cash flows. Disintermediation continues; high money market yields are pulling cash out of bank deposits. This strategy is not without risk, as we outlined earlier.

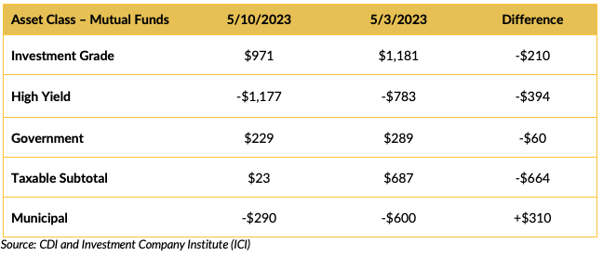

Mutual Fund Flows (millions of dollars)

Flows into bond funds are weak. Municipal bond funds continue to see withdrawals.

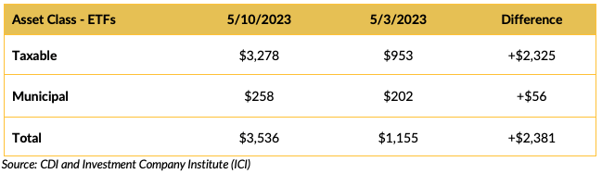

ETF Fund Flows (millions of dollars)

ETFs saw positive cash flows at a much faster rate than last week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply is expected to be moderate, with estimates slated somewhere around $8.5 billion.

CONCLUSION

Don't be fooled by the market as a strong indication of a Fed pause. A hike of 25 basis points could very much be on the table for June.

If you’re asking, “Is it the right time to buy bonds?” — our answer is “Yes.” But choose the strategy duration that best suits your needs.

Finally, debt ceiling negotiation is as much of an uncertainty now as it was when we started the month.

Due to the holiday, we will not publish our Week in Review next week — but look for our commentary the following week. Have a wonderful Memorial Day weekend.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.