.png)

WEEK ENDING 5/12/2023

Highlights of the week:

- Cash flow into money market funds continues.

- Know what’s in your money market fund.

- Latest data shows inflation moderating but still a long way off the trend.

A CITY DIFFERENT TAKE

We had two sets of inflation data released last week: CPI and PPI.

Year-over-year core CPI came in at 4.9%, below expectations of 5.0%. That was also lower than March’s unrevised 5.0%.

Year-over-year core PPI followed suit, coming in at 3.2%, below expectations of 3.3%, and March’s unrevised 3.4%. Both core measures are still well above the Federal Reserve’s 2.0% published target.

The fixed-income markets did not react much to these releases. Debt ceiling negotiations, or the lack thereof, grabbed the headlines.

CHANGES IN RATES

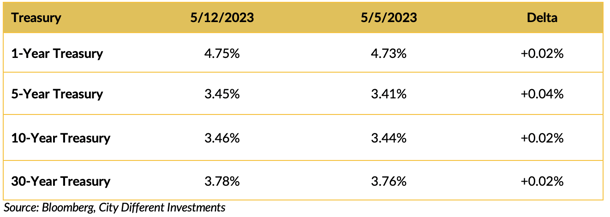

Yields on short Treasury securities were muted on the week. The real interesting stuff is happening in the short end of the Treasury market. The yield on the generic four-week Treasury bill reached a period high of 5.415% (February 8 – May 12), up 12.5 basis points on the week. The low for this generic security was 4.233% on March 17. Could this be an indication of the market's perceived risk of a government default? More on that later.

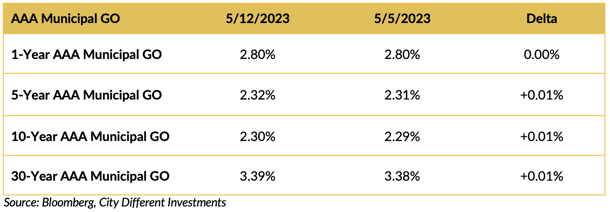

Yields in the municipal market were stable, raising only 0.01% on the week.

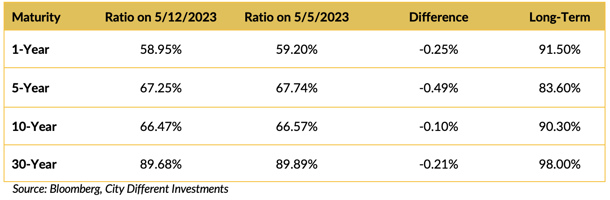

The muni/Treasury ratios moved marginally lower on the week. AAA general obligation municipal bonds in maturities greater than 5 years make sense for anyone in the 33% marginal tax bracket or higher.

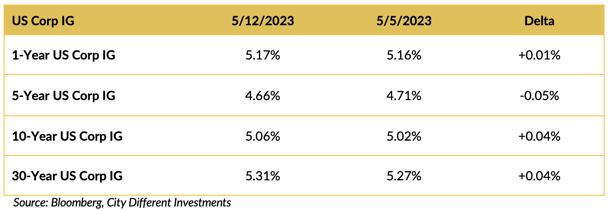

Yield in the investment grade (IG) corporate market moved marginally higher on the week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

The southern border is a mess that seems to be getting worse. The only thing worse than the fact that Congress can’t come up with a workable immigration policy is the debate on the debt ceiling!

The debt ceiling deadline is approaching. We’re 18 days away, and Congress is on recess. Congressional leaders and the president agreed to postpone a planned meeting this week and let their respective staffs work on potential solutions. We think that a government default is a low-probability event — but it’s a higher probability than ever before. Why? Because compromise in Congress also seems to be a low-probability event.

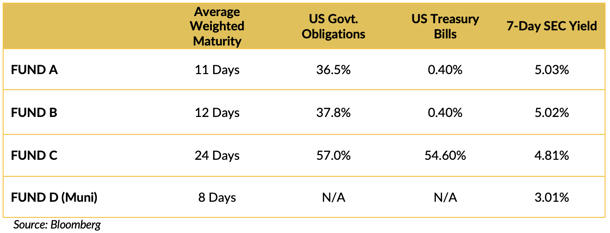

Several clients have asked what our thoughts are on this situation. First, we think that a Treasury investor's principal is safe, but may be delayed. We also believe money market funds are the most susceptible investment vehicle to negative volatility because they hold Treasury bills. Treasury bills are the very shortest government security issued. They are typically issued at a discount to par and paid back at par; the difference is the income or yield on the security. If a government default does occur (again, a low-probability event), any delay in payment will affect the income component that an investor would expect to earn. The additional risk to taxable money market funds is that market participants lower their bids on these securities to reflect an additional risk premium. How taxable money market funds react to these conditions depends on the amount and specific maturities of Treasury bills they own. Let's look at several significant money market funds without naming them.

As you can see from this minimal sample, a money market’s structure can limit the potential volatility under the worst debt ceiling outcome; municipal money market funds look to be the least susceptible to this volatility. Investors must decide what is more critical, yield or low volatility of their money market funds. This is an interesting conundrum, given the disintermediation the market has seen from bank accounts to money market funds.

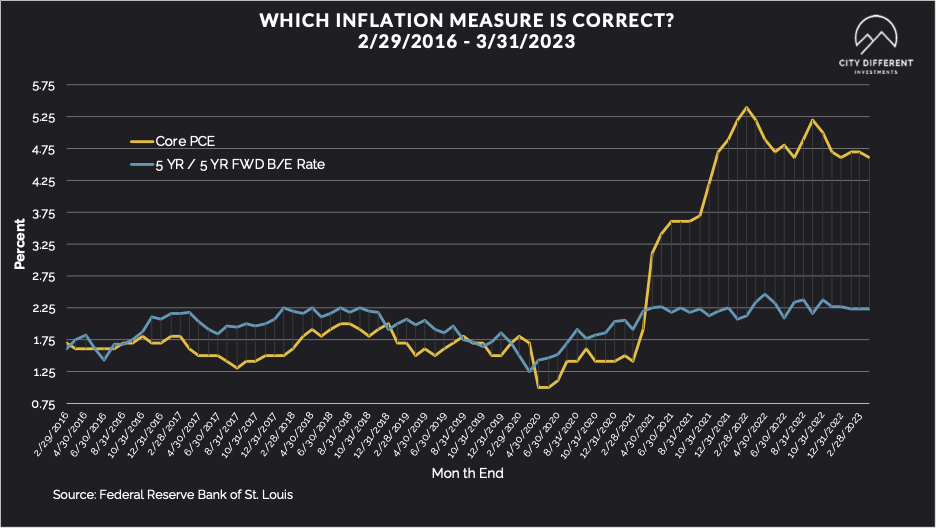

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended the week at 2.25%, 2 basis points higher than the May 5 closing of 2.23%. The 10-year Breakeven Inflation Rate ended the week at 2.18%, also 3 basis points lower than last week’s observation of 2.21%.

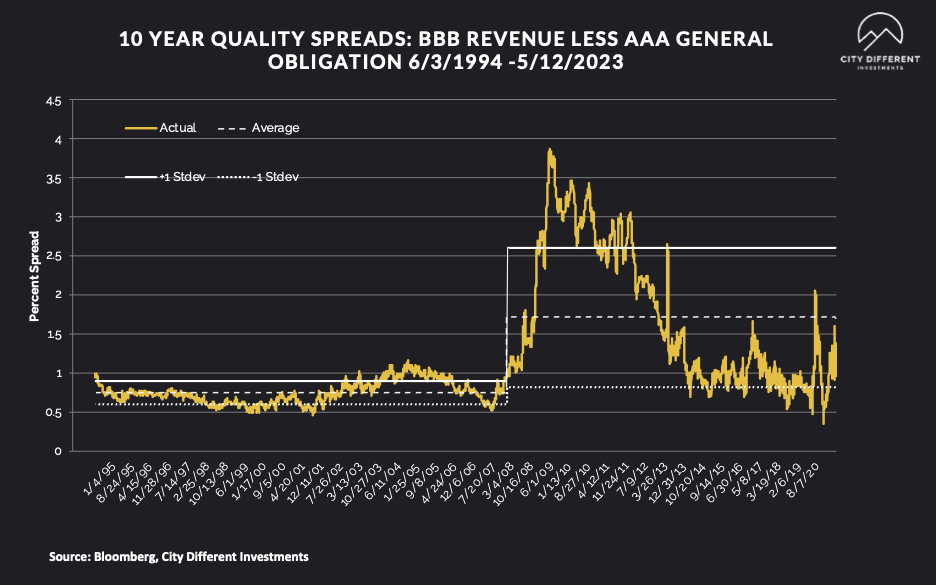

MUNICIPAL CREDIT

Most of the action was contained on the rates side for the municipal market. 10-year quality spreads (AAA vs. BBB) as of May 12 were at 1.20% (based on our calculations), 0.10% lower than last week’s 1.30%. The long-term average is 1.71%. By our way of thinking, lower-quality securities are still not attractive but are moving in the right direction.

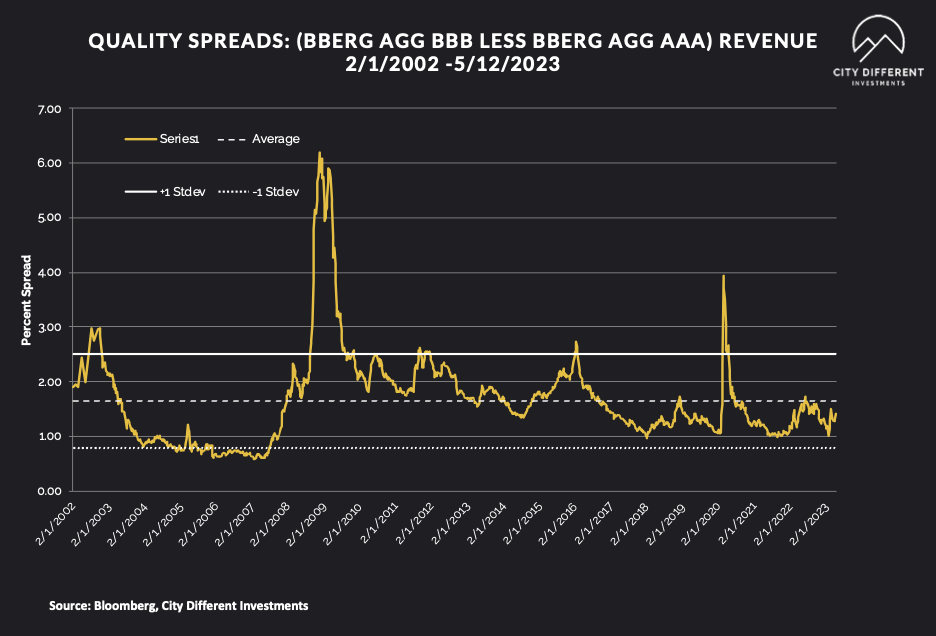

Quality spreads in the taxable market are not attractive but were stable last week, ending the week at 1.41%.

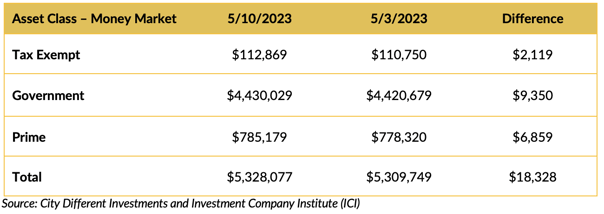

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds saw positive cash flows. Disintermediation continues; high money market yields are pulling cash out of bank deposits. This strategy is not without risk, as we outlined earlier.

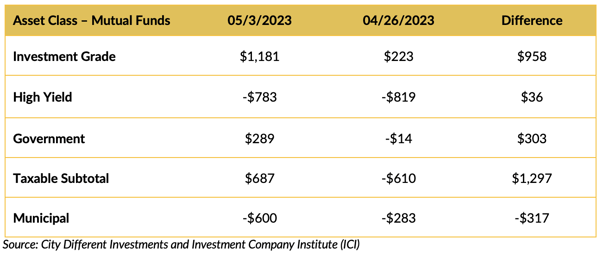

Mutual Fund Flows (millions of dollars)

Flows into bond funds are weak. Municipal bond funds continue to see withdrawals.

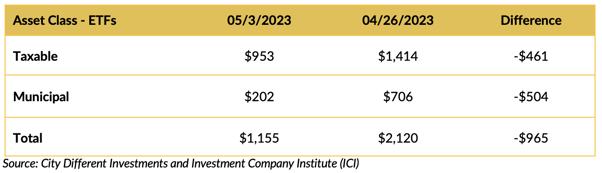

ETF Fund Flows (millions of dollars)

ETFs saw positive cash flows but at a slower rate than last week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply is moderate, with estimates slated somewhere around $6.8 billion.

CONCLUSION

Recent inflation measures show inflation moderating but still well above the Fed’s target. Debt ceiling negotiations have taken center stage and will add volatility in the markets. The disintermediation into money market funds may be impacted by these talks if a delay in payments materializes. We feel this is a low-probability event but one that is manageable if investors do a little homework. Know what your money market funds own!

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.