WEEK ENDING 3/3/2023

Highlights of the week:

- As we await March’s data, we make cases for both bull and bear markets.

The case for bear: a “reacceleration in interest rate hikes.”

The case for bull: a China reopening, disinflation trends, and corporate cost cutting. - Debt ceiling negotiations to come down to the wire.

- A question from our reader: “How do you position for a volatile bond market in 2023?”

A CITY DIFFERENT TAKE

March is an important month for economic data releases which could determine if January’s strength in data was an accident or a sustained trend.

We are awaiting key labor market numbers like nonfarm payrolls (which are expected Friday) along with ADP and JOLTs reports (expected earlier this week). On Tuesday, Federal Reserve Chairman Powell goes into his semiannual monetary meeting. CPI is released on March 14 and the FOMC meets again on March 22. All this plays into the possibility the Fed goes into its March meeting with two months of strong inflation data and strong jobs reports.

Since last autumn, we have maintained that the fogginess of the economic data and the strength of the labor market in the face of a restrictive Fed justify equal conviction to make cases for both bull- and bear-market scenarios. This underlines the slipperiness of current economic situations.

The Bull Case: The effect of China’s resurgence mostly tilts toward the bullish scenario. The growth target for China is modest, around 5%. China saw a rapid increase in consumer spending. In January, we saw the Fed and the market diverge in terms of prospective rates interpretation. Last month, Chairman Powell used the term “disinflation” in his post-meeting press conference. The Treasury market was overcome by dovish sentiments, but CDI disagreed with this interpretation. We heard no rate cuts this year. The market grabbed on to the notion that the Fed typically cuts six months after the last hike. Throw corporate cost cutting in the bull case scenario as well. Layoffs at Disney, Microsoft, Meta, and Netflix are showing some belt tightening. These job losses have a lag effect, translating about two months later.

The Bear Case: Former Treasury Secretary Lawrence Summers spoke about the possibility of a “re-acceleration in interest-rate hikes.” Summers stated, “The Fed right now should have the door wide open to a 50 basis-point move in March.” The market has priced in a 5.5% terminal rate. San Francisco Fed Governor Mary Daly iterated a higher-for-longer approach with the federal funds rate. Similarly, Richmond Fed President Barkin gave guidance of 5.5% to 5.75%.

Our team was out on the road speaking to advisors last week. We got a really smart question from an advisor who is also a reader of our weekly commentary. “I am not nervous about returns,” he said, “but how do I prepare my clients for 2023? Is it more of 2022? Is it a push-and-pull scenario like we saw in January and February of 2023?”

We go back to our equal conviction of bull and bear scenarios for the U.S. economy. We do think this is a good time to buy bonds (noting the inverted curve in the municipal and rates markets). The income in the short end of the curve does make cash reserves and short-term portfolios more interesting than they have been in years. We urge advisors to inspect the discipline and process of their third-party managers. In this time of volatility, it is the discipline of an investment manager that is put to the test. For CDI, our discipline is that of a total-return bond mandate. We believe in the active ladder management strategy. Despite the inverted yield curve, we do not believe in leaving any rung of the ladder empty. We have been actively overweighting the front end and underweighting the back end of our 1-to-10-year limited-term strategy (our preferred strategy for the current environment). We are long-term investors that believe the current fixed-income environment is right for dollar-cost averaging and reinvesting the ladder and its maturities in higher rates. Your risk management is also tested in this environment. We believe in actively monitoring the ratio of rate change to the change in the duration of our strategies.

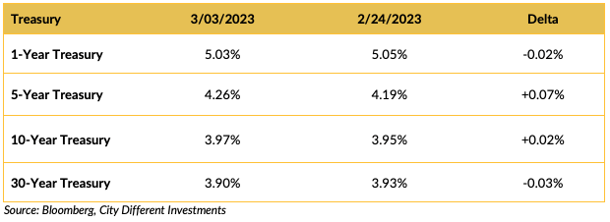

CHANGES IN RATES

Week over week, the Treasury market looked very quiet, mostly due to a strong Friday rally. This last week saw the 10-year Treasury rate stay around 4% for a considerable amount of time. The week also saw several Fed officials speak, and fourth-quarter unit labor costs came in much hotter than expected (3.2% vs. 1.6%) and hotter than the last release of 1.1%. Non-farm productivity was also a bit of a surprise; the Q4 reading was 1.7%, below expectations of 2.5% and below the prior reading of 3.0%. This combination does not bode well for future inflation.

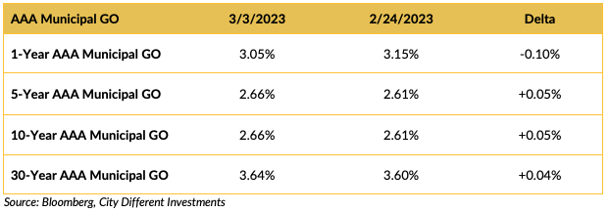

The municipal market followed the Treasury market to higher yields at about the same rate. Municipal rates did rally on Friday, along with Treasuries, but at a much slower rate. The anticipation of $10+ billion of new supply probably dampened the municipal market move.

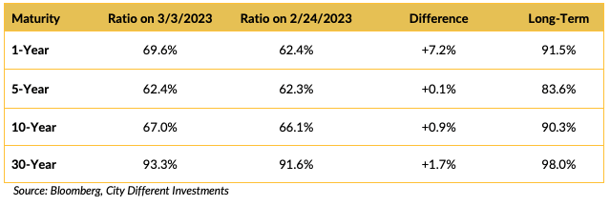

The above ratios and their weekly changes represent how the two fixed-income markets recorded such different reactions.

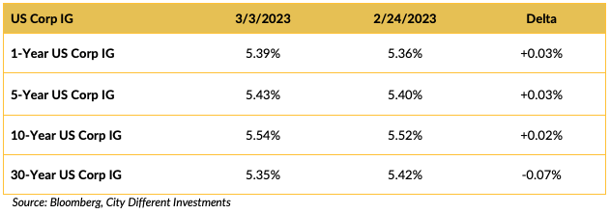

The investment grade (IG) corporate market shared the week's volatility.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Debt ceiling negotiations are still uncertain and reminiscent of 2011. We will likely see this go on until August when all extraordinary measures will be exhausted. Municipal credit that bears a direct link to federal funding will see some weakness and make for a good buying opportunity, much like 2011.

In other Washington news, former President Trump announced he will stay in the 2024 presidential race even if he is criminally charged.

Outside the U.S., two important geo-political issues are still staying strong.

- After seven months of fighting, victory in the Ukrainian city of Bakhmut would be a symbolic rather than strategic win for Russia.

- Adhering to the “One China” principle, President Xi Jinping laid out language for “peaceful reunification” with Taiwan. Meanwhile, Taiwan is on high alert for sudden entry by Chinese military into areas close to the Taiwan Strait.

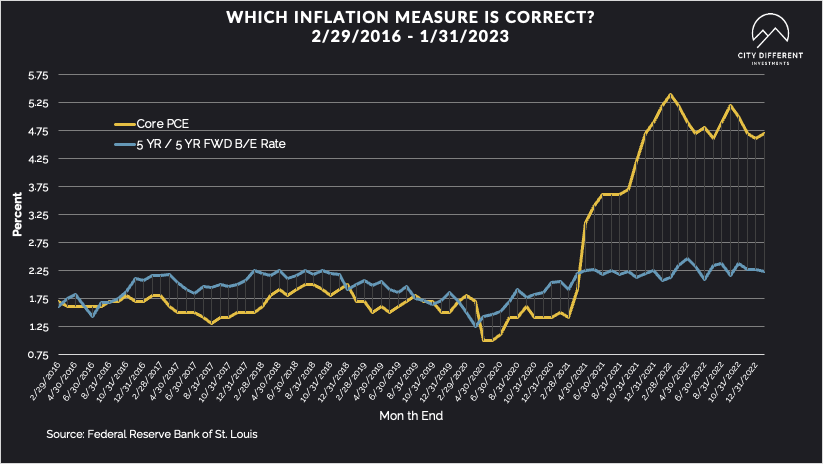

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended Friday at 2.33%, four basis points higher than the February 24 closing of 2.29%. The 10-year Breakeven Inflation Rate ended the week at 2.52%, 14 basis points higher than last week’s observation of 2.38%. This is the first week we have seen such a divergence in the moves of these two measures. Does this mean anything?

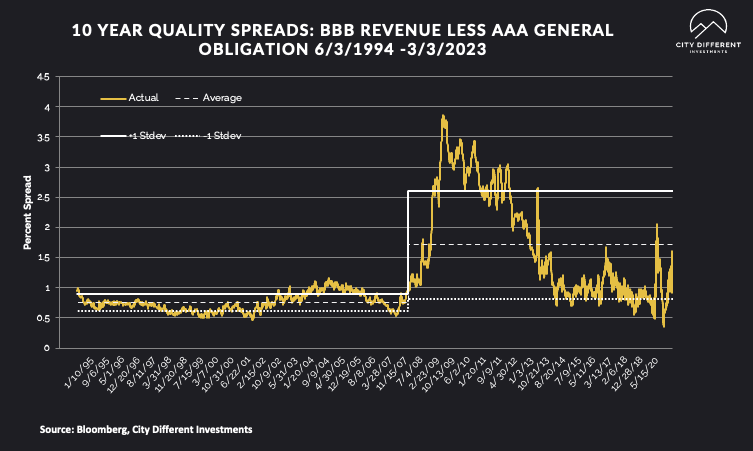

MUNICIPAL CREDIT

Municipal credit continued to be narrowed last week.

10-year quality spreads (AAA vs. BBB) were pretty much unchanged on the week, from 1.15% to 1.17% (based on our calculations). The long-term average is 1.71%. By our thinking, lower-quality securities are still not attractive.

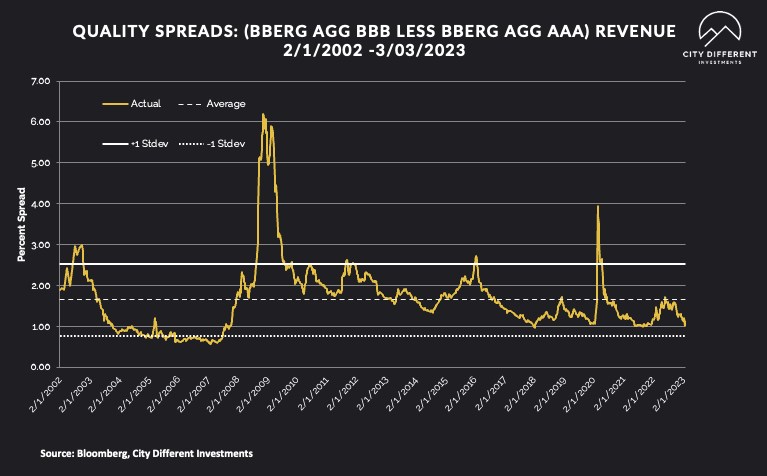

Quality spreads in the taxable market narrowed slightly, finishing at 1.15% vs. 1.02% last week.

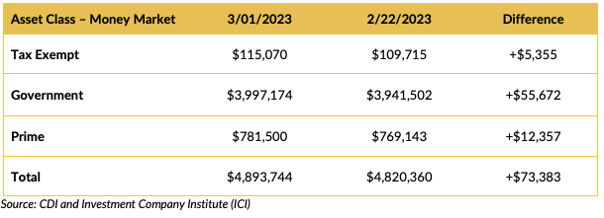

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

It looks like money market funds were popular last week. An inverted yield curve and volatility in the bond and equity markets go a long way to explaining this move.

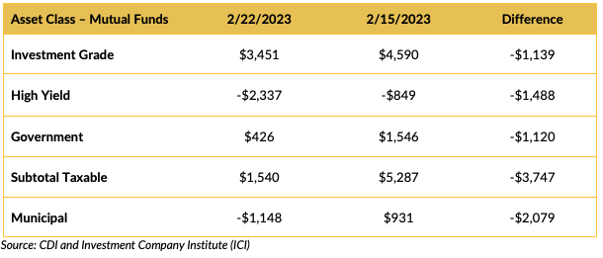

Mutual Fund Flows (millions of dollars)

Municipal bond funds shareholders showed a low tolerance for volatility.

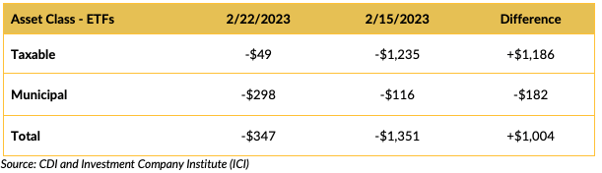

ETF Fund Flows (millions of dollars)

Other services that track mutual fund cash flows have reported negative flows for municipal bond mutual funds for the week ending March 1. This should be confirmed in next week’s ICI numbers.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Estimates for next week’s new-issue supply are around $10.8 billion

Total new issuance supply figures of $10 billion or more usually indicate weakness in new issue supply pricing (higher yields).

CONCLUSION

March is an important month for economic data releases. Pay special attention to CPI and labor market data. As we have said before, we can make a case for both a bull market and a bear market for this current economy. The debt-ceiling drama may go on until August. But if municipal bonds linked to federal funding see a credit weakness, this could make a good case to buy.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.