WEEK ENDING 3/24/2023

Highlights of the week:

- J. Thaddeus Toad would like to welcome you to another wild ride: the fixed-income market.

- Domestic and international banks have grabbed the headlines for another week. Don’t confuse correlation with causation.

- Oh, yeah. Before we forget, the Fed raised the federal funds rate range by 25 basis points.

A CITY DIFFERENT TAKE

The fixed-income markets moved around with great speed this week. Every day brought about a new problem/solution, it seemed. As the fervor about Silicon Valley Bank and First Republic Bank began to subside, the Credit Suisse issues grabbed the headlines. Those issues seemed resolved when UBS came to the rescue (with government sweeteners). Then on Friday morning, we woke up to a significant Treasury rally on the news that the spreads on Deutsche Bank’s credit default swaps blew out. Credit default swaps and the incumbent counterparty risks were significant drivers of the 2008 banking crisis, a real systemic crisis unlike this idiosyncratic one.

On Wednesday, Treasury Secretary Janet Yellen addressed a Senate committee, and Federal Reserve Chairman Jerome Powell announced the results of the two-day Fed meeting. Both tried to reassure the public that the U.S. banking system was "sound and resilient."

Oh, yeah. Before we forget, the Fed raised the federal funds rate target by 25 basis points and hinted that there might be only one more Fed action in the offing. Powell hedged this position by pointing out that the sticky portions of the Fed’s favorite inflation measure account for 56% of the core PCE. We interpret this to mean that the Fed’s 2.00% inflation target may prove difficult to achieve. In addition, this brings into question the validity of the various breakeven inflation measures. See below.

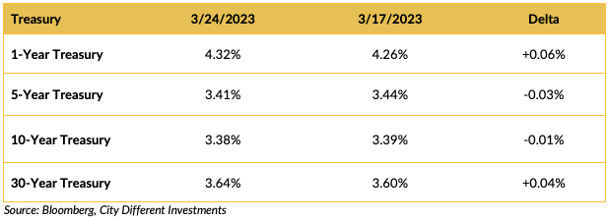

CHANGES IN RATES

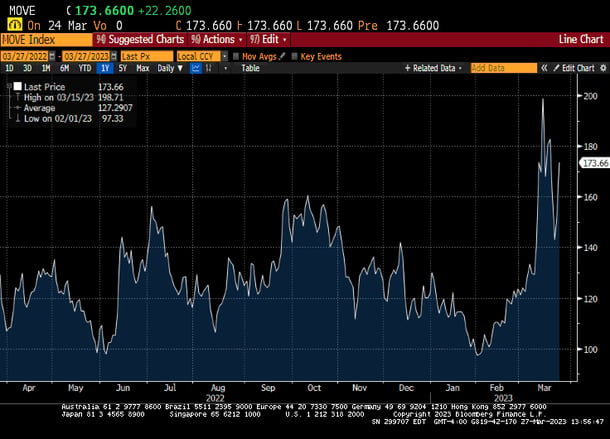

The week-over-week changes in Treasury yields suggest that a calm has befallen the Treasury markets, but that would be misleading. The 10-year Treasury rate reached 3.59% on March 21, up from 3.39% on March 17, before falling to its closing value of 3.38%. Bank of America calculates a volatility index for the Treasury market called the MOVE Index (see below).

As you can see, the last couple of weeks have been a wild ride.

As you can see, the last couple of weeks have been a wild ride.

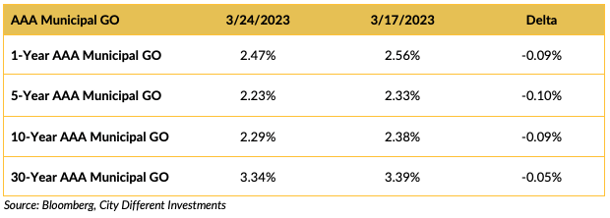

The municipal market also seemed to calm down. Underlying this performance is the lack of supply brought about by the increased volatility in the Treasury market and news flow from the banking sector.

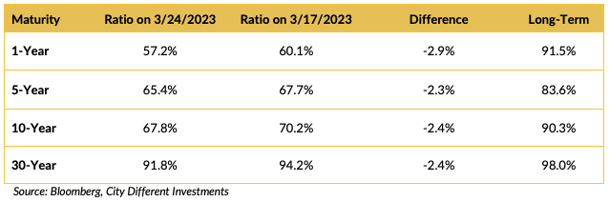

Relative to the Treasury market, municipal bonds are more expensive, as the decrease in the yield ratio indicates.

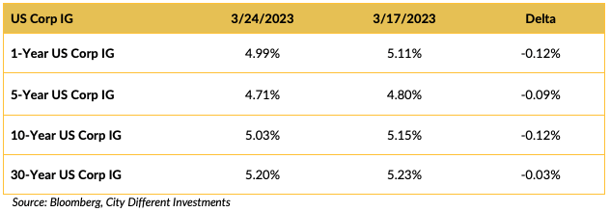

Yield in the investment grade (IG) corporate market moved lower on the week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Wednesday brought about a turn of events typically avoided in Washington — the chairman of the Federal Reserve and the secretary of the Treasury speaking publicly at the same time on policy.

Both tried to calm and reassure American depositors. (Bank runs, at their core, are rooted in psychology and fear.)

Treasury Secretary Janet Yellen discussed the Treasury’s role:

“Yellen told a Senate committee that she's not considering expanding the FDIC's insurance limit of $250,000.

“[We’ve] not considered or discussed having anything to do with a blanket insurance or guarantees of all deposits,” she said in response to a question.

Yellen, however, said that if there’s a contagious bank run, the Treasury would likely pursue an exception that would permit the FDIC to protect all depositors of the failed banks. This would be considered on a case-by-case basis, she told senators.”

At the same time, Federal Reserve Chair Powell did his best to calm depositors' fears:

“Chairman Jerome Powell addressed the turmoil in the U.S. banking sector, saying the issues were limited to a few banks and emphasized the broader financial system was "sound and resilient."

However, both Powell and Treasury Secretary Janet Yellen, in simultaneous testimony, stopped short of saying they'd do whatever it takes to save all depositors. Those comments roiled markets.”

However, Powell did go further to address inflation concerns:

”Powell noted that inflation in prices for goods has been coming down for several months, while housing-services disinflation was a matter of time, as new leases are signed. Those two categories together are responsible for 44% of the core personal consumption expenditures price index—the Fed’s preferred inflation measure.

It is the remaining 56% that remains stubbornly inflationary. Powell said that he is seeing less progress in the non-housing services elements of the PCE basket, which are closely tied to wages. Getting disinflation there may take some softening of consumer demand and labor-market conditions, he said.”

We will find out how sticky core PCE is on Friday.

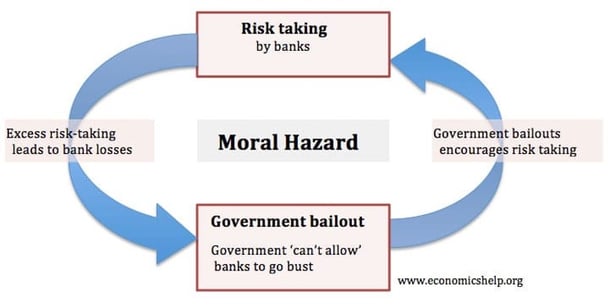

Policymakers are trying to tread a fine line to prevent a mass exodus of depositors from banks with concentrated and highly correlated depositor bases mixed with the additional problem of poor risk management. Classifying duration-rich investments as “held to maturity” adds to a bank's bottom line; owning shorter maturity securities in an era of near-zero interest rates reduces the bottom line. Hedging duration-rich securities incurs a cost that reduces the bottom line.

The other policy imperative is how to allay these fears without creating a moral hazard. A moral hazard is defined as a “lack of incentive to guard against risk where one is protected from its consequences, e.g., by insurance.”

Both Yellen and Powell assure the public that the banking system is “sound and resilient.” It sounds like we have “nothing to fear but fear itself,” — and we agree.

WHAT, ME WORRY ABOUT INFLATION?

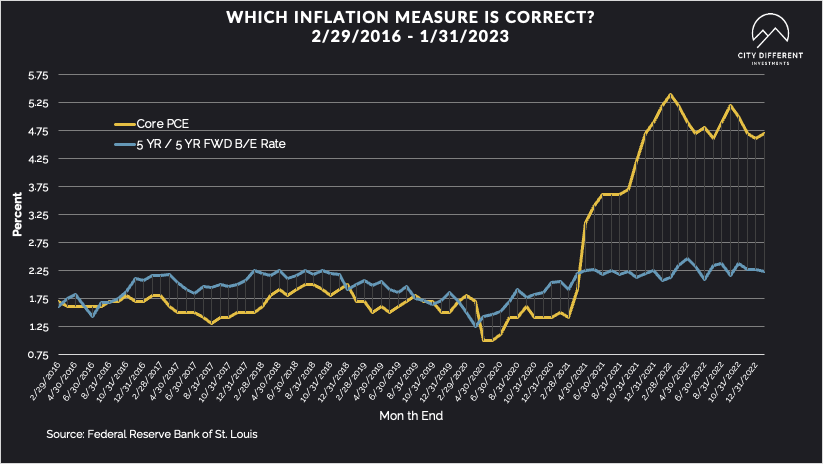

A client asked us last week to explain the 5-Year, 5-Year Forward Inflation Expectation Rate (a long form of the 5-year Breakeven Inflation rate). We get this time series from the St. Louis Fed. They define this series as “a measure of expected inflation (on average) over the five-year period that begins five years from today.” As you can see from the above chart, a significant difference has developed between this measure and the Fed’s favorite inflation measure, core PCE.

The 5-year Breakeven Inflation Rate ended Friday at 2.23%, 13 basis points higher than the March 17 closing of 2.10%. The 10-year Breakeven Inflation Rate ended the week at 2.22%, 12 basis points higher than last week’s observation of 2.10%.

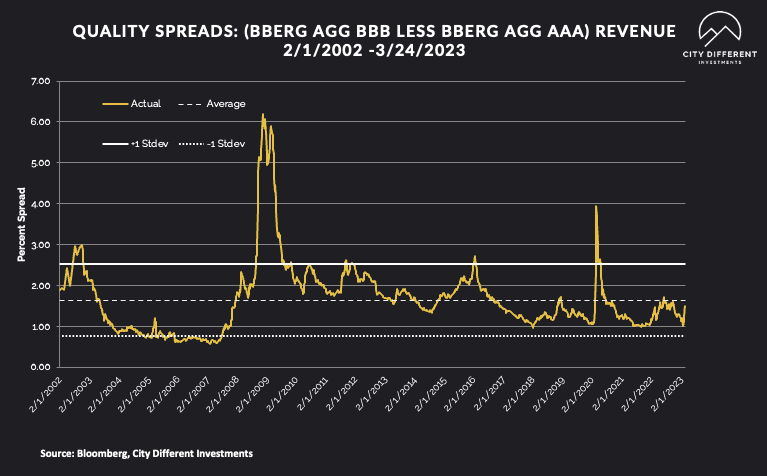

MUNICIPAL CREDIT

Municipal credit last week.

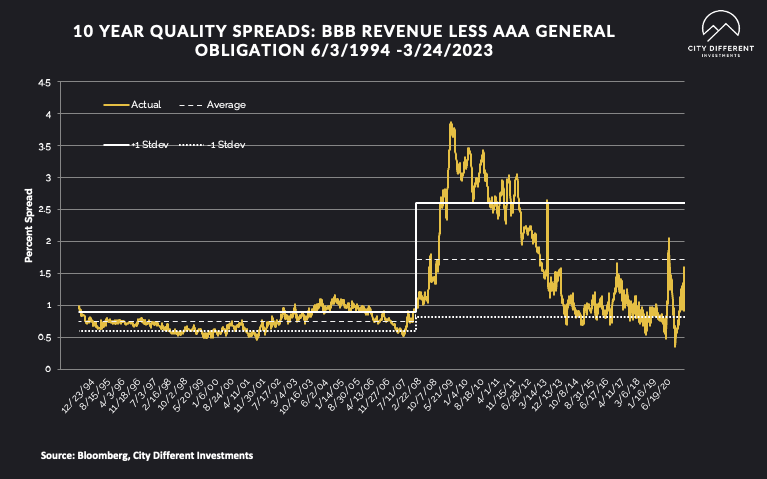

10-year quality spreads (AAA vs. BBB) were unchanged on the week (1.21%) based on our calculations. The long-term average is 1.71%. By our way of thinking, lower quality securities are still not attractive.

Quality spreads in the taxable market maintained their wider spreads this week. Ending the week at 1.47%, 3 basis points lower than last week’s 1.50%.

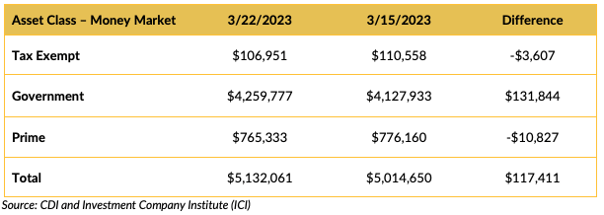

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market funds saw positive cash flows last week, especially government money market funds. Return of capital sometimes trumps return on capital.

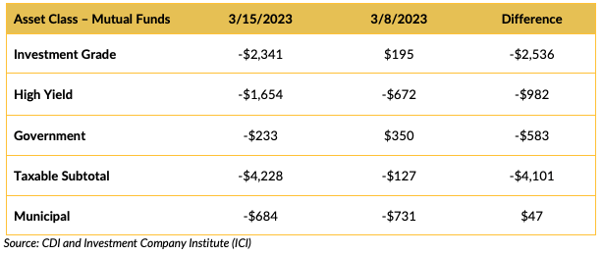

Mutual Fund Flows (millions of dollars)

It looks like no one liked bonds last week. Can you blame them? Negative cash flow into municipal bond mutual funds, while still negative, slowed a bit.

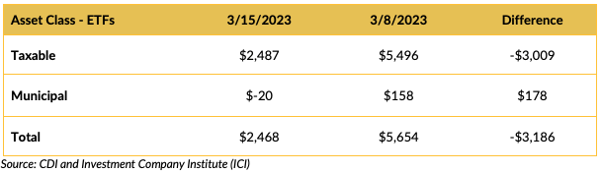

ETF Fund Flows (millions of dollars)

ETF fund flows for the week of March 15 were down from the prior week but remained positive overall.

Other services that track mutual fund cash flows have reported negative flows for municipal bond mutual funds for the week ending March 22. This should be confirmed in next week’s ICI numbers.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Estimates for next week’s new issue supply are around $7.3 billion.

Total new issuance supply figures of $10 billion or more usually indicate weakness in new issue supply pricing (higher yields).

CONCLUSION

Folks, buckle your seatbelts and keep your arms and legs inside the vehicle at all times. It looks like we will be on the “wild ride” of fixed-income volatility for some time. In this environment, we will maintain our neutral duration targets and rely on our discipline to make further investment decisions. We believe that is good advice for any investor in volatile times.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.