.png)

WEEK ENDING 3/17/2023

Highlights of the week:

- Condolences to all of you with busted NCAA brackets; maybe not the only things busted…

- Our overview of the idiosyncratic banking failures and Bank Term Funding Program.

- Does rate-cycle tightening have an end in sight?

- Common themes in banking failures are undiversified investor bases and lack of risk management.

- Trivia question: What was the largest U.S. bank to fail? Answer at the end of our weekly commentary.

A CITY DIFFERENT TAKE

This week, we’re recapping the situations of the failed (or failing) banks from this week’s headlines. Each troubled bank’s story has been idiosyncratic. However, the big theme that has emerged is that banking troubles have arisen as an unintended consequence of low interest rates and quantitative easing.

Currently, the severely inverted yield curve is giving banks some heartburn. U.S. banks have a new reality: an asset-liability mismatch created by the Federal Reserve’s tightening cycle. The Federal Reserve must factor in the current situation of fighting inflation without causing bank collapses. Also, the bookend of this story is that the Fed is moving closer to the end of the rate hike cycle.

The bank failures caused an interesting trend in the bond market where we saw the biggest drop in two year rates since October of 1987. At City Different, we interpret the drop in rates to be reflective of the market pricing in an end of the tightening cycle. But the market has proven to be wrong earlier in the year. Without much speculation, with regards to the daily gyrations in the market, we advise our readers to pay attention to what the Federal Reserve has to say later this week.

How is this different from 2008?

The big difference is that the market doesn’t have to worry about many counter-party risks. For the U.S. banks, this is an asset and liability matching issue. Depositors can walk out the door, and the banks must fund these withdrawals by selling long-duration securities. This is very painful after interest rates have increased so much. The poor investment and risk management decisions of management are coming home to roost! The Treasury, Federal Reserve, and the Federal Deposit Insurance Corp. have shown quickness in response to prevent any spillover of these “idiosyncratic bank failures” to the wider economy.

Now let’s look at each unique situation:

Silvergate Capital

Silvergate was an important bank for the crypto industry. It was a California-based community bank launched in 1996 that moved into crypto in 2013. With crypto growth big stakeholders like Blackrock and Citadel announced investments in Silvergate. This legitimized the potential of its instant payment platform that enabled it to send money to depositors when traditional banks were closed on weekends. Excitement circulated on the bank’s potential to issue stablecoin. The bank was facing several lawsuits in connection to the FTX scandal. Earlier this month Silvergate announced a delay in filing its annual report to the SEC and reported a $1 billion loss for its fourth quarter. Investors withdrew money and last week the bank liquidated. This banking failure preceded Silicon Valley Bank’s collapse by two days.

Silicon Valley Bank

The second-largest banking failure in U.S. history. With an undiversified investor base of tech founders, startup funding money, and private equity this was indeed a unique bank that catered to distinctive solutions for the tech industry. With funding drying up in the tech world last year, the depositor base were companies that were burning cash or, in non-startup words, spending cash.

As we mentioned in last week’s commentary, SVB’s uniqueness was also in its higher-than-average noninsured deposit base and higher bucket of fixed-income securities that were held to maturity which had to be marked down to reflect the new fixed-income reality. This was a failure of the bank’s asset-liability management committee and its chief risk officer.

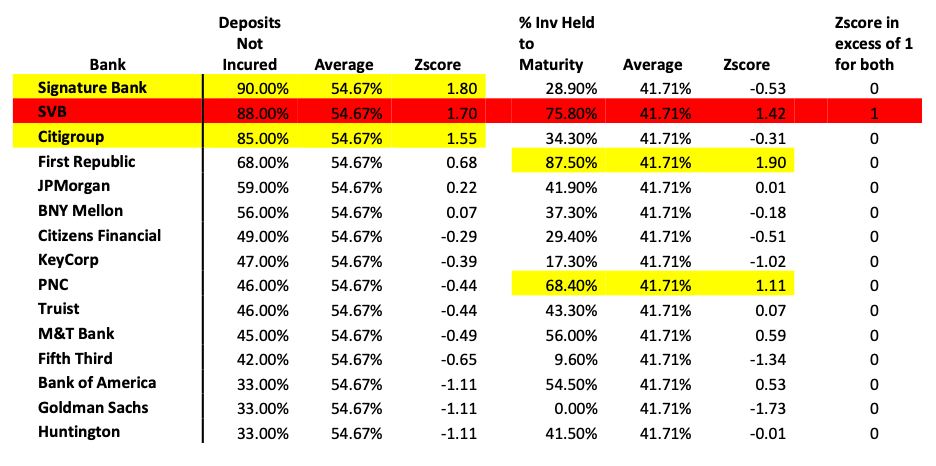

We must also note the insured vs. uninsured deposit base. Prior to 2023, not much analysis has been performed on the uninsured deposit base. Currently, the FDIC guarantees $250,000 for an individual and $500,000 for a couple’s joint deposit in a bank. Any amount above that is uninsured. We looked at the sample ranking for some of the largest banks, based on the percentage of total deposits not FDIC insured. We calculated the number of standard deviations (average variability from its mean) from each institution's mean (average). We then performed the same analysis for the percentage of investments “held to maturity” on the balance sheet as of December 31, 2022.

Any institution more than +1 standard deviation off the mean was highlighted in yellow. Any institution with a measure of more than +1 standard deviation in both categories was highlighted in red. See the table below:

Source: Business Intelligence, City Different Investments calculations

Here is our big takeaway from our brief Statistics 101 interlude: a bank run is based on fear. Given the factors that pushed SVB into the nanny state’s arms, psychology is a bigger factor than math.

We do not think this is a systemic problem.

On Friday, March 18, SVB filed for bankruptcy. The rumor is that the FDIC is now looking to break the bank into two parts and sell it.

“The only thing we have to fear is fear itself.” — Franklin D. Roosevelt

Signature Bank

Quickly behind SVB, Signature Bank was the third-largest bank to fail in the U.S. Signature was a growth bank, which put customers first with very little red tape (read due diligence) to open customer accounts. Clients ranged from commercial real estate businesses to crypto firms. In 2022, 27% of Signature’s deposits were from digital asset clients. With the FTX failure, Signature took a big hit against its crypto deposit base. Here the problem was an esoteric and small depositor base that quickly lost confidence in the bank. As soon as SVB and Silvergate collapsed, depositors started withdrawing money from Signature Bank. The bank went to the Federal Home Loan Bank of New York which could not meet Signature’s request in the few hours that it took for Signature’s client base to withdraw $18 billion or 20% of the lender’s total deposit. It was a crisis of confidence that New York regulators quoted as they shut down the bank.

Credit Suisse

At the time of this writing, there is news of UBS buying Credit Suisse for more than $3 billion. (As of March 10, UBS had a market cap of $65 billion and Credit Suisse had a market cap of $8 billion). The deal, engineered by Swiss regulators, aims to save confidence in the banking system. Swiss National Bank has offered UBS around $100 million in liquidity. The rumor is UBS would hold on to the valuable wealth management and asset management arm of Credit Suisse and spin off its local Swiss operations into an independent entity. According to the Wall Street Journal, a combined bank would be a “behemoth” holding around 30% of Swiss domestic loans and deposits.

Impact on Bonds:

Credit Suisse’s fixed-income book is expected to be substantially written down, impacting bonds.

First Republic Bank

The biggest U.S. banks agreed on March 16 to contribute $30 billion in deposits to First Republic Bank to stabilize the lender which relies heavily on uninsured deposit funding. Investors speculated the bank could be the next to fail.

Impact on Bonds:

Moody’s has downgraded the bonds to B2/negative and S&P assigned a B+ rating. Fitch has the bonds at BB- negative. As of Friday, First Republic 4.375% 2046 were trading at $62.

Overview of Bank Term Funding Program

The Bank Term Funding Program offers loans of up to one year to banks, savings associations, credit unions, and other depository institutions pledging U.S. Treasuries, agency debt, mortgage-backed securities, and other qualifying assets as collateral, which will be valued at par. The motivation is to save banks like SVB which had to sell their assets at a loss to meet cash withdrawals from depositors. The sharp rise in interest rates has caused big losses in bank portfolios that are currently paper losses. But if they attempt to sell, it materializes in a mark-to-market situation, leading to a substantial loss and a true reflection of the current fixed-income market.

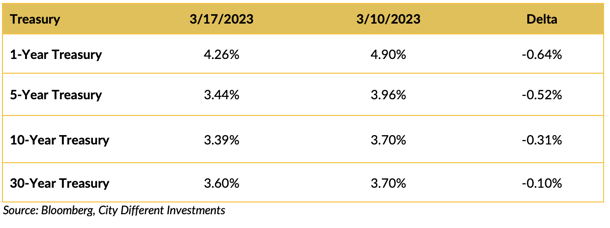

CHANGES IN RATES

Volatility has continued to roil the Treasury market. One day you are a hero, and the next, the opposite. The fixed-income and equity markets are still trying to figure out what the trouble with Silicon Valley Bank and First Republic Bank means.

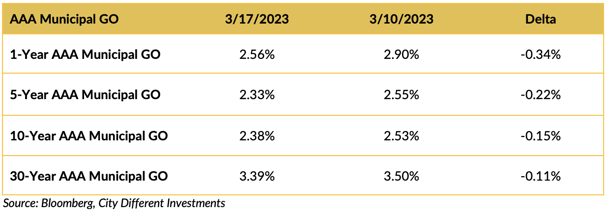

The municipal market followed the Treasury lower in yields but and a much slower pace. We know most of our readers will be shocked by this revelation!

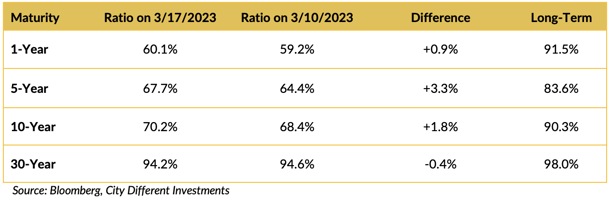

The change in ratios was small and mixed depending on the maturity.

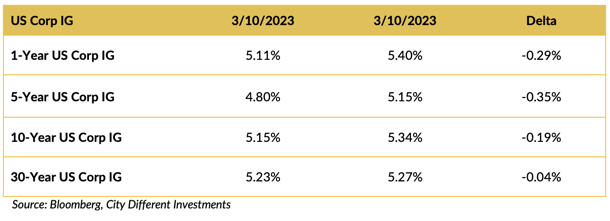

The investment grade (IG) corporate market shared the week's volatility.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Nanny state to the rescue. Funny how many people with libertarian leanings love government intervention when their ox gets gored.

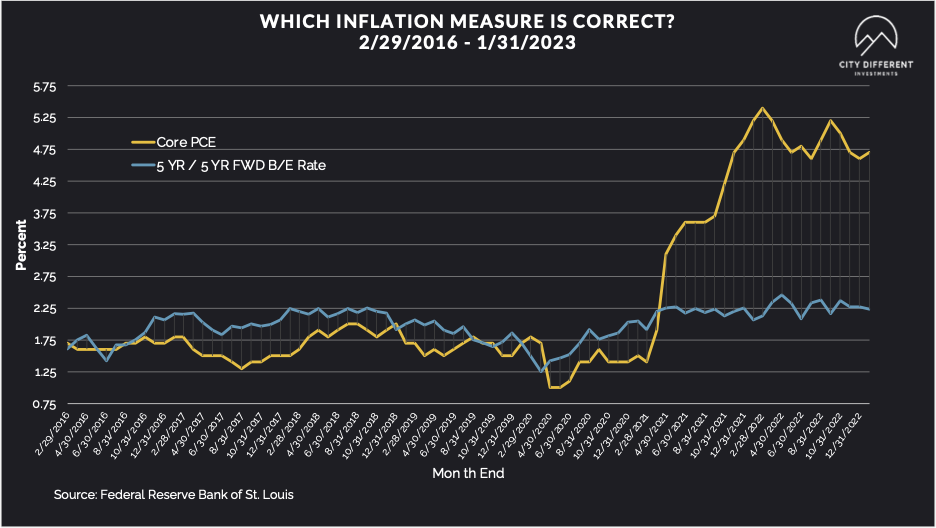

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended Friday at 2.10%, 8 basis points lower than the March 10 closing of 2.18%. The 10-year Breakeven Inflation Rate ended the week at 2.10%, 16 basis points lower than last week’s observation of 2.26%.

MUNICIPAL CREDIT

Municipal credit continues to be narrowed last week.

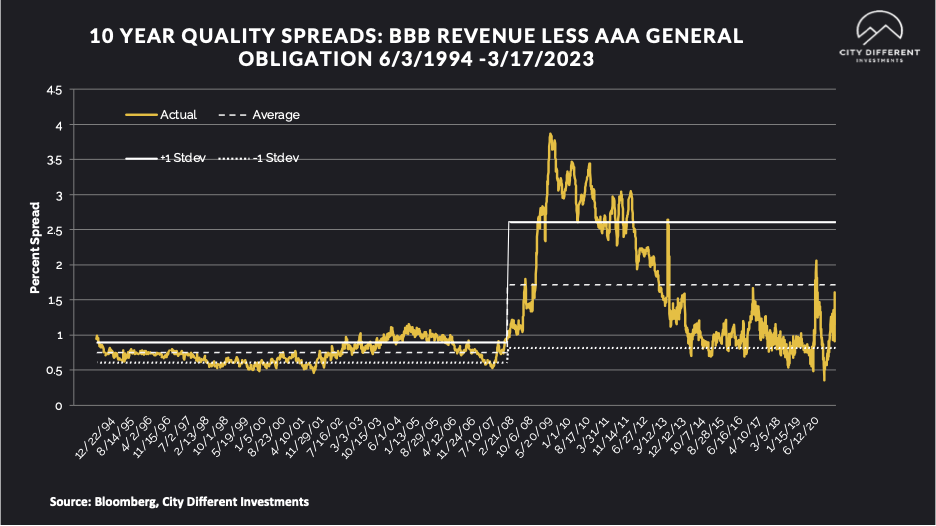

10-year quality spreads (AAA vs. BBB) were effectively unchanged on the week from 1.21% to 1.22% (based on our calculations). The long-term average is 1.71%. By our way of thinking, lower quality securities are still not attractive.

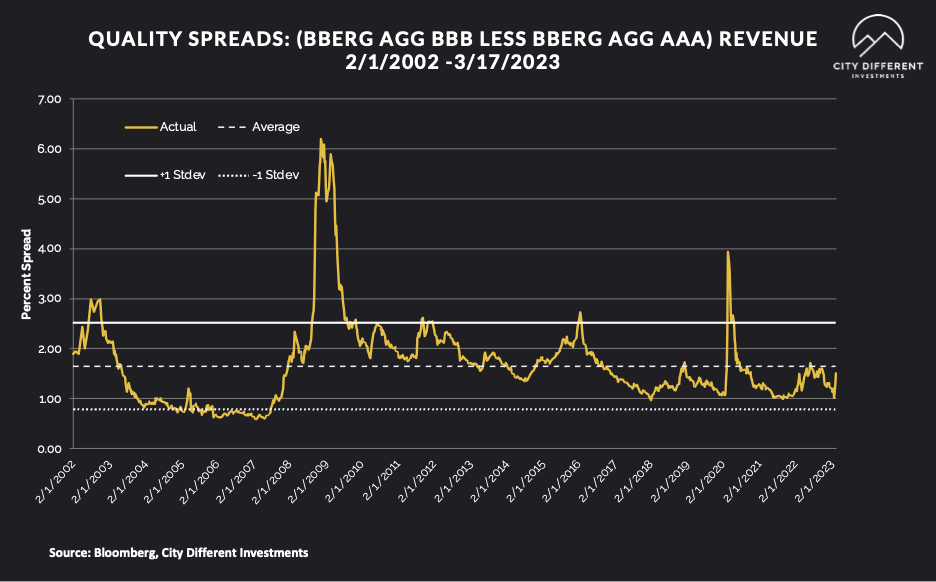

Quality spreads in the taxable market widened from 1.27% to 1.50%. Flights to quality have a tendency to do such things.

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

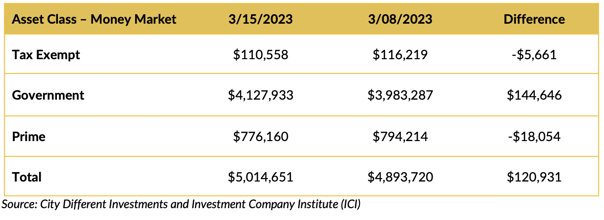

Money Market Flows (millions of dollars)

Money market funds (especially government money market funds) saw positive cash flows last week. Again, flights to quality tend to do such things.

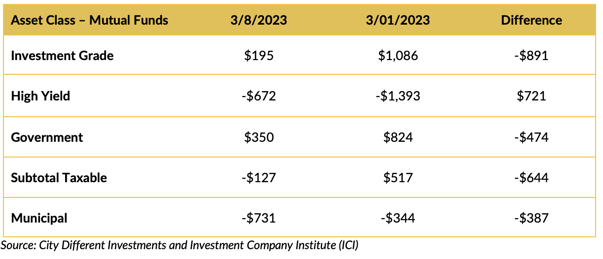

Mutual Fund Flows (millions of dollars)

Municipal bond funds shareholders withdrew funds for another week.

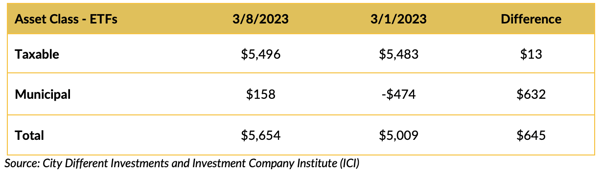

ETF Fund Flows (millions of dollars)

Other services that track mutual fund cash flows have reported negative flows for municipal bond mutual funds for the week ending March 8. This should be confirmed in next week’s ICI numbers.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Estimates for next week’s new issue supply are around $5.3 billion.

Total new issuance supply figures of $10 billion or more usually indicate weakness in new issue supply pricing (higher yields).

CONCLUSION

Remember our trivia question “What was the largest bank to fail in U.S. history?” The answer is “Washington Mutual” in 2008.

Thank you for reading this week’s commentary which was more of a situational breakdown for all the banks grabbing headlines. When you assess individual situations for these troubled banks, they do look unique. However, the broader takeaway is these banks saw the pitfalls of asset liability mismatch, a non-diversified investor base, and lack of risk controls.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.