WEEK ENDING 3/10/2023

Highlights of the week:

- Silicon Valley Bank fails due to poor diversification in its depositor base and too much duration in its fixed-income portfolio.

- We do not believe this is systemic, but the Wall Street Journal reported on Friday of at least two other California-based regional banks with the same risk profile: First Republic and PacWest Bancorp.

- If SVB suffered an old-fashioned run, the fixed-income market’s reaction was an old-fashioned flight to quality.

- CPI and PPI are released this week.

A CITY DIFFERENT TAKE

We expected to be writing about the Friday jobs release, but Silicon Valley Bank (SVB) — a regional bank catering to California tech, startups, and venture capital firms — took the spotlight by collapsing last week. The failure of SVB was spectacular, not only because of why it happened but because of the sheer speed of the collapse. SVB suffered from two risks:

- Its depositor base was not diversified, and the liquidity needs of this base were correlated in a way that when one segment needed its cash, they all did.

- SVB had too much duration in its investment portfolio; stretching for income is not just a retail investor sin.

This does not represent a systemic risk to the banking system, and the need or desire for a government bailout is limited regionally.

From everything we know (as of late Sunday afternoon), we believe the markets should recover from Friday’s panic to focus on CPI and PPI. We do not see why Friday's isolated bank failure should change the Fed’s strategy going forward, although it increases the odds of a 25-bps increase in the overnight rate (vs. a 50-bps increase).

There are several strategies to help investors avoid the problems presented by SVB. We would be glad to share them, so give us a call.

Monday Morning Update:

Chris Ryon: Stop the presses! Monday morning, we learned the government has come in to do a non-bailout bailout. The Wall Street Journal has an excellent explanation of what has transpired in its opinion sector. (As Hardy would say to Laurel, “This is another fine mess you’ve gotten us into.”)

President Biden spoke this morning to reassure Americans that the banking system is safe. In summary, all bank depositors (insured or otherwise) will have access to all their money this morning. The president claims this is not a bailout, but we think he “doth protest too much.” Troubled bank management will be fired. Is that before or after they have sold their stock? Reports from this weekend infer that high-ranking SVB bank officers sold stock on Thursday.

Our take is that this is bad policy! The governor on excessive risk-taking is the risk of loss. Once the risk of loss is limited, what is there to stop excessive risk-taking? As the risk-taking grows, the potential problem for policymakers grows until it becomes systematic.

These great risk-taking entrepreneurs benefit from government largesse such as carried interest and now are offered cover for their bad financial decisions. The nanny state is to be derided until you find yourself in a crisis; then, a hug from the nanny state is a good thing!?

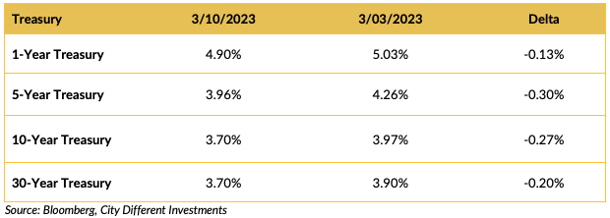

CHANGES IN RATES

If you believe (as we do) that the hard times that have befallen Silicon Valley Bank are isolated and highlight the need for a diversified depositor base and better interest rate risk management, then what happened Thursday and Friday was an old-fashioned “run on the bank” (exacerbated by electronic funds transfer protocols). In response, the fixed-income markets experienced and old-fashioned “flight to quality.” Investopedia defines a flight to quality as:

“Flight to quality occurs when investors in aggregate begin to shift their asset allocation away from riskier investments and into safer ones, for instance out of stocks and into bonds.”

Think of it as an investor/depositor stampede. What is the best thing to do if you find yourself in a stampede? Get out of the way!

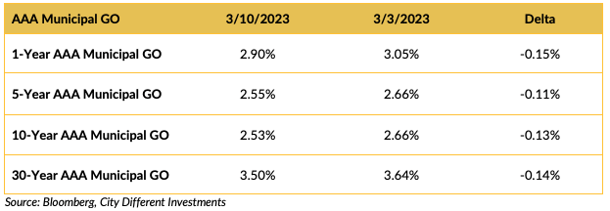

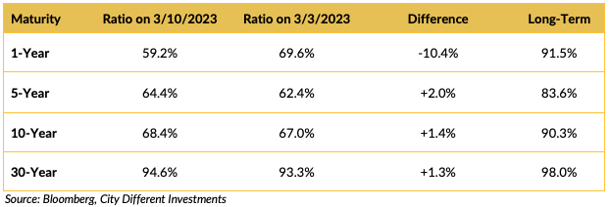

The municipal market followed the Treasury but at a much slower pace — except for the one-year maturity, which matched the Treasury market’s move to lower yield.

As noted above, the one-year maturity of the municipal market matched the Treasury market's move to lower yield, resulting in a much larger percentage move in the ratios.

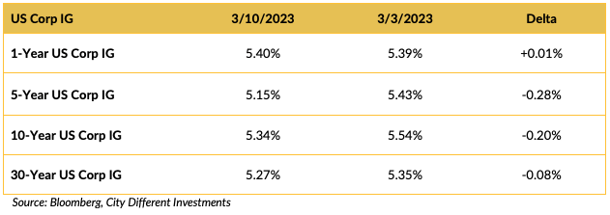

The investment grade (IG) corporate market shared in the week's volatility.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Silicon Valley Bank’s collapse has everyone's attention this week. One representative from SVB's congressional district called for a government bailout of all depositors, not just those within the FDIC guidelines. Until today, we viewed this as a low-probability event because SVB’s collapse, while sad for those involved, is not systemic to the banking system. Such a move would bring into question a “moral hazard.” If the government bails out all those who make bad decisions, what are the risks of making a bad decision?

It was reported by Bloomberg on Sunday afternoon that the FDIC kicked off an auction process late Saturday night for SVB, with bids due by Sunday afternoon. Given the short time frame and all the unknown risks associated with the collapse, do the Feds really expect a bid better than JP Morgan's bid for Bear Stearns at $2.00 per share? There does not seem to be ample time for proper due diligence. If any bank wants to grab SVB’s tech and private equity lending business, it seems a safer strategy would be to have bankers on their way to Silicon Valley loaded with workout deals.

In our estimation, selling SVB’s portfolio and allocating it to depositors is a better course of action. One aside: it was reported that a high-ranking officer sold millions of dollars of shares on Thursday. Now there’s a captain going down with the ship.

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended Friday at 2.18%, 15 basis points lower than the March 3 closing of 2.33%. The 10-year Breakeven Inflation Rate ended the week at 2.26%, 26 basis points lower than last week’s observation of 2.52%.

We had someone stop by the office last week and ask us about this chart. So, we took a deeper dive into this relationship. We calculated the six-month correlations of these two time series on a nominal basis, a first-difference basis, and a relative first-difference basis. Our results were nominal correlation of -0.09, first-difference correlation of -0.35, and relative first-difference correlation of -0.34. The result of all this math is to use Core PCE when judging real yields because that is what we see and feel (not to mention it’s the Fed’s favorite inflation measure).

MUNICIPAL CREDIT

Last week, municipal credit continued to narrow.

10-year quality spreads (AAA vs. BBB) widened on the week from 1.17% to 1.22% (based on our calculations). The long-term average is 1.71%. By our way of thinking, lower quality securities are still not attractive.

Quality spreads in the taxable market widened slightly, finishing at 1.27% vs. 1.15% last week.

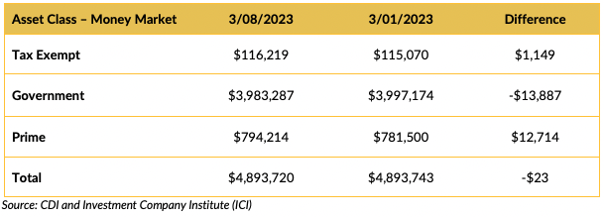

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Not a big change in overall money market balances — more of a reconfiguration of the deck chairs.

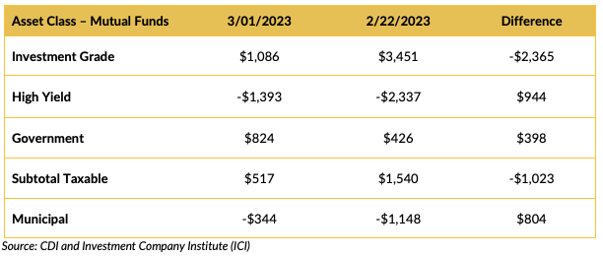

Mutual Fund Flows (millions of dollars)

Municipal bond funds shareholders withdrew funds for another week.

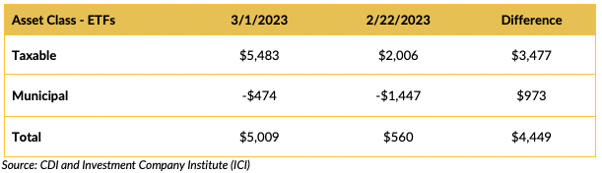

ETF Fund Flows (millions of dollars)

Other services that track mutual fund cash flows have reported negative flows for municipal bond mutual funds for the week ending March 1. This should be confirmed in next week’s ICI numbers.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

Estimates for next week’s new issue supply are around $7.6 billion.

Total new issuance supply figures of $10 billion or more usually indicate weakness in new issue supply pricing (higher yields).

CONCLUSION

We expected to be writing about the February jobs numbers this week. (Oh, by the way, those numbers exceeded expectations and the revision to January’s numbers didn’t really change much.) But the Friday collapse of Silicon Valley Bank has taken center stage.

We feel this is not a systemic event and draws attention to the most basic risk management tool available to all investors: diversification. This tool is always forgotten, especially when investors are stretching for income until an event like SVB’s failure hits the press. Then all the second-guessers wonder why they didn’t know. Well, here is why: in a zero-interest rate environment, folks forget the two biggest risks in the fixed-income markets to fulfill their desire for income are credit and duration. Yield is not a promise to pay; more than ever, it is a measure of risk. More relative income, more relative risk (credit or duration). SVB was hurt by poor diversification of its depositor base and too much duration in its investment portfolio — a painful combination and a tale as old as time.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.